Nigeria Oil & FX Outlook: H1 2025 Review and Q3 Outlook amid Iran–Israel Conflict

June 27, 2025 by johneb492254456

H1 2025 Oil Production & Exports

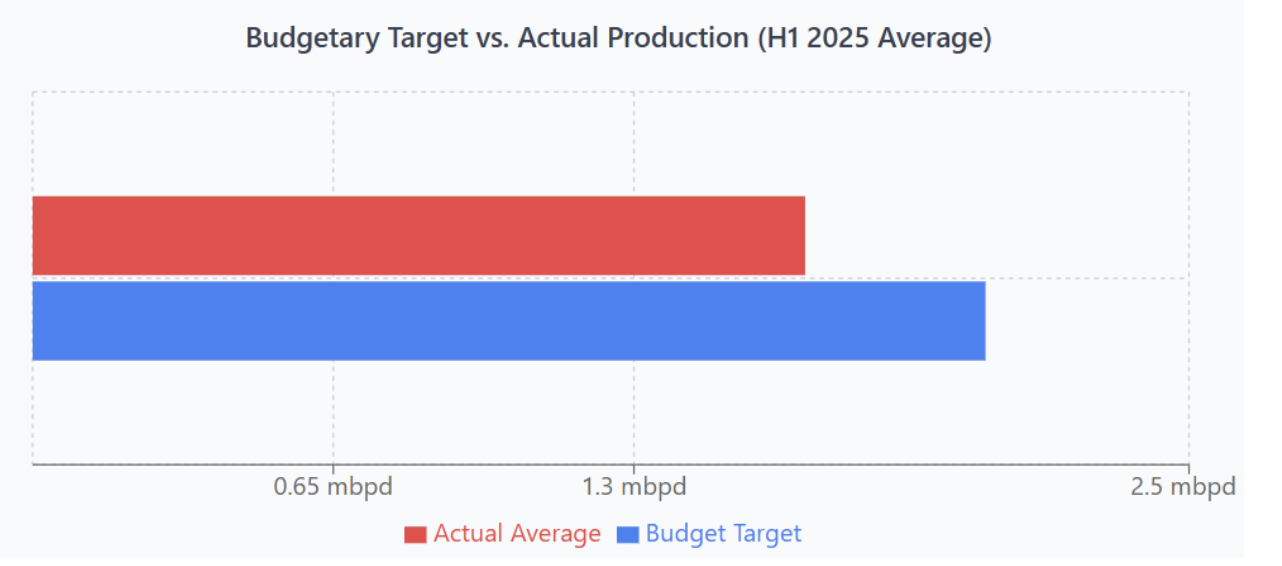

In the first half of 2025, Nigeria’s oil production remained underwhelming, continuing a multi-year struggle to meet output targets. Crude oil output, including condensates, hovered between 1.6 to 1.7 million barrels per day (mbpd), a figure significantly below the federal government’s budgetary benchmark. Specifically, production peaked modestly at approximately 1.74 mbpd in January, according to industry data, before declining to around 1.65 mbpd by May. Data released by the Nigerian National Petroleum Company (NNPC) shows that actual crude output in April was approximately 1.61 mbpd, underscoring the country’s chronic inability to meet its OPEC quota or internal fiscal assumptions.

The 2025 national budget, based on projections of 2.06 mbpd in average daily production for H1, was overly optimistic. The medium-term outlook from the Ministry of Finance and the Nigerian Upstream Petroleum Regulatory Commission (NUPRC) even targets 2.5 mbpd in the near future, a benchmark that has increasingly seemed aspirational rather than attainable. In reality, the deficit between projected and realized production levels in H1 2025 was stark, ranging between 20% and 25%. This shortfall has had direct consequences for oil revenues, dollar inflows, and fiscal planning, as oil remains the dominant source of government income and foreign exchange.

A persistent and structurally damaging factor behind Nigeria’s underperformance is the enduring challenge of oil theft and pipeline vandalism. According to investigative reports and statements from security agencies, the country is losing an estimated 200,000 barrels per day to illicit siphoning and sabotage along critical pipelines, particularly in the Niger Delta. These losses are not only draining government revenue but also discouraging investment and affecting the reliability of supply contracts with international buyers. In many cases, operators have been forced to shut down or defer production due to security concerns or export terminal disruptions caused by theft-induced downtime.

Adding to the complexity is the role of Nigeria’s domestic refining resurgence, led by the Dangote Refinery. This massive 650,000 barrels per day facility, which began scaling operations in early 2025, has begun absorbing a significant share of locally produced crude. According to the NNPC, Dangote alone is expected to refine roughly 99.5 million barrels over the year, a figure that already began impacting H1 crude export volumes. The broader local refining system, combining Dangote and smaller modular refineries, now demands approximately 770,000 barrels per day, representing over one-third of Nigeria’s total daily output. While this has greatly reduced Nigeria’s dependence on costly fuel imports, it has simultaneously diverted export-bound crude, further affecting oil revenue generation from foreign markets.

