From SWIFT to Stablecoins: Are Banks Still Relevant in Cross-Border Trade?

June 10, 2025 by johneb492254456

Cross-border trade is undergoing a seismic shift as blockchain-powered solutions like stablecoins promise instant, borderless transfers, challenging the traditional role of correspondent banks. For decades, the SWIFT network has been the backbone of international payments, but high costs, slow processing, and inefficiencies have opened the door to innovation. This week’s StayWired discussion explores whether banks remain vital in global commerce or if decentralized technologies are poised to render them obsolete, diving into costs, speed, and the evolving financial landscape.

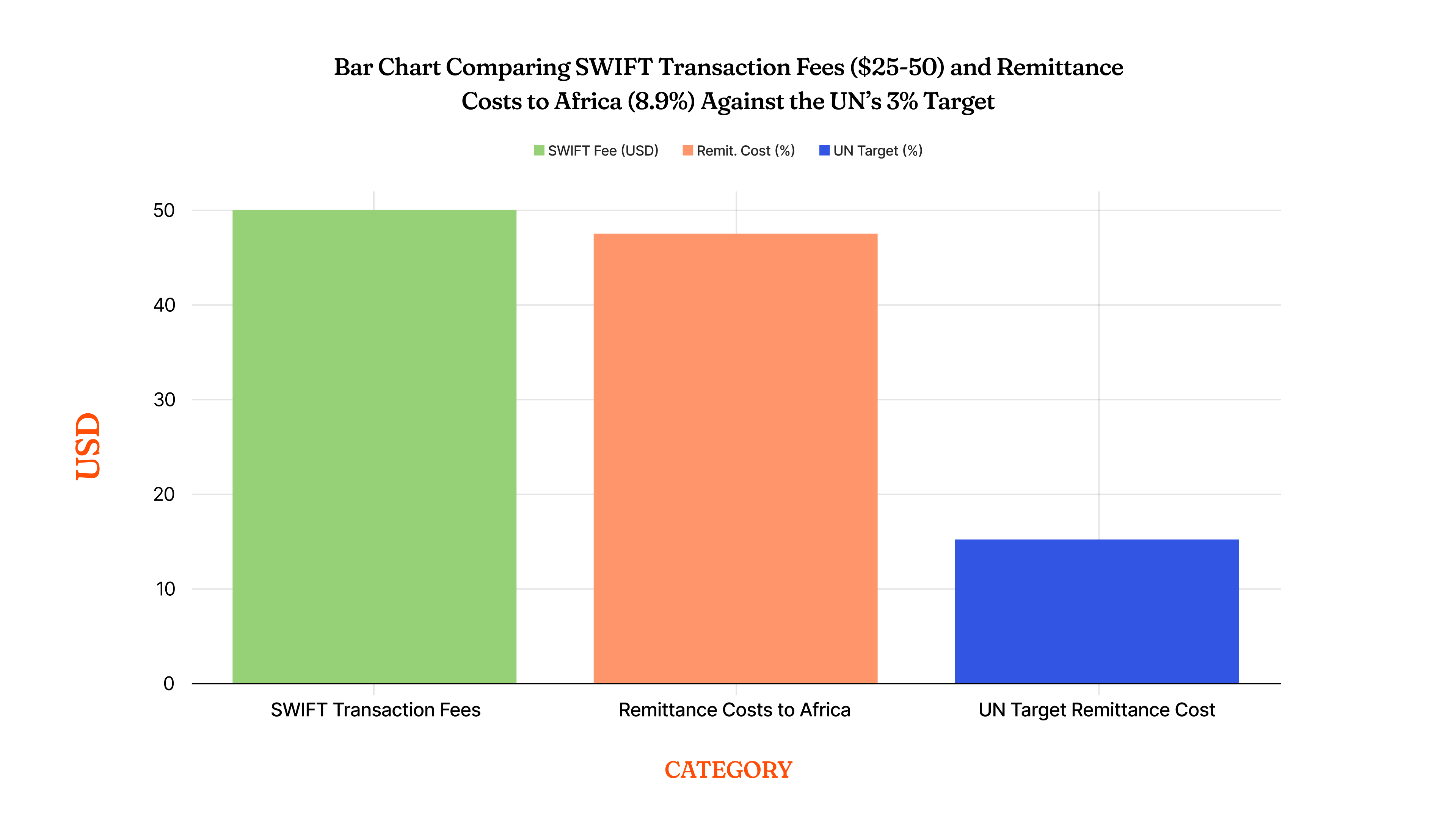

The SWIFT system, launched in 1973, connects over 11,000 financial institutions across 200 countries, handling $150 trillion in annual cross-border payments, according to SWIFT’s 2024 report. However, transactions often take 1-5 days, with fees averaging $25-$50 per transfer, per the World Bank’s 2023 data. Correspondent banks, acting as intermediaries, add layers of cost and delay, with smaller businesses in emerging markets hit hardest. A 2024 IMF study notes that remittance costs to Africa average 8.9%, far above the UN’s 3% target, exposing SWIFT’s limitations in a fast-moving world.

