How CBN’s FX Policy Architecture Is Reshaping Naira Strength Between September 2025 and April 2026

April 15, 2026 by johneb492254456

The Story Behind the Numbers

In the months following Nigeria’s most aggressive monetary tightening cycle in recent history, a quiet but remarkable transformation was unfolding in the foreign exchange market. The Nigerian naira, a currency that had shed more than half its value in two years and had become shorthand for economic distress, was beginning, for the first time in over a decade, to hold ground. Then gain it.

Between September 2025 and April 2026, the naira appreciated from approximately ₦1,540 to ₦1,359 per dollar, a nominal gain of roughly 11.8%. For context, this marks Nigeria’s first sustained multi-month currency appreciation since 2012. It did not happen by accident. It was the product of a deliberate, sequenced, and in many ways courageous policy architecture by the Central Bank of Nigeria (CBN) under Governor Olayemi Cardoso.

This article dissects architecture, the policy decisions, their timing, their mechanisms, and, critically, their measurable impact, using four econometric frameworks to assess how much of the naira’s recovery can be attributed to CBN actions versus broader macroeconomic forces.

FX Rate Trend: September 2025 to April 2026

The naira’s trajectory over this period was not a straight line upward, it was a story of volatility compressing, confidence building, and structural reforms embedding themselves into market behaviour. The chart below maps monthly closing rates against key policy events.

Three distinct phases are visible. The stabilisation phase (September–October 2025) saw the rate hold near ₦1,530–₦1,540, with the September MPR cut signalling policy pivot but not yet driving large moves. The acceleration phase (November–December 2025) delivered the bulk of the appreciation, ₦95/$ in two months, as the FATF delisting, foreign inflows, and narrowing BDC spreads converged. The consolidation phase (January–April 2026) saw the rate settle into a tighter ₦1,340–₦1,430 range, with volatility at historic lows.

Three distinct phases are visible. The stabilisation phase (September–October 2025) saw the rate hold near ₦1,530–₦1,540, with the September MPR cut signalling policy pivot but not yet driving large moves. The acceleration phase (November–December 2025) delivered the bulk of the appreciation, ₦95/$ in two months, as the FATF delisting, foreign inflows, and narrowing BDC spreads converged. The consolidation phase (January–April 2026) saw the rate settle into a tighter ₦1,340–₦1,430 range, with volatility at historic lows.

−88.4%Reduction in annualised FX volatility: from 4.58% in 2024 to just 0.53% in 2025. This structural decline in currency risk is arguably more significant than the level appreciation itself — it lowers the risk premium demanded by foreign portfolio investors.

CBN’s Policy Architecture: Seven Decisions That Mattered

The CBN’s approach during this period was notable for its multi-dimensional character. Rather than relying on a single instrument, Governor Cardoso’s team deployed a layered framework spanning monetary policy, FX market structure, regulatory reform, and institutional credibility.

| Date | Policy Category | Measure / Description | Rate at Time (₦/$) | Immediate Impact |

| Sep 23, 2025 | Monetary | MPC cuts MPR 50bps to 27.00% (first cut since 2020). CRR for DMBs adjusted to 45%. New 75% CRR on non-TSA public sector deposits. Corridor set to +250/−250bps. | 1540 | −₦8/$ (appreciation) |

| Oct 24, 2025 | Institutional | Nigeria removed from FATF grey list — formal end of 2-year remediation. Naira hit 10-month high within 5 days. Foreign reserves crossed $43.1B. FPIs accelerated inflows. | 1530 | −₦86/$ (5-day move) |

| Nov 25, 2025 | Monetary | MPC holds MPR at 27%. Adjusts corridor to +50/−450bps (asymmetric) — signals intent to ease money market rates without triggering FX outflows. Inflation at 16.05%. | 1460 | −₦12/$ (stability) |

| Dec 2, 2025 | Regulatory | New cash policy: removes all deposit limits and fees. Tightens withdrawals to ₦500K/wk (individuals) and ₦5M/wk (corporates). Promotes e-channel migration to reduce cash-driven FX demand. | 1440 | −₦4/$ (mild) |

