An Analysis of the Cocoa Price Boom: Why Ghana Is Winning in Revenue but Losing in Output

July 14, 2025 by johneb492254456

Introduction

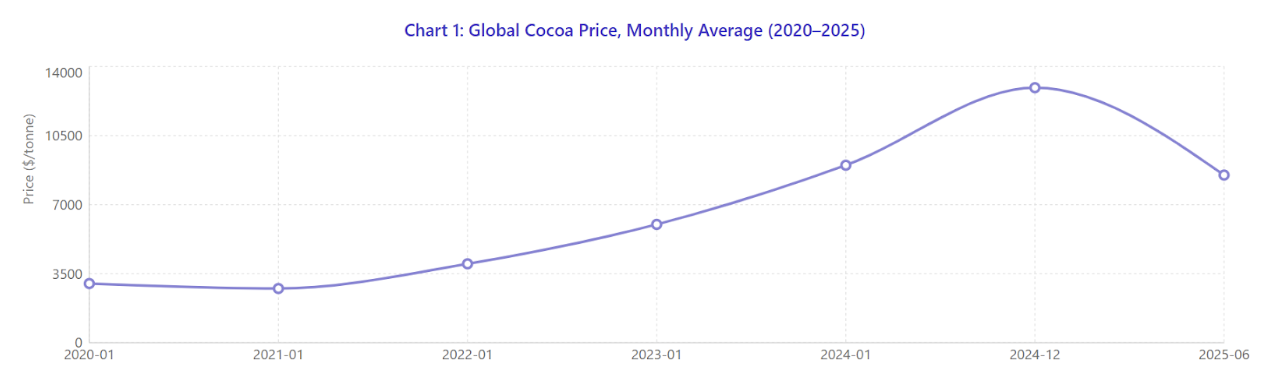

Global cocoa prices surged sharply from 2020 through 2024. After relatively moderate prices ($2,500–3,000/tonne) in early 2021, supply shocks and weather problems in West Africa drove futures much higher. By late 2024, cocoa had “nearly tripled in price” from its year-ago level, reaching a record NY–ICE high of about $12,930/tonne in late 2024. (For context, cocoa was trading near $3,000 in early 2020.) This boom was driven by consecutive years of production shortfalls in Ghana and Côte d’Ivoire – for example, Ghana fell to ~530,000 tonnes in 2023/24 vs. 1.05 million in 2020/21 – which tightened world supply.

The price boom greatly affects Ghana’s economy because cocoa is a major export. Cocoa contributes roughly $2 billion in foreign exchange per year (making it Ghana’s third-largest export). In normal seasons, cocoa revenues help finance the government and foreign currency earnings. When world prices soared, Ghanaian exporters in principle earned more per ton. Indeed, Ghana’s Cocoa Board (COCOBOD) saw its revenues jump – in 2022/23 it reported 17.7 billion cedi (≈$1.15 billion) in cocoa sales, up 42% year-on-year – the first profit in six years for the agency. However, much of this higher price did not translate into Ghana’s export earnings in 2024 (see below).

Prices began to ease somewhat in 2025, as improved weather and carryover stocks alleviated shortages. By mid-2025, ICE cocoa futures fell back to the $8,000–9,000/tonne range. Nonetheless, prices over 2023–24 remained at multidecade highs, roughly 3–4 times the levels of early 2020.

Prices began to ease somewhat in 2025, as improved weather and carryover stocks alleviated shortages. By mid-2025, ICE cocoa futures fell back to the $8,000–9,000/tonne range. Nonetheless, prices over 2023–24 remained at multidecade highs, roughly 3–4 times the levels of early 2020.