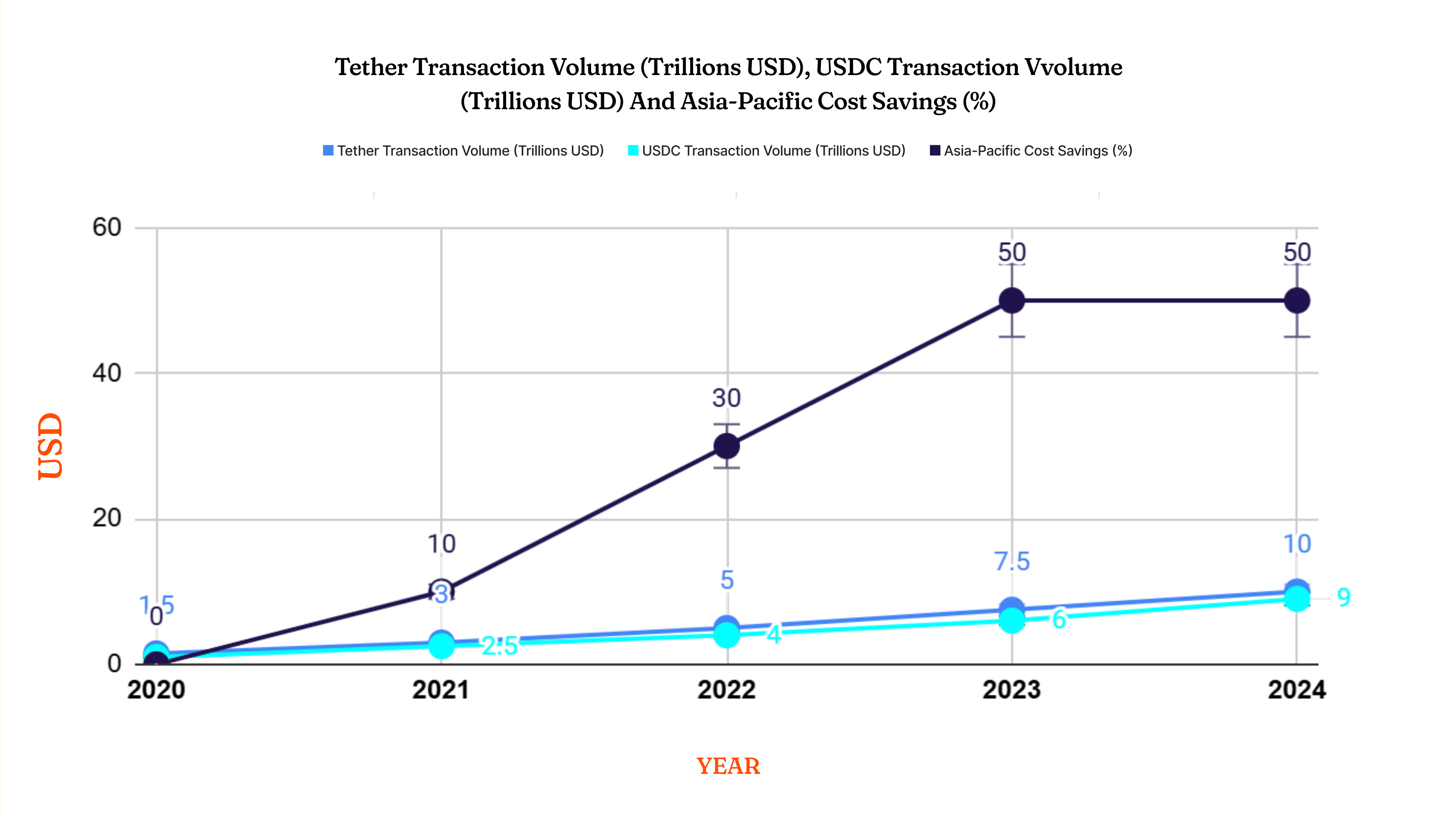

Enter stablecoins, digital currencies pegged to assets like the U.S. dollar, offering a compelling alternative. Tether (USDT) and USD Coin (USDC) processed $10 trillion in transactions in 2024, per CoinGecko, with near-instant settlements at fees often below $1. Blockchain’s transparency cuts out middlemen, enabling peer-to-peer transfers across borders. A 2023 Ripple survey found that 70% of Asia-Pacific firms using stablecoins for trade payments saw cost reductions of 50% or more, hinting at a revolution for exporters in places like Singapore and Thailand.

Banks, however, aren’t standing still. Major players like JPMorgan have launched JPM Coin, facilitating instant cross-border settlements, with $1 billion in daily transactions by 2024, per the bank’s annual report. The Bank for International Settlements’ 2024 mBridge project, a blockchain platform linking central banks, processed $22 million in test trades across four countries, showing banks can adapt. They also offer trust to FDIC insurance and regulatory oversight give comfort that stablecoins, often issued by private firms, can’t match, especially after 2022’s TerraUSD collapse wiped out $40 billion, per Chainalysis.

Speed and cost favor stablecoins, but risks loom large. The Financial Stability Board’s 2024 report warns of stablecoin volatility if reserves aren’t fully backed, with 10% of audited coins showing discrepancies. Regulatory gaps