How Stablecoins Are Redefining Savings in High-Inflation Economies

October 8, 2025 by diadem445c3650ff

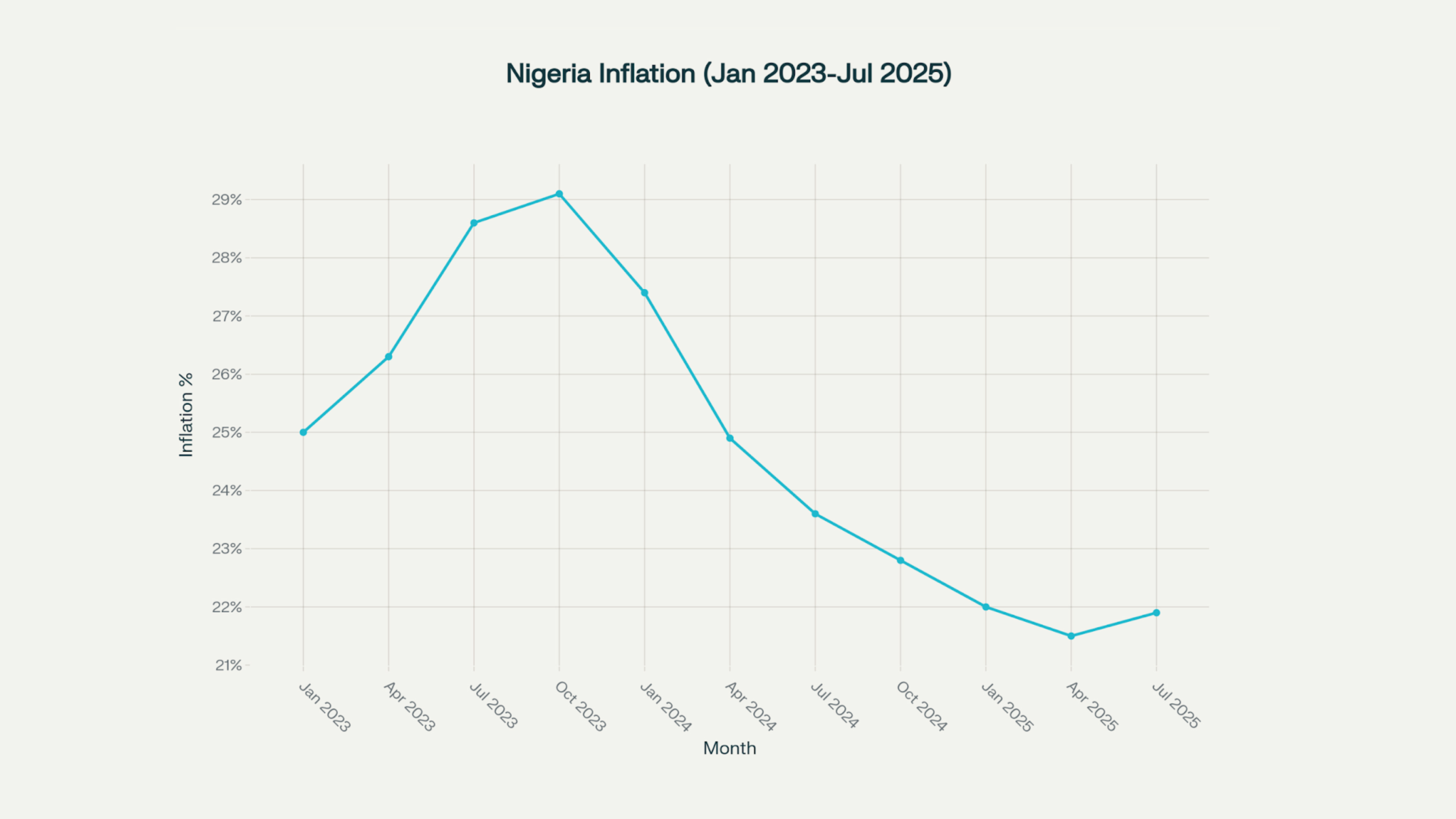

Across many emerging markets, blockchain-based stablecoins like USDT and USDC are supplanting traditional dollar savings. In countries where inflation is rampant and foreign exchange is restricted, people increasingly keep value in tokenized dollars rather than local cash. Stablecoins are crypto tokens pegged 1:1 to the U.S. dollar and backed by reserves, so they effectively act as digital dollar accounts. For example, Nigeria’s inflation ran near 21.9% in mid-2025 – so a Nigerian saver might move funds into USDT to prevent the naira’s erosion. As Morgan Stanley notes, in such environments stablecoins “are often considered a store of value, protecting against local currency depreciation”. In short, USDT provides 24/7 access to dollars through a smartphone, a practical hedge for households and businesses when official dollar accounts are scarce or expensive.

In high-inflation economies from Nigeria to Argentina, local currencies are losing value fast. Nigeria’s consumer prices hit 21.9% (year-on-year) in July 2025, and many African currencies have weakened dramatically. Governments often impose strict foreign‐exchange (FX) controls, making legal dollar accounts hard to open. This erodes trust in fiat and pushes savers to alternatives. A recent Chainalysis study finds that Nigeria has received roughly $92.1 billion in crypto inflows over 12 months, nearly three times South Africa’s volume, driven largely by inflation and limited forex access. In this context, crypto analysts and reporters emphasize that stablecoins can “mirror the strength of the U.S. dollar” and fill the vacuum.

Data from African crypto platforms confirm the trend. A Yellow Card–sponsored report finds stablecoins now represent about 43% of all crypto trading volume in sub-Saharan Africa, with Nigeria alone accounting for ~$22 billion over a one-year period. Practically every young trader or remittance sender there is increasingly using tokens like USDT instead of withdrawing dollars. Yellow Card itself says 99% of its transactions are in stablecoins (USDT alone is 88.5% of their volume). Roughly 70% of Yellow Card’s users report using these tokens for personal remittances or savings. This data highlights the point: for many people, USDT isn’t speculation – it’s a lifeline. Savers use it as a “digital dollar account” to park money.