Ghana Cocoa Exports and Government Revenue

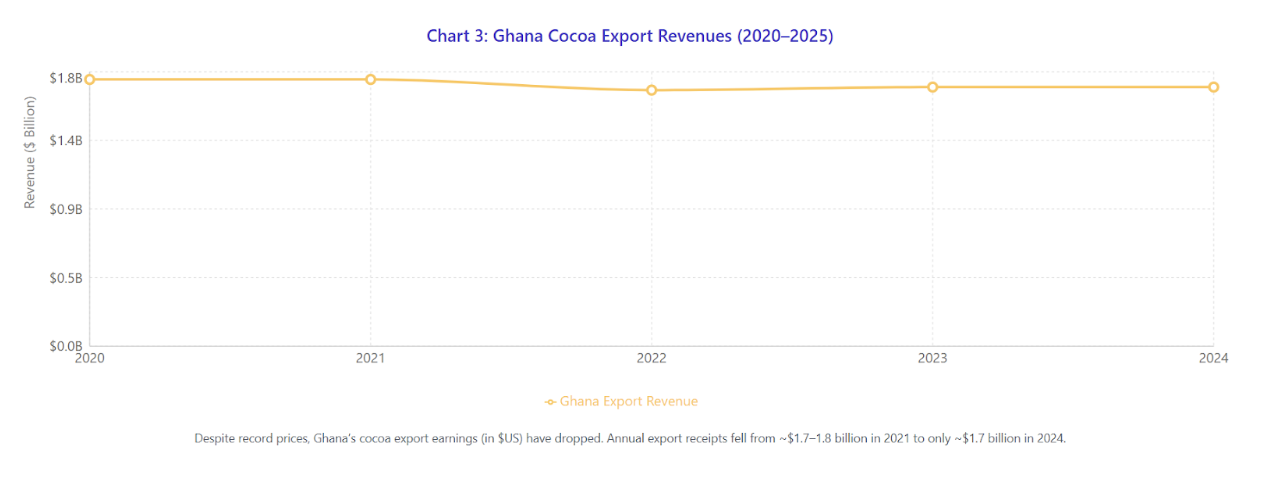

Cocoa remains a staple of Ghana’s export economy. Pre-crisis, Ghana earned roughly $1.7–2.0 billion per year from cocoa exports. For example, cocoa exports earned about $1.26 billion (beans) plus $0.41 billion (paste) in 2022 (≈$1.68 b total). By 2024, however, Ghana’s cocoa export revenues fell rather than rose, despite record prices. Bank of Ghana data show cocoa export receipts dipped below $2 billion, hitting about $1.7 billion in 2024, the lowest level in 15 years.

This paradox (record world prices but lower revenues) occurred because Ghana could not immediately sell its crop at the new highs. Due to prior forward-sale contracts (at lower prices) and delayed shipments, Ghana locked in a lot of its exports at much lower rates. In other words, high prices mostly went to fulfilling past commitments. Confectionery News reports that 57% of Ghana’s 2024/25 crop had been sold forward months in advance at pre-boom prices, limiting the benefit to the country. Thus even though global cocoa prices spiked by ~+157% in 2024, Ghana’s export earnings did not rise.

At the same time, Ghana’s government coffers from cocoa have been hit by currency and financing issues. COCOBOD’s operations carry heavy debt, and higher international prices did not immediately relieve its obligations. Ghana’s President warned in 2025 that COCOBOD stood to lose ~$1.3 billion on forward contracts written at low prices. (COCOBOD also struggled to roll over $2 billion of accumulated debt.) The shortfall in expected cocoa revenue contributed to Ghana’s fiscal strains in 2024/25. On the positive side, COCOBOD ended 2023 with a profit (2.3 billion cedi, ~$150 million) for the first time in years, as higher sales and its debt restructuring took effect. Overall, though, Ghana’s cocoa-dependent government revenues have not benefited from the price boom to the extent one might expect, because of currency fluctuations and contract timing.

Declining Cocoa Production in Ghana

Declining Cocoa Production in Ghana

Ghana’s cocoa production fell steeply from 2021 onward. After reaching a record ~1.04 million t in 2020/21, output declined to roughly 683,000 t in 2021/22 and 656,000 t in 2022/23. By the 2023/24 harvest (the season ending mid-2024), output plunged further to around 430,000–530,000 t. Early estimates for 2024/25 suggested a modest rebound (600k–700k t) as COCOBOD forecasts improved, but still well below pre-crisis levels. (Ghana’s government is targeting a symbolic 1 million t, which it has only met in 2010/11 and 2020/21.)

