Africa’s EV Critical Minerals Push — Which Countries Are Poised to Be Suppliers, and Which Are Left Behind

October 27, 2025 by diadem445c3650ff

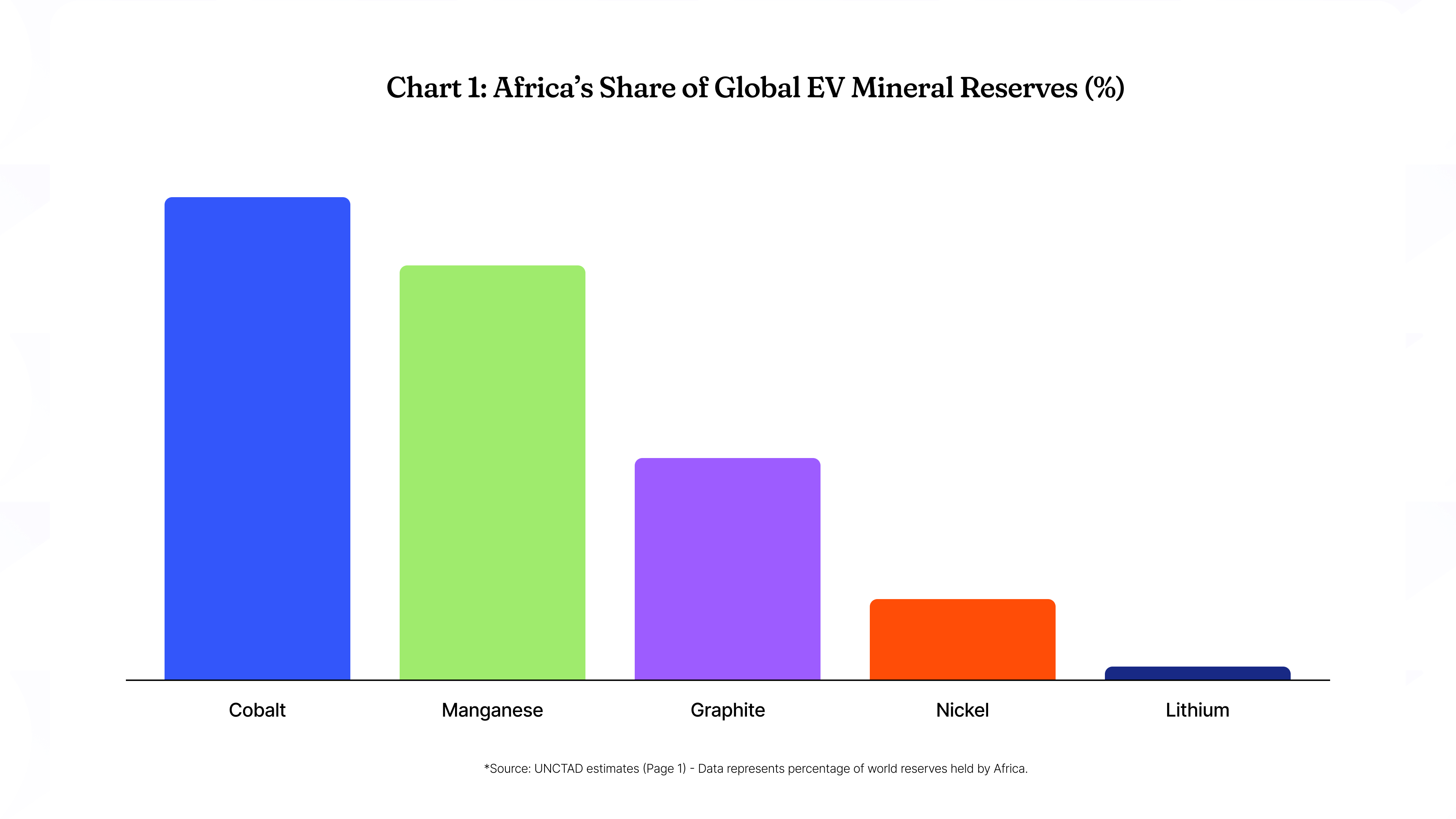

Africa is richly endowed with the minerals needed for electric vehicles (EVs) – in fact, UNCTAD estimates Africa holds roughly 55% of the world’s cobalt reserves, 47.7% of manganese, 21.6% of natural graphite, 5.6% of nickel, and 1% of lithium. As global EV demand surges, these deposits have drawn intense interest. African governments and companies are racing to expand mining and processing of lithium, cobalt, nickel, graphite, and manganese, the key battery metals. However, success varies widely. Some countries have the right mix of resources, policy suppor,t and infrastructure to become long-term EV-supply hubs, while others risk falling behind due to weak regulations, poor infrastructure or governance challenges.

