How Africa-Asia Trade Corridors Are Quietly Redefining Global South Commerce

October 14, 2025 by johneb492254456

Trade between Africa and Asia has surged in recent years, creating new South–South corridors that bypass traditional Western financial channels. In 2024, Asia–Africa trade is likely to exceed $400 billion (with China–Africa alone ~$296 billion). Major infrastructure projects (ports, railways, pipelines) and bilateral agreements are knitting Asian and African markets closer. Crucially, Chinese, Indian, and Southeast Asian investors increasingly settle trade in local currencies, reducing reliance on the US dollar and SWIFT. This shift – quietly championed by leaders from ASEAN to BRICS – is reshaping global trade patterns in the Global South.

Chinese Investment and Yuan Settlements

China is systematically pushing its yuan into Africa to support Belt & Road corridors. In 2025 alone, Chinese banks and African financial institutions signed multiple yuan-denominated trade agreements. For example, during Premier Li Qiang’s visit to Egypt, China and Egypt agreed on a yuan–dinar swap and expanded UnionPay and CIPS (China’s SWIFT-alternative) payment links for the Suez trade zone. Other African countries – notably South Africa, Nigeria and Angola – have struck yuan-settlement deals with Beijing. These accords allow exporters and importers to invoice directly in RMB, bypassing dollar credit lines.

The infrastructure for moving yuan is expanding: China’s Cross-border Interbank Payment System (CIPS), launched in 2015, now connects Chinese banks to their global counterparts. In mid-2025, two African institutions – Afreximbank and South Africa’s Standard Bank – joined CIPS as direct members. This allows them to clear yuan payments without an intermediary (and without routing them through Western SWIFT channels). Beijing has made dozens of currency-swap lines and payment pilots with African central banks. In short, Chinese projects on the continent are increasingly financed and repaid in yuan, reinforcing Asia–Africa corridors outside US/EU banking.

India’s Rupee Strategy in Africa

India’s Rupee Strategy in Africa

India is likewise encouraging local-currency trade with Africa. New Delhi has struck deals to settle more of its exports in rupees. In July 2023, India and Malaysia agreed that bilateral trade could be invoiced in INR. India is also negotiating rupee settlement pacts with key suppliers (like Saudi Arabia and the UAE) and has a longstanding rupee-for-ruble mechanism with Russia. To facilitate this, many foreign banks now hold Rupee accounts in India. By late 2024, 18 countries – including Kenya, Tanzania, and Mauritius – had banks with special Vostro Rupee accounts in Indian banks. This infrastructure lets an African importer receive rupees directly and swap them locally, skipping dollar funding.

Indian businesses on the continent welcome this trend. Trade between India and Africa recently topped $100 billion (nearly double from 2019), yet exporters often face costly currency hedging or credit constraints. As one analyst notes, “promoting Rupee-denominated trade could alleviate local liquidity issues, stabilizing costs for African importers and encouraging deeper integration”. In practice, this means a Kenyan firm importing Indian machinery might pay in rupees (via a correspondent bank) instead of sourcing scarce dollars – effectively bypassing Western banks and dollar exchange markets.

