Consumers Are Broke, But Sales Are Booming: Welcome to the Credit Economy

October 22, 2025 by diadem445c3650ff

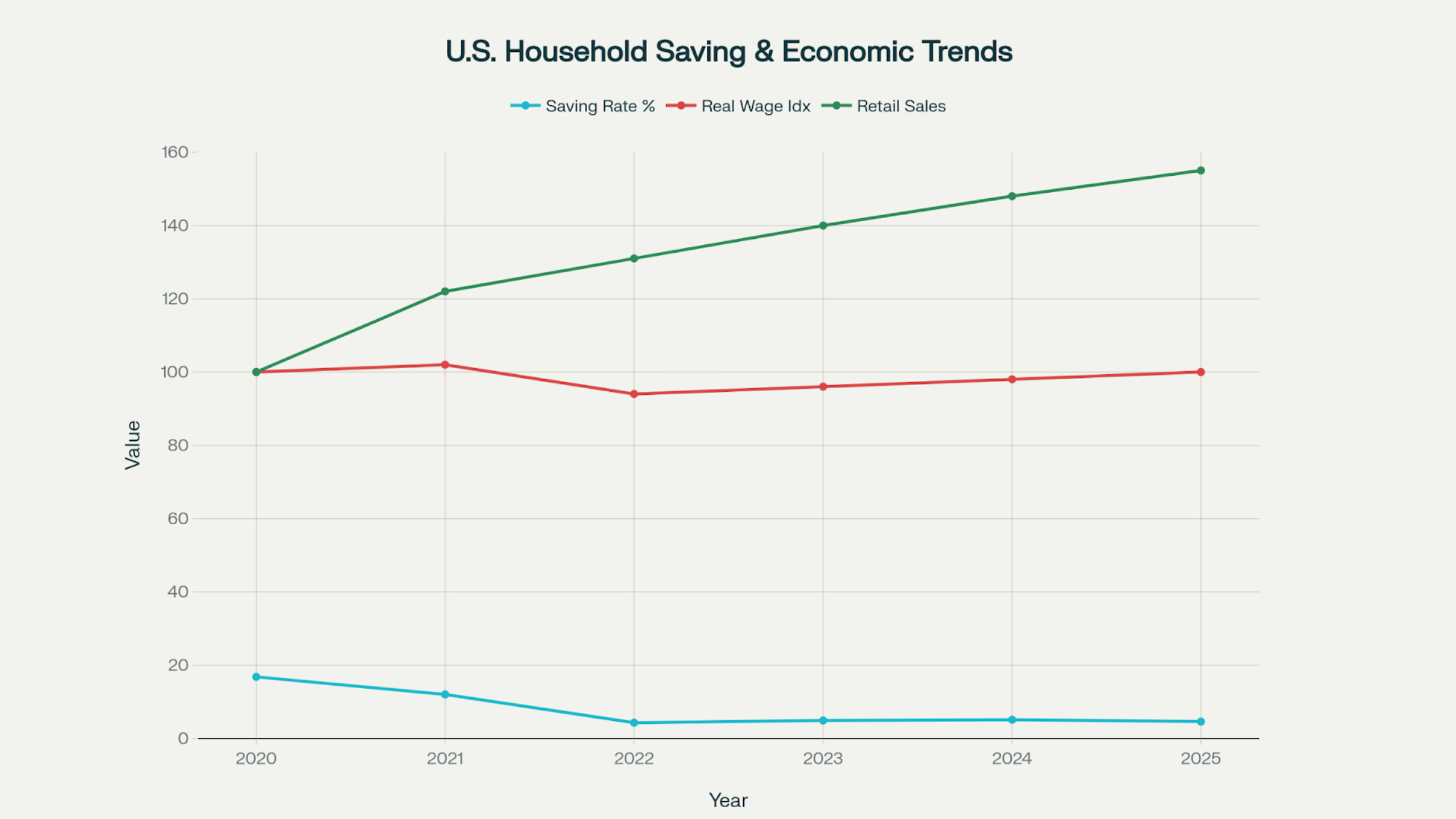

Across the world, a striking contradiction has emerged: consumers report feeling financially squeezed even as retailers report rising sales. In many advanced economies household savings have plunged and real wages are barely keeping up with inflation, yet spending remains robust. For example, by 2025 the U.S. personal saving rate had fallen to only about 4–5%, among the lowest levels of the past decade, even as retail sales jumped (up ~5% year-on-year in mid‑2025). Major banks and analysts now talk of a “resilient” or “stretched” consumer: a situation where apparent demand is largely bankrolled by borrowed money rather than rising income. U.S. banking CEOs note that consumers seem to be spending freely (with credit card delinquencies below expectations), but much of this is credit-fueled rather than salary-fueled.

