How to Sell to Africa’s ‘Unbanked’—When They’re Not Poor

August 6, 2025 by johneb492254456

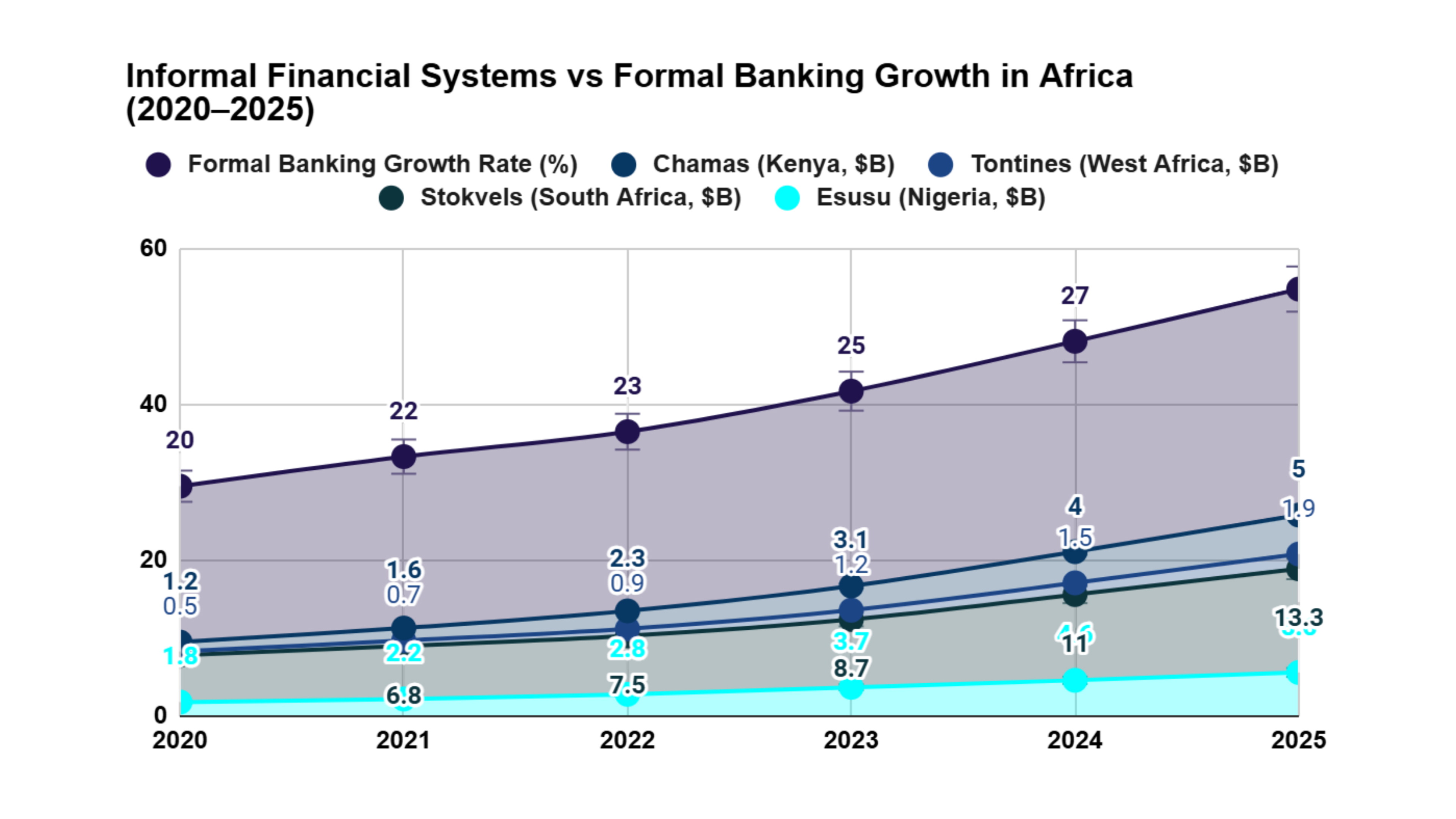

Africa’s unbanked population, often misjudged as financially excluded, drives a $20 billion informal credit economy through vibrant systems like Nigeria’s esusu, South Africa’s stokvels, and Senegal’s tontines. These community-based mechanisms reveal a market of creditworthy individuals, powered by trust and resilience rather than poverty. With Sub-Saharan Africa’s GDP growth projected at 3.5% in 2025 by the World Bank, this presentation explores how businesses can harness this ecosystem’s potential. Drawing from financial news, think tanks, and reports like the IMF’s 2025 Regional Outlook, we analyze opportunities amidst geopolitical shifts, including Middle East tensions impacting oil markets, and propose strategies for engaging this dynamic market.