persist; only 25% of jurisdictions have comprehensive crypto laws, per the OECD, leaving cross-border trade exposed to fraud and money laundering. Banks, by contrast, comply with strict AML and KYC rules, with the Basel Committee noting a 98% compliance rate among global banks in 2023, a safeguard blockchain struggles to replicate.

Emerging markets highlight the stakes. In Latin America, where 60% of cross-border trade relies on U.S. dollar payments, stablecoins cut costs for small firms, with a 2024 Inter-American Development Bank study showing a 40% drop in transfer fees for Brazilian exporters. Yet, banks remain critical for credit—trade finance, like letters of credit, backed $5.2 trillion in global trade in 2023, per the ICC, a service stablecoins can’t yet scale. Without bank intermediation, smaller players risk exclusion from complex deals, especially in Africa and Asia.

Are banks still relevant? Stablecoins win on speed and cost, slashing fees and delays for cross-border trade, with volumes soaring past $10 trillion in 2024. But banks bring stability, credit, and regulatory trust—vital for large-scale commerce and risk-averse players. The future likely blends both: banks adopting blockchain to stay competitive, while stablecoins mature under tighter rules. Insight: A 2025 McKinsey report predicts hybrid systems could handle 20% of global trade payments by 2030, suggesting banks and stablecoins will coexist, reshaping commerce together.