ASEAN and Southeast Asian Initiatives

ASEAN and Southeast Asian Initiatives

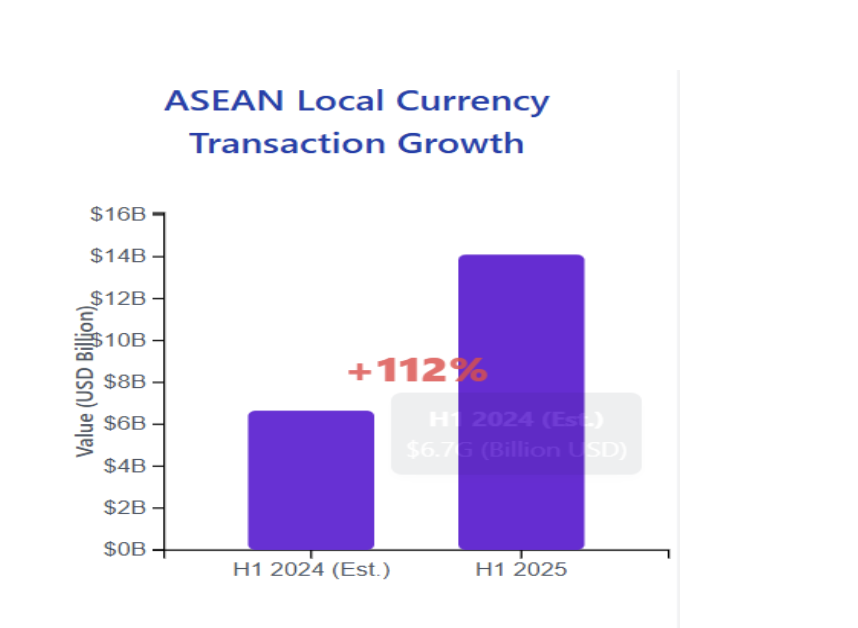

Southeast Asian economies have also built local-currency payment networks, which indirectly strengthen Asia–Africa links. Since 2016, Thailand and Malaysia have operated a Local Currency Settlement Framework allowing firms to settle trade in baht or ringgit. Indonesia joined the scheme in 2018, and new QR-code payment arrangements now let people pay cross-border in baht, ringgit, rupiah or other ASEAN currencies without any dollar intermediary. These regional platforms have taken off: in the first half of 2025, ASEAN cross-border transactions in local currencies hit $14.1 billion (a 112% jump year-on-year). Officials credit the shift with making trade and investment more efficient and reducing FX volatility in Southeast Asia.

Although ASEAN’s schemes mainly cover intra-ASEAN trade, they set a precedent that ASEAN-led investors bring to Africa. For example, Singaporean agribusinesses (like Olam and Tolaram) are major players in Africa, and Thailand’s investors (like Charoen Pokphand) operate widely. These firms, aware of their own region’s LCSF, increasingly favor using baht, ringgit or rupiah in their African deals when possible, mirroring what they do at home. At the 2025 BRICS summit, Malaysian PM Anwar Ibrahim explicitly cited ASEAN’s local-currency model as one to emulate, urging emerging markets to challenge Western dominance by trading more in national currencies.

Alternative Payment Networks

Beyond specific deals, several new payment systems underpin these corridors. China’s UnionPay network has expanded across Africa, and its Cross-Border Interbank Payment System (CIPS) is being pitched as an alternative to SWIFT for RMB payments. Africa’s Standard Bank and Afreximbank joining CIPS means African exporters can receive yuan settlements without US or EU correspondent banks. Similarly, India’s growing use of Special Rupee Vostros allows trade flows to settle via UPI or other domestic rails in Asia.

Looking ahead, multilateral projects could further cement local-currency corridors. For instance, ASEAN central banks launched a multilateral QR-payments system linking Indonesia, Malaysia, Singapore, and Thailand. BRICS countries (which now include major African economies like Egypt and Ethiopia) are developing their own payment platform (“BRICS Pay”) for cross-border local-currency transfers. Combined with regional swaps and central-bank arrangements (e.g., the 2012 SAARC Currency Swap for INR), these tools let Africa–Asia partners transact directly in yuan, rupees, baht, etc., sidestepping U.S. dollar clearing entirely.

Implications for Global South Commerce

These Africa–Asia corridors are quietly redefining trade in the Global South. By settling in local currencies, Asian and African countries reduce exposure to dollar volatility and Western sanctions. Exporters in countries facing dollar shortages (like Sri Lanka, Bangladesh, or many African economies) can keep exporting by switching to rupees or yuan. Importantly, this deepens economic ties on Asian terms: Chinese, Indian, Thai, or Malaysian lenders and investors gain leverage in financing and projects.

At the same time, experts caution about the broader impact. The IMF notes that while local-currency arrangements improve resilience for participants, they also fragment the global payment system – potentially raising costs by up to ~7% of world GDP. For now, the dollar remains dominant in overall trade, but its share is slowly slipping in corridors driven by geopolitics and necessity. As one analysis put it, these developments embody a trade fragmentation trend away from the U.S. and Europe.

In sum, African and Asian leaders are building new South–South financial infrastructure to match growing trade. These corridors – from Mombasa to Mumbai to Manila – unite continents through local currencies. They reflect a vision, voiced at forums like BRICS, of the Global South “speaking as one” and leveraging homegrown monetary systems. The result is a more multipolar commerce: one where African exporters may soon invoice in yuans or rupees instead of dollars, and Southeast Asian investors fund projects in local notes. In doing so, they redefine Global South commerce on their own terms.

Key Takeaways:

- Trade volumes are rising. Asia now takes ~40–45% of African exports (and vice versa), with Asia–Africa trade ~US$400B in 2024. China remains the largest player, but India, ASEAN, and others are growing fast.

- Local-currency deals. China, India, and ASEAN countries have struck swaps and trade agreements to settle in RMB, INR, baht, ringgit, etc.. African banks (e.g., Standard Bank, Afreximbank) have joined networks like CIPS to process these payments locally.

- Bypassing Western finance. These shifts reduce the use of dollar credit and SWIFT. CIPS, UnionPay, bilateral Rupee-Vostro accounts, and regional QR-pay systems let partners transact outside Western banking.

- Economic empowerment vs. fragmentation. Local settlement can aid countries with dollar shortages and foster South–South ties. But IMF analysts warn that a fractured payment landscape may hurt efficiency.

- Global South strategy. Emerging-market coalitions (BRICS, ASEAN) explicitly endorse this path. Leaders urge using local currencies to boost “Global South clout” and reduce dependence on Western-led systems