An Analysis of Africa’s Lithium Crash: From $850/T Highs to an 80% Collapse — What It Means for Exporters Like Zimbabwe

June 13, 2025 by diadem445c3650ff

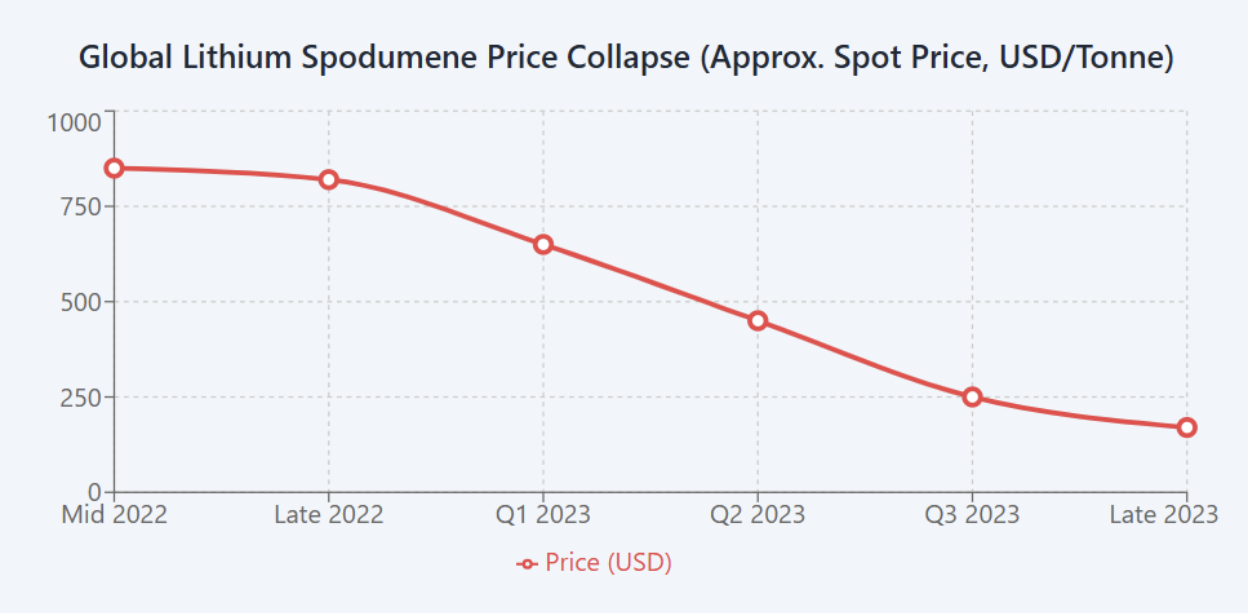

The lithium market saw a dramatic boom-and-bust cycle in the early 2020s. Prices for lithium products shot up through 2021–22 (for example, Chinese spot prices for spodumene concentrate briefly hit about $850/tonne) as electric vehicle (EV) and battery demand surged. However, by mid-2023, global oversupply (especially from China) and weaker-than-expected EV sales triggered a collapse of roughly 80%. By late 2023, lithium prices – from hard-rock concentrates to refined carbonate – had plunged to levels near 20% of their late-2022 highs. This reversal forced major producers (e.g., battery maker CATL) to suspend some mining operations and led top miners like Albemarle to cut costs and jobs. In short, the market turned sharply from a seller’s paradise to a buyers’ market, with prices tumbling about 80% in roughly one year.

Zimbabwe’s Lithium Boom (2020–2022)

Zimbabwe holds the largest lithium reserves in Africa and is rapidly becoming a new frontier for battery minerals. Beginning around 2020, Chinese firms flocked to Zimbabwe. For example, Zhejiang Huayou Cobalt spent ≈$422 million to acquire the Arcadia lithium project, and Sinomine Resources paid hundreds of millions for the Bikita mine. By 2022, Zimbabwe’s lithium sector was tiny (≈800 tonnes produced in 2022) but poised to expand. The government moved quickly to ban raw (unprocessed) lithium exports in late 2022, aiming to force value-added processing.