The combined effect of subdued production, theft-related losses, and increased domestic crude allocation has reduced the volume of Nigerian crude available for international export. Export performance in H1 2025 reflected this dynamic: according to NBS data aggregated by Nairametrics, Nigeria earned ₦12.96 trillion from crude oil sales in Q1 2025, a figure that represents roughly 63% of total exports for the period. However, this figure marks a 16% decline compared to Q1 2024, suggesting that despite more favorable pricing conditions in late Q2, overall export earnings from oil in early 2025 remained soft.

Yet, not all export dynamics were negative. Nigeria’s non-crude petroleum exports, such as petrochemicals and LNG, posted noticeable gains, benefiting from improved capacity utilization and expanded trade ties, particularly with India, the United States, and several European countries. This diversification, though still marginal about crude exports, points toward a slow but meaningful shift in Nigeria’s export mix.

In essence, Nigeria’s oil production and export trajectory in H1 2025 was shaped by an intricate combination of structural deficits, security challenges, infrastructural shifts, and ambitious fiscal assumptions. While the country did manage to maintain output within the 1.6–1.7 mbpd range, this level fell short of both domestic budget needs and external obligations. The implications of this underperformance have already started to manifest in oil revenue shortfalls and FX availability constraints, although later Q2 price spikes related to Middle East geopolitical tensions may help cushion the fiscal blow heading into Q3.

H1 2025 Oil Prices

In the first half of 2025, international oil markets moved through a distinctly two-phase pricing environment, marked initially by subdued pricing and later disrupted by geopolitical shocks. Nigeria’s benchmark crude, Bonny Light, which closely tracks global Brent prices, traded within a relatively moderate band of $70 to $75 per barrel for most of the half-year period. These figures were largely in line with the federal budget benchmark of $75 per barrel, providing some level of fiscal predictability in the earlier months of the year.

However, by May, signs of oversupply were beginning to weigh on market sentiment. Brent crude prices fell to around $65 per barrel during that month, reflecting both muted global demand and expectations of increased output from key producers. This downward drift was supported by forecasts from the U.S. Energy Information Administration (EIA), which had projected that, barring major shocks, global oil markets would remain oversupplied in 2025, potentially dragging Brent prices down to an average of $61 per barrel by year-end. This bearish outlook was rooted in expectations of inventory build-ups, weaker-than-expected industrial demand in Europe and China, and the phased unwinding of OPEC+ production cuts.

That trajectory, however, changed abruptly in June as geopolitical tensions in the Middle East escalated sharply. The intensification of the Iran–Israel conflict sent a ripple of uncertainty through global commodity markets. Investors and analysts responded swiftly to the increased risk of supply disruptions, particularly concerning the strategic Strait of Hormuz, a maritime chokepoint responsible for transporting a significant percentage of the world’s seaborne oil. As a result, Brent prices reversed course and surged to between $77 and $81 per barrel by the latter part of June, marking the highest levels seen since early January. Bonny Light, which typically commands a slight premium over Brent due to its low sulfur content and high gasoline yield, traded around $79 per barrel during the same period.

This late-quarter price rally proved to be a significant fiscal windfall for Nigeria. With a large portion of federal revenues and foreign exchange earnings tied to crude oil exports, even modest increases in the price per barrel have a multiplicative impact on national revenue performance. The jump in prices during June not only helped offset earlier shortfalls triggered by lower production volumes but also improved Nigeria’s external earnings potential heading into the third quarter. Moreover, the sudden shift in pricing dynamics highlighted the volatility of Nigeria’s fiscal outlook, which remains highly sensitive to global energy geopolitics.

In effect, H1 2025 can be characterized as a tale of two quarters, one of moderation and caution, followed by a sharp revaluation in oil markets that caught many observers by surprise. While the gains in June helped Nigeria edge closer to its budgetary assumptions, they also served as a stark reminder that global oil prices remain vulnerable to geopolitical flashpoints and that any fiscal strategy tied to hydrocarbons must be inherently adaptive and risk-aware.

USD/NGN and FX Liquidity

The naira has traded in a relatively tight range (₦1,400–1,600 per $) since early 2025, reflecting greater FX stability. The unified interbank (I&E) rate has been roughly ₦1,500–1,520 in mid-2025, while the parallel (“black”) market hovers ~₦1,590. According to analysts, the parallel market is now only ~5% above the official rate, indicating limited arbitrage. Higher oil receipts and remittance inflows are expected to keep the naira supported; one analyst notes that the recent oil‑price bump “could improve FX reserves by 15% and stabilize the naira”. The CBN has offered FX through weekly wholesale auctions and raised deposit and lending rates to defend the currency (MPR ~24.5%), while liquidity in foreign exchange markets appears ample. Overall, H1 saw a gradual strengthening (or at least stability) of the naira driven by better FX inflows, with little need for drastic central‑bank interventions so far.