Multiple factors drove this slump. Climate and weather played a central role: West Africa suffered repeated droughts, unusually dry spells, and higher temperatures that stressed cocoa trees. Analysts note “adverse weather” for four consecutive seasons (2021–24) in Ghana and Côte d’Ivoire, with Ghana’s government explicitly citing an “unusual dry spell” in 2024 that cut its 2024/25 crop estimate from 810,000 to 650,000 t. Hot, dry conditions reduce flower pollination and pod development, sharply cutting yields.

Disease and aging trees also hurt yields. Cocoa Swollen Shoot Virus Disease (CSSVD) has spread in western Ghana, killing old cacao trees. Confectionery News reports that aging and disease have undermined Ghana’s mature plantations. Government sources note over 500,000 hectares of older cocoa farms in Ghana are “unproductive” due to CSSVD, old age and miners. Illegal gold mining (“galamsey”) destroyed or displaced many cocoa farms, particularly in the Western Region. Smuggling is another factor: low local prices in past seasons induced farmers to divert cocoa across borders (into Côte d’Ivoire or Togo). Reuters estimates over 150,000 t of cocoa were smuggled out of Ghana annually in 2021–2023. (This smuggled cocoa isn’t counted in Ghana’s official output.)

Labor constraints and under-investment are related issues: chronic low farm incomes in recent years meant farmers often skimped on inputs and replanting. Many smallholders age, and cocoa farming has become less attractive to young Ghanaians. Combined, these problems have hit Ghana’s production hard, even as world prices soared. (By contrast, Côte d’Ivoire maintained fairly stable production in 2019–23, highlighting Ghana’s outsized weather and governance issues.)

Impacts on Cocoa Farmers

Impacts on Cocoa Farmers

For Ghana’s farmers, the price boom has been a double-edged sword. In principle, higher farmgate prices should raise incomes, and COCOBOD did sharply raise Ghana’s official “producer price”. For the 2023/24 season, COCOBOD raised the farmgate price by 63% to 20,943 cedi/tonne (≈$1,837/t at the time), and for 2024/25 it jumped to 48,000 cedi/tonne ($3,070/t)– roughly three times the 2022/23 level. But these Ghana prices still lag far behind global prices. A Reuters analysis notes Ghana’s 2023/24 producer price of $1,837/t was much lower than world futures ($3,800/t), and by 2024/25 world cocoa peaked near $13,000/t while Ghana’s price was only ~$3,070/t. As a result, the high world market price has not fully reached farmers: many continued to lose out (some resorting to smuggling) rather than benefit from the “cocoa windfall”.

Meanwhile, the costs of farming have skyrocketed. Global inflation and currency moves have made fertilizers, pesticides, and labor much more expensive. Fairtrade reports that Ghana’s fertilizer prices (in cedi) nearly tripled since 2019, a 52% rise even measured in USD terms. Overall living costs for rural Ghanaian households jumped sharply in 2022–23. Thus, many farmers face a squeeze: even with higher nominal prices, input and living costs are eating up gains. Fairtrade notes that rising input costs mean farmers have “low profit margins” and may be unable to reinvest in their farms. A Fairtrade/Ghana report warns that the 2022 inflation increases of 59% in Ghana make it hard for farmers to earn a decent living.

The combination of low relative prices and high costs has kept many cocoa farmers in poverty. Confectionery News quotes Fairtrade Africa: “Global inflation on the cost of production and living has forced many farmers to live in poverty or extreme poverty.” Ghana’s rural poverty rates in cocoa areas have been high for years. Despite COCOBOD’s price hikes (farmgate roughly tripled in two years), farmers’ real income gains are limited if the Ghana cedi remains weak and inflation persists. Many farmers thus remain cash-poor: land tenure is weak, banks will not lend easily, and farmers often lack funds to replant old trees or buy fertilizers.

On the other hand, farmers do receive higher nominal payments per bag now than before the boom. The 2024/25 farmgate price (~3,100 cedi/bag or ~$307/t) is well above the ~$1,100/t in 2022. This may relieve some hardship, but it’s still below the global reference price that Ghanaian coffee/chocolate buyers pay. Ghanaian cooperatives and authorities are under pressure to raise future farmgate prices further: economists estimate a “living income price” of ~$2,100/t would be needed for Ghanaian farmers to earn sustainable incomes. Farm unions have demanded much larger increases in 2025/26.