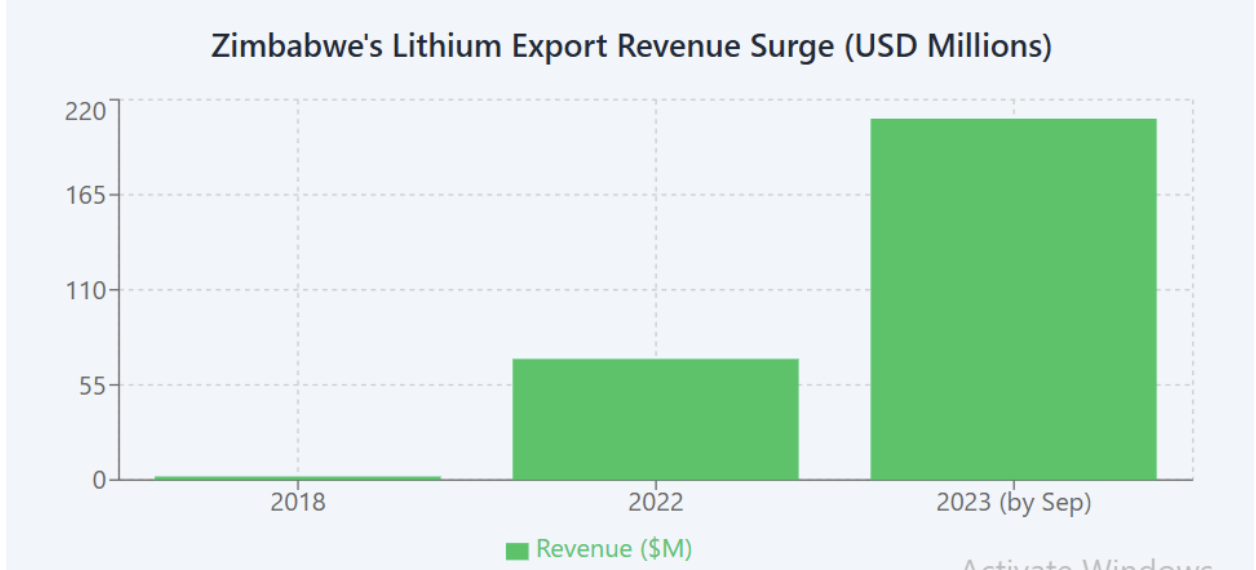

With these investments, production and exports surged. Output jumped to about 14,900 tonnes in 2023 and 22,000 tonnes in 2024. Export revenue reflected this boom: lithium went from less than $2 million in 2018 to roughly $70 million in 2022, then to $209 million by September 2023. By late 2023, lithium was on track to become Zimbabwe’s third-largest mineral export (after gold and platinum). In sum, a 2020s investment frenzy lifted Zimbabwe from near-zero lithium production to tens of thousands of tonnes in just a few years.

The Crash and Zimbabwe’s Mining Sector (2023–2025)

Lithium concentrate being loaded at the Prospect Lithium (Arcadia) mine in Goromonzi, Zimbabwe (January 2024). Chinese firms like Huayou Cobalt and Sinomine have invested over $1 billion in Zimbabwe’s lithium projects. As of 2024, nearly all Zimbabwean lithium was shipped as concentrate to China for further refining.

The sharp price collapse has put these operations under severe strain. Zimbabwe’s lithium miners – overwhelmingly Chinese-owned – have been cutting output and staff. According to government and industry reports, sustained price declines (~80% from late-2022) “have made it difficult for lithium companies to stay afloat,” forcing many to downscale production and lay off workers. For example, Sinomine (owner of Bikita) told legislators its Zimbabwe unit is operating below capacity due to the slump. In some cases, even large investors have paused new projects until prices recover.

Operating challenges have exacerbated these financial pressures. Zimbabwe’s deteriorating infrastructure and economic policies raise production costs. Miners report that weak roads, unreliable power and water, and logistical bottlenecks in rural mining regions significantly increase costs. Currency controls add another burden: Sinomine notes that a rule forcing export earnings to be converted (at a loss) into Zimbabwe’s local currency erodes miner revenues. In short, “fragile power supply, capital constraints, and foreign currency shortfalls” are impeding production.

At the same time, a large informal sector has sprung up around lithium. NGO investigations estimate ~5,000 artisanal miners were operating in Zimbabwe by late 2022, using primitive methods (picks, wheelbarrows) to extract ore. These small-scale miners often sell raw lithium ore at very low prices (around $100–$150 per tonne) to local buyers or traders. Much of this ore is reportedly smuggled into neighboring countries. The result is a massive leakage of value: material worth thousands of dollars on world markets is sold for only a few hundred locally. This means Zimbabwe’s impoverished artisanal diggers see little benefit from the lithium boom, while the state foregoes tens of millions in export earnings.

Overall, Zimbabwe’s lithium mining sector has been forced into retreat. Initial production gains are flattening or reversing as companies cope with the downturn. Some Chinese investors are even rethinking timelines; for instance, Kuvimba Mining (state-owned) pressed ahead with a new concentrator only on the expectation of a future price rebound. But currently, most exporters are in survival mode.

Zimbabwean Government Policy Response

In response to both the boom and the bust, Harare has enacted a mix of incentives and restrictions. In December 2022, it banned unprocessed lithium exports, and in June 2025 extended this to a formal ban on all lithium concentrate exports effective January 2027. The aim is to force foreign mining companies to build processing plants in Zimbabwe. Indeed, plans are underway: Sinomine’s Bikita and Huayou’s Arcadia each have lithium-sulphate/refinery projects in development, targeting local conversion of concentrate. The Minister Winston Chitando has stated that once these facilities are ready, “the export of all lithium concentrates will be banned from January 2027”.