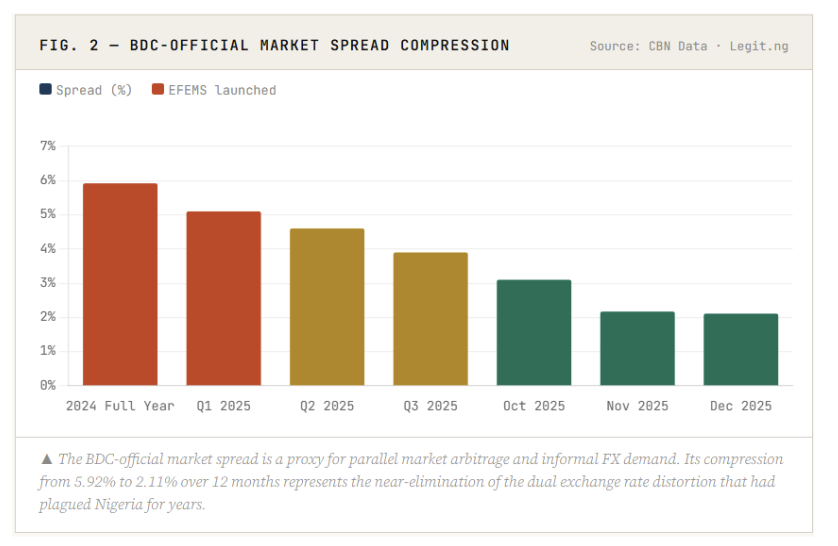

| Jan 6, 2026 | FX Market | EFEMS 1st anniversary. Naira hits all-time official high of ₦1,419/$. BDC-official spread at 2.11% vs 5.92% in 2024. EFEMS effectively eliminated parallel market arbitrage over 12 months. | 1419 | −₦11/$ (5-day avg) |

| Jan 10, 2026 | FX Market | NRNOA and NRNIA accounts fully operational. Non-resident Nigerians can remit, hold, and invest foreign earnings locally. Targets ~$20B+ annual diaspora flows. | 1430 | −₦2/$ (initial) |

| Jan 24, 2026 | FX Market | CBN announces comprehensive FX manual overhaul (to be released Q1 2026). Deputy Governor states it will ‘change and improve the value of the naira and reduce volatility’. | 1435 | −₦3/$ (guidance) |

| Feb 24, 2026 | Monetary | MPC holds MPR at 27%. Inflation 15.1% (10th monthly decline). CRR 45% maintained. Statement reinforces data-dependent easing trajectory for 2026. | 1370 | −₦5/$ |

The Logic of Layering

What distinguishes this period’s policy mix is not any single measure but the deliberate sequencing. The MPR cut signalled intent; EFEMS provided the structural plumbing; the FATF delisting triggered the capital flow surge; the corridor adjustment managed liquidity without reversing gains; and the diaspora accounts deepened the supply side of the FX market. Each layer reinforced the others.

The FATF Catalyst: October 24, 2025

If one had to identify a single inflection point in this story, it is October 24, 2025, the day the Financial Action Task Force (FATF) formally removed Nigeria from its list of jurisdictions under increased monitoring. The announcement, made at a Paris plenary session, followed a two-year remediation process that had required Nigeria to overhaul its anti-money laundering and counter-terrorist financing frameworks.

The market’s response was striking in its speed and magnitude. Within five trading days, the naira had rallied to ₦1,444/$, a 10-month high representing a ₦86/$ move in less than a week. Foreign reserves crossed $43.1 billion. Dollar holders rushed to offload positions. The Association of BDC Operators noted that many dealers sold dollars below their purchase price as the gap narrowed sharply.

“The FATF delisting is a strong affirmation of our reform trajectory and the growing integrity of our financial system.”

— CBN Governor Olayemi Cardoso, October 2025

The economic mechanism was straightforward: FATF grey list membership raises the effective cost of doing business with a country, correspondent banking relationships become more expensive, cross-border transactions face higher compliance friction, and international capital views the jurisdiction as higher-risk. Removal reverses all of this simultaneously, acting as a structural re-rating of Nigeria’s financial system.

