January: The Real Start of the Trade Year — Why December Data Misleads

January 7, 2026 by johneb492254456

Data released in January often upends the exuberance of December. Economists caution that calendar effects distort year‐end trade figures. As Brad Setser notes, the “pre-holiday surge in imports” in the U.S. and Europe shifts ever closer to Christmas, making it difficult to determine whether December’s strength is genuine demand or simply a seasonal pull-forward. In practice, companies often flood markets in Q4 to meet contracts and clear budgets, not because final demand increased. The result is a misleading spike in December numbers. Multiple sources confirm that once the holiday “noise” fades, January data show the true baseline of trade activity.

December trade volumes jump for several non‐economic reasons. Retailers heavily promote goods for the holidays and rush to clear annual budgets or take advantage of tariff windows. For example, retailers “took steps like front-loading imports” in Q4 while tariff increases were delayed. Supply‐chain experts observe that store shelves were kept “well‐stocked” by such front‐loading. Paradoxically, this means December volumes fall afterward – data from the NRF’s Global Port Tracker foresaw an almost 18% year‐over‐year slump in December import volumes (the weakest since March 2023) because firms had pulled shipments forward. In effect, December can look like “growth” when much of it is a timing shuffle – budgets had to be spent and contracts met at year’s end, regardless of true demand.

When the new year begins, these artificial boosts unwind. Importers that raced in December often pause in January as cash constraints, credit limits, and inventory realities set in. Logistics surveys show this shift. The January 2025 Logistics Managers Index, for instance, noted its fastest overall expansion in three years, driven largely by inventory buildup under tariff uncertainty. At the same time, truck freight volumes did not rebound with import dollar totals. FTR’s index for January 2025 plunged to –2.56 (vs +2.67 in Dec), reflecting weak freight volumes and utilization even as high-value goods arrived. In short, January data expose the “reality” behind the season: inflated demand signals collapse into genuine demand – often revealing that actual shipments and freight usage have slowed.