Detailed data show the roots of this paradox. Real incomes have been weak: inflation-adjusted wages grew modestly in 2024–25, and in many countries still lag pre‑pandemic levels. An OECD study notes that even as average real wages have started to recover, in about two‑thirds of member countries they remain below their early‑2021 peaks. Meanwhile inflation and costs have surged (housing, food, energy), eroding spending power. Households have responded by cutting savings or drawing down reserves.

In the U.S., the official saving rate has tumbled to roughly 4–5% of income (from double digits during the pandemic), indicating far less buffer for rainier days. Emerging markets show similar strains: for example, many Nigerians report slashing non‑essential spending or borrowing to cover basics as prices soar. Yet total consumption figures keep growing. U.S. retail sales as of late 2025 were significantly above year-ago levels, and anecdotal reports from Africa and Asia likewise note stable or rising demand for staples even as budgets pinch.

In the U.S., the official saving rate has tumbled to roughly 4–5% of income (from double digits during the pandemic), indicating far less buffer for rainier days. Emerging markets show similar strains: for example, many Nigerians report slashing non‑essential spending or borrowing to cover basics as prices soar. Yet total consumption figures keep growing. U.S. retail sales as of late 2025 were significantly above year-ago levels, and anecdotal reports from Africa and Asia likewise note stable or rising demand for staples even as budgets pinch.

What explains the disconnect is debt. Credit balances have surged, effectively bridging the income shortfall. In the United States, total household debt has climbed to about $18.4 trillion by mid-2025. Non-mortgage debts are rising especially fast: credit card balances reached roughly $1.21 trillion in Q2 2025 (nearly 6% higher than a year earlier), and auto loans hit $1.66 trillion. This is mirrored by an upswing in new lending: large banks report record credit-card spending and mortgage originations. Notably, much of the credit growth is tied to higher‑income households: recent Federal Reserve analysis shows that affluent consumers have raised their credit spending aggressively (and carry lower debt relative to income), whereas middle‑income and poorer households have spent less and amassed proportionally more debt.

Beyond traditional loans, new forms of credit are proliferating. Buy-Now-Pay-Later (BNPL) plans and digital microloans have exploded in the past few years, especially among younger shoppers. U.S. regulators report that BNPL lending leapt from $2.0 billion in 2019 to about $24.2 billion in 2021, and industry growth suggests roughly $36 billion by 2024. Consumer surveys indicate roughly one‑fifth of Americans have used BNPL in the past year, often for clothing or electronics. Economist analyses find that BNPL significantly boosts short‑term spending (by effectively discounting immediate prices) at the expense of future liquidity. In many developing countries, mobile lending apps play a similar role: for example, in Nigeria over half of survey respondents said they took a loan or credit in the past year to meet everyday needs

The flip side of the credit boom is vulnerability. With households and governments more leveraged, higher interest rates and any credit squeeze could trigger trouble. Central banks around the world have kept policy rates elevated to fight inflation, meaning debt servicing costs are climbing. U.S. consumers now pay record interest on revolving debt (credit card rates are around 20%), and many emerging‑market borrowers face even higher rates. Surveys note that a nontrivial share of households are already caught in debt spirals – for example, roughly 4% of Nigerian respondents said they were borrowing simply to repay existing loans. Credit delinquencies are still relatively low, but they have begun inching up in 2024–25 in some markets. Regulators have taken notice: the UK and EU are moving to regulate BNPL, and many banks have tightened underwriting.

In sum, the “credit economy” paints a picture of temporary prosperity. Sales and GDP figures remain strong today, but this demand is increasingly financed by borrowing rather than actual income gains. Analysts note that much of the current growth may reflect consumers “front‑loading” purchases and using credit to smooth through high prices. The risk is that when borrowing stops or when debts come due under tighter money, the boom will reverse sharply. Policymakers and businesses are now charting credit trends more closely, recognizing that traditional indicators (retail sales, retail inventories, etc.) no longer tell the full story of household health. The bottom line: we live in a credit‑driven economy, where headline strength masks deeper strain. The next downturn, should one occur, may be defined by these hidden debts and the limits of synthetic demand.