However, as prices collapsed, the government has shown more flexibility. In late 2024, Deputy Minister Polite Kambamura said authorities would now assess miners’ plans “on a case-by-case basis” rather than enforcing blanket deadlines. Previously, companies had been given until March 2024. Facing pressure from struggling miners, the government softened these requirements while still emphasizing its value-added goals.

Zimbabwe has also introduced fiscal measures on lithium exports. In 2023 it imposed a 5% export levy on lithium concentrates to raise state revenue. This policy has been controversial: Zimbabwe’s Lithium Exporters Association (including major Chinese firms) has petitioned to delay the tax until 2027, arguing it should coincide with the launch of local processing plants. Industry sources note that policy reversals and quick changes (like these bans and taxes) have created uncertainty. Indeed, NGOs describe the export ban as a “knee-jerk reaction” to the resource rush, warning that erratic rules could scare off further investment.

In summary, the government’s approach balances two goals: capturing more value by building domestic refineries and keeping the mining sector alive amid a brutal price crash. It remains to be seen whether Zimbabwe can steadily develop its lithium industry without undermining investor confidence.

Geopolitical Considerations

Lithium is a strategic commodity, and Zimbabwe’s experience is tied to broader global rivalries. Chinese companies dominate Zimbabwe’s lithium sector: besides the >$1B invested overall, specific deals highlight this control (e.g., Huayou’s Arcadia, Sinomine’s Bikita). This fits China’s global strategy to secure critical minerals for its EV and battery industries. In turn, Zimbabwe’s “Look East” policy and political ties have made Beijing its favored partner for resource development. Western mining firms have largely shunned Zimbabwe due to political risk and sanctions concerns, leaving Chinese firms free to set the terms.

As a result, most of Zimbabwe’s lithium is shipped to China for processing (usually via subsidiary refineries or commodity traders). Beijing’s vast battery production capacity can absorb this supply, but it also means Zimbabwe has limited leverage. In the oversupplied lithium market, Chinese consumers can squeeze exporters’ margins. Geopolitically, Zimbabwe’s rise as a lithium supplier may boost its strategic importance to China, but it also makes Harare heavily reliant on one buyer amid a volatile market.

Regionally, Africa’s other lithium projects (in Namibia, DRC, etc.) are also attracting foreign interest, but Zimbabwe remains the continent’s biggest producer. Global moves to diversify away from China (e.g., U.S./EU seeking alternate sources) may put further pressure on Chinese-backed projects. For now, however, Zimbabwe sits squarely in China’s orbit for batteries – for better or worse.

Recommendations

- Stabilize and Clarify Policy: Avoid sudden rule changes. Phase in any export restrictions or taxes gradually, tied to market conditions. For example, delaying the export levy (as miners request) until local processing is viable can help preserve industry cash flow. Policymakers should commit to transparent timelines for refineries and tax policies, reducing “knee-jerk” volatility.

- Provide Targeted Relief: During the downturn, support mining operations with incentives. Options include temporary tax breaks, reduced royalties, or deferred levy payments for lithium miners. Easing foreign-exchange requirements (e.g., allowing miners to repatriate more foreign currency) could help maintain capital for investment. In short, mitigate the pain so companies weather the market trough.

- Improve Infrastructure: Invest in roads, power, water, and logistics in lithium-rich regions to lower production costs. Public-private partnerships (possibly with mining companies) could fund grid upgrades and transport links. Better infrastructure will make Zimbabwe more competitive when markets recover.

- Formalize Artisanal Mining: Bring informal diggers into the legal system. Legalizing small-scale mining (with permits and oversight) would capture more value and reduce illicit trade. Training and small loans could help artisanal miners use safer, more efficient methods. International experience shows that regulation can improve incomes and reduce environmental harm. A portion of revenues from artisanal operations (via fees or royalties) could fund local community projects, making the boom benefit rural areas.

- Encourage Downstream Investment: Continue to attract and support investors to build local refineries and battery-chemical plants, but pace them with demand. Consider partnerships with established global battery firms or host joint ventures to share technology. Meanwhile, ensure new plants meet environmental and labor standards to prevent past issues in mining. As lithium demand likely grows long-term, building domestic processing capacity will eventually pay off.

- Monitor Global Market Trends: Stay agile. The lithium industry is shifting (e.g., new battery chemistries, recycling). Zimbabwe should track demand and emerging technologies to adjust its strategy. For instance, if certain lithium compounds fall out of favor, the country can refocus on those in demand. Policymakers and miners should plan for price volatility as the norm.

Conclusion

Zimbabwe’s lithium story shows both opportunity and risk. The country’s vast reserves and recent investments promise future growth, but the recent 80%-plus price crash exposes vulnerabilities. By adopting stable policies, supporting miners through the downturn, and investing in value-added production, Zimbabwe can maximize the long-term benefits of its lithium wealth. If it navigates these challenges wisely, Zimbabwe could emerge not just as an exporter of raw ore, but as a lasting participant in the global battery supply chain.