Capital Flows & Reserves

Nigeria recorded a trade surplus in Q1 2025 (≈₦5.17 trillion) largely because imports fell faster than exports. The collapse in fuel imports (thanks to Dangote’s output) was a key factor. On the capital side, foreign portfolio flows have remained muted – global rate hikes and regional volatility keep many international investors on the sidelines. However, diaspora remittances (always one of the highest in Africa) continued to support FX supply through official channels. Externally, Nigeria’s reserve buffers are ample: end‑January 2025 reserves were $38.88 billion (≈8.8 months of goods imports). This is down slightly from December 2024 ($40.19 b) but still well above minimum thresholds. With trade surplus and higher oil earnings, reserves are likely to drift higher in H1. In short, Nigeria’s external position in H1 was healthy – sizable reserves, trade surplus, and steady remittances – even as capital inflows remained lackluster.

Impact of Iran–Israel Conflict

The Middle East conflict (mid‑June 2025 onward) sent shockwaves through oil markets. After U.S. and Israeli strikes on Iran, Brent briefly reached ~$81.4/barrel (a five-month peak) on June 23. Prices jumped ~$12–14 from May to mid‑June (Brent ~$65→$77), largely due to fears that Iran might close the Strait of Hormuz. Nigeria’s crude benefited: Bonny Light traded ~4% above Brent (≈$79). At Nigeria’s H1 output (~45 million barrels/month), the price rise translates into roughly +$630 million extra oil income in June. In percentage terms, analysts suggest this windfall could boost FX reserves by ~15%. In other words, the conflict has materially improved Nigeria’s oil receipts and bolstered FX.

However, there are important trade-offs. Higher international oil prices have lifted domestic fuel prices: petrol briefly reached N915–N925/liter in Lagos (versus ~N885 prior), stoking inflationary pressure. Experts warn of “dual risks” – imported inflation and potential capital flight to safe assets – that could tighten liquidity in FX markets. In sum, the conflict-driven oil spike is a net positive for Nigeria’s revenues and reserves, but it also heightens inflation and may induce cautious capital reallocations abroad.

Q3 2025 Outlook (Scenarios)

Several forces will shape the near-term outlook: the course of the Iran–Israel war, OPEC+ policy, global demand trends, and Nigeria’s own reforms. Key scenarios include:

- Escalating Conflict: If tensions intensify (e.g., actual closure of Hormuz or expanded strikes), Brent could surge toward $90–100+ (some forecasts see a short-term $90–100 and even $130 in a worst-case). Nigeria would gain materially more oil revenue (easing fiscal pressures) and likely see even stronger FX inflows. The naira could firm on additional reserves, but inflation risks would spike. Policymakers would face a trade-off: harness the revenue windfall while containing inflation (possibly via tighter fiscal spending or higher interest rates).

- Conflict De‑Escalates: If the war calms, oil supplies from Iran (and possibly Iraq) could gradually normalize. OPEC+ is already set to expand output (June +411 kbd), and analysts (Barclays) had forecast Brent in the mid‑$60s (cutting 2025 to $66/bbl). Likewise, the EIA’s base case expects rising inventories and falling prices (Brent ~$61 by end-2025). In this scenario, oil prices could retreat toward pre-crisis levels, squeezing Nigeria’s revenue. The naira might weaken due to less forex inflow, and fiscal shortfalls would re-emerge. Nigeria would then need production gains or budget adjustments to compensate.

- OPEC+ Decisions: Longer-term OPEC+ strategy matters. On the current course, extra voluntary cuts end by Oct 2025 (Barclays sees ~+390 kbd extra in 2025), which would put more downward pressure on oil. However, if prices fall too fast or conflict worsens, OPEC+ (led by Saudi Arabia) might pause or reintroduce cuts to stabilize the market. Nigeria, as an OPEC member underproducing its quota, may lobby for greater output allowances. If OPEC+ leans toward restraint, Brent could remain at elevated levels; if they flood markets, prices drop.

- Domestic Reforms: Nigeria’s internal policies will also shape Q3. Tight fiscal management (using windfalls to pay debt or invest) and continued FX liberalization (maintaining unified rate) would bolster stability. Achieving the NUPRC’s 2.5 mbpd production goal remains critical: any output gains would enhance export capacity if prices stay high. The government may also revise the budget if oil revenue far out/under‑performs targets. Meanwhile, inflation outlook hinges on CBN’s stance – if global rates stay high (due to war-driven inflation), Nigeria’s central bank is likely to keep policy rates elevated.

In summary, H1 2025 saw subdued output and a mixed revenue picture, but a sudden price shock improved prospects. For Q3, much depends on the Middle East conflict and OPEC+ actions. A sustained oil rally would benefit government coffers and the naira, whereas a reversal (via conflict easing or oversupply) would revive budgetary and FX pressures. Policymakers should prepare for either path by shoring up fiscal buffers when possible and ensuring liquidity. Overall, Nigeria’s ample reserves (∼9 months cover) provide some cushion, but the nation’s fortunes will ride on how these global and domestic factors unfold in the coming quarter.