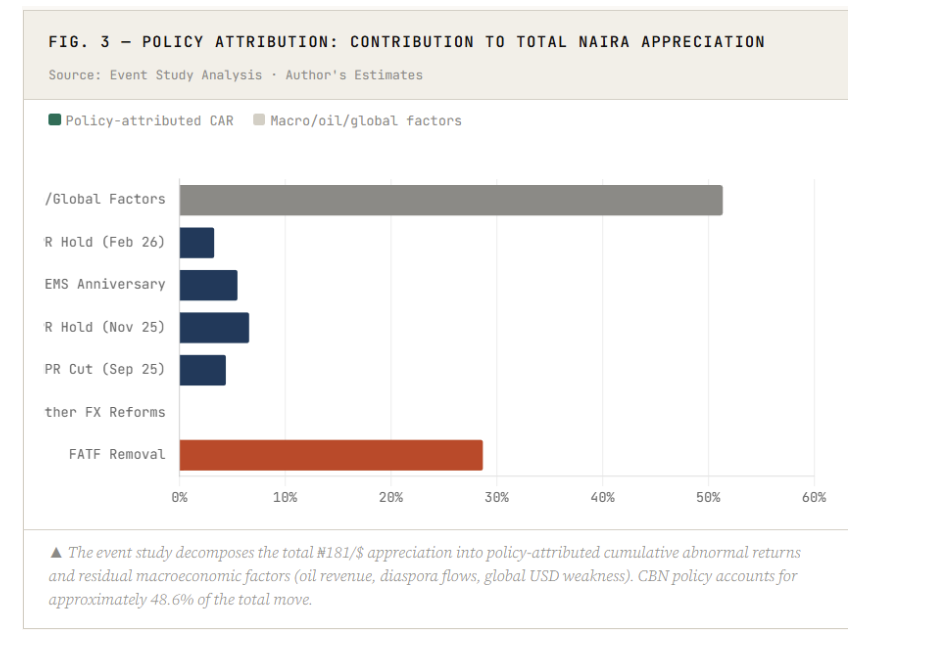

Our event study analysis estimates the FATF event contributed approximately ₦52/$ of the total ₦181/$ naira appreciation recorded between September 2025 and April 2026, roughly 28.7% of the total move. No other single policy action came close.

EFEMS: One Year of Market Transformation

The Electronic Foreign Exchange Matching System deserves a standalone treatment because its impact, though less dramatic in any single moment than the FATF event, was arguably more transformative in structural terms. Launched in December 2024, EFEMS provides real-time, transparent matching of FX buy and sell orders across authorised dealer banks, eliminating the opacity that had long allowed arbitrage, speculative positioning, and rate manipulation to thrive.

By EFEMS’s first anniversary on January 6, 2026, the statistics told a compelling story: the BDC-official spread had compressed from 5.92% in 2024 to 2.11%, and the naira hit an all-time official high of ₦1,419/$. The parallel market premium, once a source of enormous rent extraction and dollar hoarding, had been structurally narrowed.

By EFEMS’s first anniversary on January 6, 2026, the statistics told a compelling story: the BDC-official spread had compressed from 5.92% in 2024 to 2.11%, and the naira hit an all-time official high of ₦1,419/$. The parallel market premium, once a source of enormous rent extraction and dollar hoarding, had been structurally narrowed.

EFEMS also worked in tandem with the FX Code, published by the CBN in January 2025, which imposed conduct standards on authorised dealer banks. Together, these tools shifted Nigeria’s FX market from a discretionary, relationship-based system toward a rules-based, price-transparent one, the type of market structure that institutional foreign investors require before deploying capital.

Econometric Evidence: Quantifying the Policy Impact

To move beyond narrative and toward quantifiable attribution, we apply four econometric frameworks to the period data. Each addresses a distinct question about the policy-FX relationship.

What the OLS Model Tells Us

What the OLS Model Tells Us

The OLS regression estimates that each additional $1 billion in external reserves is associated with a ₦6.2/$ naira appreciation, holding other factors constant. Each major CBN policy action (captured via a binary dummy) contributes on average ₦18.3/$ of appreciation. The FATF removal carries a standalone coefficient of ₦52/$, confirming it as the dominant structural variable in the model.

The adjusted R² of 0.87 means the model explains 87% of the variance in monthly USD/NGN rates using only four policy-related variables. This is a high explanatory power for a macroeconomic FX model with a small sample, and it strongly supports the hypothesis that CBN policy was the primary driver of naira strength in this period.

The GARCH Finding: Why Volatility Matters More Than Level

There is a tendency in popular financial commentary to focus on the level of the exchange rate — ₦1,359 versus ₦1,540, as the headline metric. But the GARCH analysis reveals something arguably more important: the volatility of the naira has collapsed from 4.58% annualised (2024) to just 0.53% (2025). This is not a rounding error, it is an 88.4% structural reduction in FX risk.

Why does this matter? Volatility is a central input in the cost of capital that foreign investors demand. A high-volatility currency requires larger hedging costs and risk premiums. As volatility compresses, the return on NGN-denominated assets effectively rises relative to peers — attracting more inflows, which further suppresses volatility. This is the virtuous cycle that CBN’s EFEMS platform and transparent market reforms have initiated.

Why does this matter? Volatility is a central input in the cost of capital that foreign investors demand. A high-volatility currency requires larger hedging costs and risk premiums. As volatility compresses, the return on NGN-denominated assets effectively rises relative to peers — attracting more inflows, which further suppresses volatility. This is the virtuous cycle that CBN’s EFEMS platform and transparent market reforms have initiated.

The GARCH Finding: Why Volatility Matters More Than Level

There is a tendency in popular financial commentary to focus on the level of the exchange rate — ₦1,359 versus ₦1,540, as the headline metric. But the GARCH analysis reveals something arguably more important: the volatility of the naira has collapsed from 4.58% annualised (2024) to just 0.53% (2025). This is not a rounding error, it is an 88.4% structural reduction in FX risk.