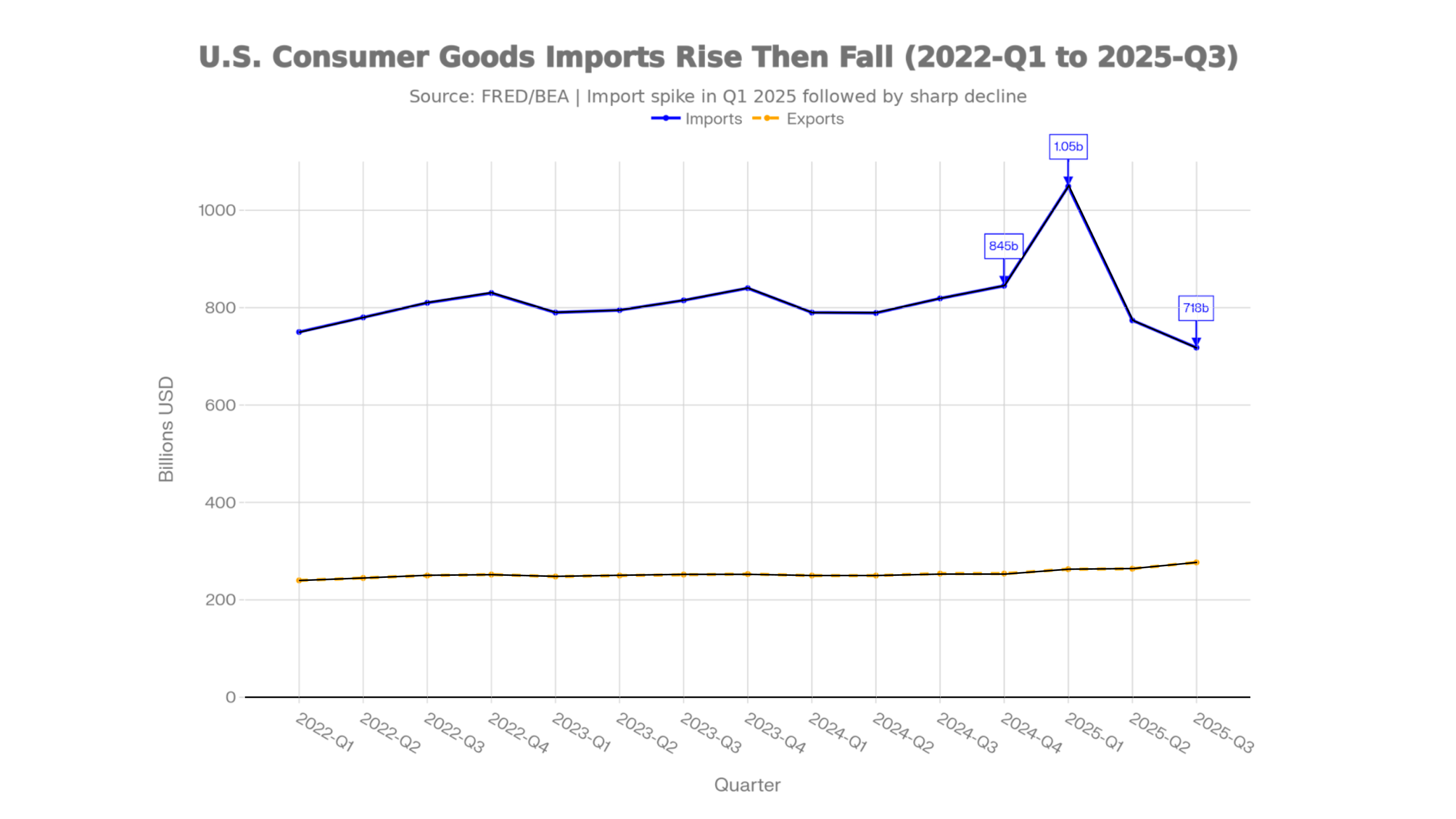

In the U.S., the consumer goods sector illustrates the December/January shift. The data show that imports of consumer goods (excl. food/auto) jumped from about $818.7 billion in Q3’2024 to $845.2 billion in Q4’2024, then collapsed to $717.9 billion in Q3’2025. Exports of consumer goods by contrast stayed around $250 billion per quarter, underscoring that the Q4 import spike was not matched by an export or demand increase abroad. In fact, January 2025 imports (SAAR) surged to an even higher $1,048.9 billion – largely because shippers advanced orders into year‐end, not due to new demand.

This December/January pattern is not unique to the U.S. Other economies show similar swings. Official German trade data, for example, swung markedly: January 2024 exports jumped 6.3% (and imports +3.6%) vs. Dec 2023, but by January 2025, exports were down 2.5% from Dec 2024. These month‐to‐month reversals reflect volatility around year‐end. China’s recent data also underscore the effect of single-period anomalies: in November 2025, China’s total exports actually fell 1.1% year-on-year, but shipments to the U.S. plunged over 25%, driven by year-end tariff moves. In short, spikes or dips at year‐end can obscure longer‐term trends in any country’s trade.

This December/January pattern is not unique to the U.S. Other economies show similar swings. Official German trade data, for example, swung markedly: January 2024 exports jumped 6.3% (and imports +3.6%) vs. Dec 2023, but by January 2025, exports were down 2.5% from Dec 2024. These month‐to‐month reversals reflect volatility around year‐end. China’s recent data also underscore the effect of single-period anomalies: in November 2025, China’s total exports actually fell 1.1% year-on-year, but shipments to the U.S. plunged over 25%, driven by year-end tariff moves. In short, spikes or dips at year‐end can obscure longer‐term trends in any country’s trade.

In sum, January often marks the true start of the trade year. December data can be an illusion, inflated by seasonal and fiscal factors. As multiple sources underline, year‐end trade figures should not be overinterpreted. When the holiday “noise” passes, January’s figures tend to reflect underlying consumption power and supply‐chain capacity. Businesses and analysts, therefore, look to January (and often March) to reset expectations. Citations from trade analysts and statistical agencies alike urge this perspective: only after the New Year’s transitional distortions do actual demand and inventory levels become clear, setting a reliable baseline for the year ahead.