The notion that unbanked Africans lack financial capacity is misguided. The World Bank’s Global Findex 2021 survey shows over 80 million unbanked adults in Sub-Saharan Africa earn cash from agriculture, trade, or remittances, fueling systems like Nigeria’s esusu, Kenya’s chamas, and Ghana’s susu. These rotating savings and credit associations enable participants to pool funds for business ventures, education, or emergencies, significantly contributing to local economies. South Africa’s stokvels, for instance, manage over $7 billion annually, according to a 2023 Nedbank report. The IMF notes that informal sectors account for 40% of GDP in countries like Nigeria and Kenya, underscoring the unbanked’s economic influence. Businesses must recognize this spending power to design products that align with these trust-based systems.

Africa’s $20 billion informal credit economy thrives on diverse systems tailored to local needs. Nigeria’s esusu involves regular contributions to a communal pot, accessible to members for loans or investments. South Africa’s stokvels support varied goals, from burials to property purchases, while Senegal’s tontines empower women-led enterprises, with 60% of participants being female, per a 2024 African Development Bank study. Kenya’s chamas, often digitized via mobile apps, facilitate group investments in real estate. Despite global challenges like reduced aid flows noted in the African Development Bank’s 2025 Economic Outlook, these systems remain robust, insulated from shocks like oil price fluctuations tied to 2024-2025 Middle East conflicts. Businesses can engage by offering tools that enhance these systems’ functionality without replacing them.

Africa’s $20 billion informal credit economy thrives on diverse systems tailored to local needs. Nigeria’s esusu involves regular contributions to a communal pot, accessible to members for loans or investments. South Africa’s stokvels support varied goals, from burials to property purchases, while Senegal’s tontines empower women-led enterprises, with 60% of participants being female, per a 2024 African Development Bank study. Kenya’s chamas, often digitized via mobile apps, facilitate group investments in real estate. Despite global challenges like reduced aid flows noted in the African Development Bank’s 2025 Economic Outlook, these systems remain robust, insulated from shocks like oil price fluctuations tied to 2024-2025 Middle East conflicts. Businesses can engage by offering tools that enhance these systems’ functionality without replacing them.