The technical plumbing behind this shift involves crypto exchanges and mobile‐money interfaces. Africans often buy USDT on P2P networks or fintech apps. For example, global exchanges’ peer-to-peer desks (like Binance P2P) allow users to trade naira or shillings for Tether directly at market rates. Local startups such as Yellow Card, Bitnob or Bundi provide instant rubicon between Tether and mobile wallets or bank accounts. As Cointelegraph reports, some freelancers in Kenya now invoice clients in USDC and receive payouts in M-Pesa within minutes. In Nigeria, reporters note traders maintain working capital in USDT to avoid naira crashes. Chainalysis data back this up: in Nigeria, every transaction under $1 million in one quarter was in stablecoins, totaling about $3 billion.

This dollarization trend isn’t limited to Africa. Latin America’s high-inflation economies show similar patterns. Chainalysis notes that four LatAm countries rank among the top 20 globally for grassroots crypto adoption. In Argentina – which saw inflation over 100% – stablecoins dominate local crypto trading. About 61.8% of Argentina’s crypto transaction volume is now in stablecoins (versus ~44.7% global average). Every time the peso fell last year, Argentinians quickly piled into USDT on local exchanges. Venezuela’s population has also fled into crypto (BTC and stablecoins) as the bolívar collapsed; indeed, Venezuelan crypto inflows grew 110% YoY even while the government experimented with its own “petro” token

In summary, USDT and its peers have quietly become the new “dollar accounts” for many in high-inflation countries. Instead of speculating, everyday users treat these tokens as simple tools to protect their savings from eroding local currencies. This shift is still a small fraction of the global monetary system – stablecoins today represent a few tenths of a percent of world money supply – but the growth is striking. The total stablecoin market cap jumped from about $5 billion in early 2020 to roughly $300 billion by late 2025, driven in part by usage in emerging markets. Looking forward, stablecoins could become even more mainstream: financial giants and tech firms are racing to integrate them into payments, and a wave of central bank digital currencies (CBDCs) is on the way as governments try to offer an official digital alternative.