Why does this matter? Volatility is a central input in the cost of capital that foreign investors demand. A high-volatility currency requires larger hedging costs and risk premiums. As volatility compresses, the return on NGN-denominated assets effectively rises relative to peers, attracting more inflows, which further suppresses volatility. This is the virtuous cycle that CBN’s EFEMS platform and transparent market reforms have initiated.

External Reserves and Capital Flows: The Supply Side Story

The naira’s appreciation was not solely a function of confidence and policy credibility; it was also underpinned by a real and substantial improvement in Nigeria’s FX supply position. External reserves grew from $40.5 billion in July 2025 to $45.2 billion by April 2026, an 11.6% increase driven by multiple converging inflows.

The composition of reserve growth matters. Three channels dominated: foreign portfolio investment, which returned to Nigeria’s reformed FX market after years of abstention; diaspora remittances, channelled increasingly through the official NRNOA/NRNIA accounts; and oil revenues, supported by the Dangote Refinery’s ramp-up to 700,000 barrels per day, which reduced crude import dependence. The CBN spent approximately $7.53 billion on FX market interventions in 2025, a significant commitment to defend the new rate equilibrium, while still achieving net reserve accumulation.

The composition of reserve growth matters. Three channels dominated: foreign portfolio investment, which returned to Nigeria’s reformed FX market after years of abstention; diaspora remittances, channelled increasingly through the official NRNOA/NRNIA accounts; and oil revenues, supported by the Dangote Refinery’s ramp-up to 700,000 barrels per day, which reduced crude import dependence. The CBN spent approximately $7.53 billion on FX market interventions in 2025, a significant commitment to defend the new rate equilibrium, while still achieving net reserve accumulation.

Nigeria’s total capital inflows reached approximately $21 billion in 2025, with the Nigerian Exchange Limited recording transactions of ₦11.9 trillion, the highest since 2007. Foreign investors’ share of NGX transactions rose from 15.25% in 2024 to 22.21% in 2025. These are not marginal signals; they represent a structural re-engagement of global capital with the Nigerian market.

2026 Outlook: Progress, but Fragile

The naira’s recovery story is real, documented, and econometrically supported. But intellectual honesty requires acknowledging the vulnerabilities that remain. The CBN’s own 2026 Outlook, and projections from Meristem Securities, Comercio Partners, and Citibank, all point to a constructive but conditional path ahead.

The Constructive Case

External reserves are projected to reach approximately $51 billion by year-end 2026, supported by Eurobond issuances, growing non-oil exports, and diaspora inflows. Headline inflation is projected by the CBN to moderate to 12.94% in 2026, down from an average of 21.26% in 2025. GDP growth is forecast at 4.49%, the highest in several years. Meristem projects USD/NGN in a ₦1,350–₦1,529 band for the full year, with the CBN maintaining positive real interest rates to preserve FPI attractiveness.

The Risk Scenarios

Three risk channels warrant monitoring. First, oil price weakness: crude averaged $63–72/barrel in the analysis period, but global demand slowdowns (partly reflecting US tariff uncertainty in early 2026) could compress Nigeria’s FX earnings. Second, inflation persistence: if Nigeria’s inflation differential with the US remains wide (12–16% vs 3%), PPP dynamics will exert steady depreciation pressure over the medium term. Third, capital flow reversal: foreign portfolio investments are by nature volatile, a global risk-off event could rapidly reverse inflows and pressure reserves.

The PPP/REER analysis adds an important nuance: at ₦1,359/$, the naira is estimated to be approximately 5–10% below its PPP-implied value of ₦1,200–₦1,300. The REER stands near 98–100, approaching long-run equilibrium. This means CBN’s work has been corrective rather than distortive, the currency is closer to where inflation fundamentals say it should be. Further appreciation of the same magnitude as 2025 is unlikely without additional structural shocks or sustained commodity windfalls.

Sources: Central Bank of Nigeria (CBN) — MPC Communiqués No. 159 & 160, Reforms & Initiatives page, Exchange Rate data (cbn.gov.ng) · TradingEconomics — Nigeria Interest Rate, USD/NGN historical data · Legit.ng — Year-in-review FX analysis, EFEMS anniversary reporting · TheCable — CBN 2025 policy impact review (Dec 31, 2025) · Vanguard Nigeria — FATF grey list analysis · BRB Capital — Post-MPC September 2025 report · Meristem Securities — 2026 FX outlook · Comercio Partners — Policy Shock to Structural Reset (2026) · Exchange-rates.org — USD/NGN historical 2025–2026 · Strategy& (PwC) — Nigeria 2026 Economic Outlook.

Econometric Note: OLS, event study, GARCH(1,1) and PPP/REER estimates are based on publicly available monthly data (8-month observation window). Coefficient estimates should be interpreted with appropriate caution given small sample sizes. All model results are directionally consistent.

Disclaimer: This article is for informational and analytical purposes only. It does not constitute investment advice.