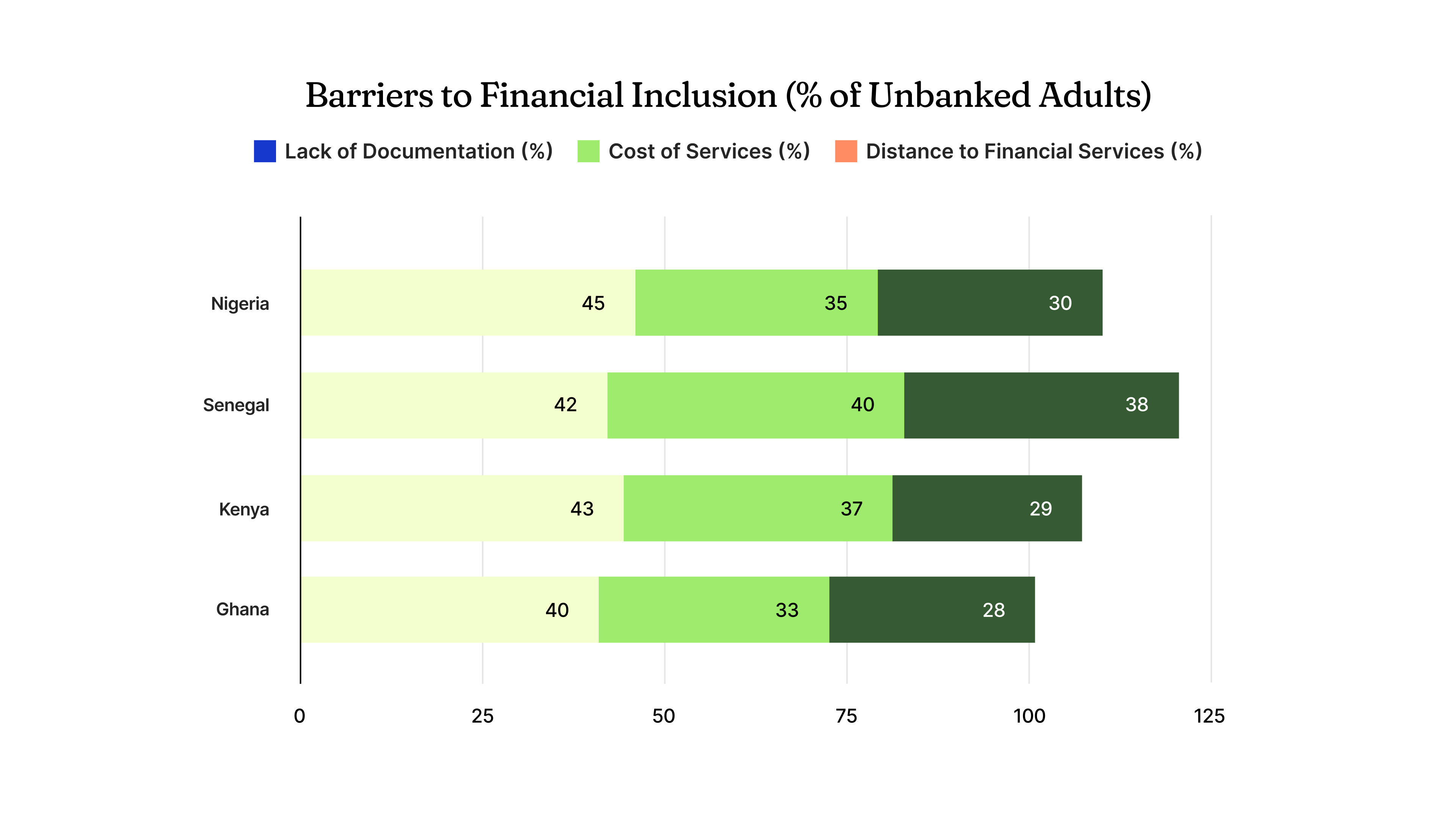

To reach Africa’s unbanked, businesses must integrate with systems like esusu, stokvels, tontines, and chamas. The World Bank’s 2023 Digital Africa report highlights mobile money’s role, with 15% account ownership growth in countries like Ghana from 2017-2022. Fintechs can develop apps to digitize esusu contributions, offering transparency while preserving community trust. Retailers can introduce microcredit or pay-later models, addressing barriers like lack of documentation, which affects 45% of unbanked adults, per Global Findex 2021. Diaspora communities in the U.S. and Europe, adopting similar systems, present a global opportunity. For instance, Ghanaian susu groups in the UK manage millions annually, per a 2024 Bloomberg report. Tailored financial products can bridge local and diaspora markets, amplifying reach.

Engaging Africa’s unbanked involves navigating risks like Nigeria’s 23.7% inflation rate in April 2025 (IMF) and food insecurity affecting 8% of its population, which strain informal systems. Geopolitical risks, such as potential U.S. aid reductions flagged by the Atlantic Council in 2025, may limit external support, increasing reliance on local networks. However, opportunities abound: Nigeria’s 2024 reforms, including subsidy cuts and currency liberalization, have spurred investor interest, per the IMF, creating a favorable climate for private sector growth. Fintechs and retailers offering affordable, tech-enabled solutions like mobile apps for esusu or tontines can capture a market where 464 million people remain in poverty yet actively drive informal economies.

Engaging Africa’s unbanked involves navigating risks like Nigeria’s 23.7% inflation rate in April 2025 (IMF) and food insecurity affecting 8% of its population, which strain informal systems. Geopolitical risks, such as potential U.S. aid reductions flagged by the Atlantic Council in 2025, may limit external support, increasing reliance on local networks. However, opportunities abound: Nigeria’s 2024 reforms, including subsidy cuts and currency liberalization, have spurred investor interest, per the IMF, creating a favorable climate for private sector growth. Fintechs and retailers offering affordable, tech-enabled solutions like mobile apps for esusu or tontines can capture a market where 464 million people remain in poverty yet actively drive informal economies.

Africa’s unbanked population powers a $20 billion informal credit economy through systems like esusu, stokvels, tontines, and chamas, proving their financial resilience. With Sub-Saharan Africa’s growth projected at 4.2% by 2026 (World Bank), businesses must move beyond stereotypes to tap this market’s potential. By digitizing trusted systems, addressing access barriers, and navigating geopolitical challenges like oil price volatility, companies can unlock significant opportunities. For the general public, this redefines financial inclusion as empowerment, not charity. Startups, retailers, and investors should act now: partner with communities, leverage mobile technology, and build products that amplify these systems’ strengths, positioning Africa’s unbanked as the next frontier for global fintech innovation.