African mines like this rare-earth operation in South Africa underscore the continent’s mineral wealth. Global demand for EV battery materials is shifting the calculus of African resource development.

EV Mineral Endowments by Country

Lithium: Africa’s largest lithium reserves are in Zimbabwe and Mali, with growing deposits in Namibia, Ghana and the DRC. For example, Zimbabwe’s Arcadia project alone hosts ~42.3 million tonnes of lithium (Li₂O) reserves – among the world’s largest hard-rock deposits. Bikita (Zim.) can output ~300,000 t of spodumene concentrate per year. Namibia’s Karibib mine is mining spodumene (773,000 t over its life) for export. New mines are coming online: Mali’s Goulamina holds ~142.3 Mt @1.38% Li₂O, and Ghana’s Ewoyaa 35.3 Mt @1.25%. The DRC’s Manono lithium project (401 Mt @1.65%) is under development. By contrast, West Africa’s Nigeria and Burkina Faso have lithium occurrences but very limited exploitation. Overall, African lithium output is small today but poised to grow (Zimbabwe and Namibia are already shipping concentrates).

Cobalt: The DRC dominates African cobalt – and the world – producing over 70% of global cobalt (around 170,000 t in 2023) and holding ~6.0 Mt of reserves (about half of the world total). Zambia produces modest cobalt (Munali mine ~4,000 t/yr) and has ambitious projects (FQM’s 30,000 t-planned Enterprise mine). No other African country is a significant cobalt player. Cobalt ore and hydroxide from the DRC are mostly exported to China and, increasingly, to Europe for refining. Other African nations have negligible cobalt output, so they are neither leaders nor major laggards in this mineral.

Nickel: Africa’s nickel output is modest. Madagascar’s Ambatovy mine (co-owned by Sumitomo) has a nameplate capacity of ~60,000 t of Ni per year, though production has been disrupted by a pipeline issue. South Africa produces a few thousand tonnes annually as a byproduct of its PGM operations (e.g., Mogalakwena, Impala). Zambia recently opened Munali (≈4,000 t/yr) and is developing the 30,000 t/yr Enterprise project. Tanzania holds Africa’s largest undeveloped nickel deposit (Kabanga, ~4.4 Mt @2.2% Ni), but no production yet. Zimbabwe has major nickel projects (Sabi Star, Bindura) on hold due to financing. In sum, Africa has potential (notably Madagascar and Southern Africa), but its nickel production is small relative to global demand.

Graphite: Major African graphite producers are Mozambique, Madagascar, and Tanzania. These three hold 69 Mt of reserves (≈21% of global). Mozambique’s Balama mine (Syrah Resources) has the world’s largest known graphite reserves (~16 Mt contained graphite) and produced 72,000 t in 2021. Madagascar’s Molo and Sahamamy mines together produced ~70,000 t in 2021. Tanzania has burgeoning projects (Mahenge, Nachu, Bunyu) expected to add hundreds of kt/year. (By contrast, countries like Nigeria or South Africa have minimal graphite output.) Africa supplied roughly 9% of global graphite in 2021 but stands to climb above 26% by 2026 if new Tanzanian mines come online. Almost all African graphite is currently exported as concentrate; downstream processing (flakes, anodes) is virtually non-existent on the continent.

Manganese: Africa is a global powerhouse. South Africa alone has ~38% of world manganese reserves (~640 Mt) and was the world’s largest producer in 2021 (7.2 Mt, 36% global).

Gabon has vast ore fields (250 Mt reserves by some accounts; 4% global according to one profile) and in 2021 was the #2 producer (4.34 Mt, 22% global). Ghana and Côte d’Ivoire also mine Mn (Ghana ~0.94 Mt in 2021). Combined, these four countries hold 43% of global manganese reserves. (Others: Nigeria has small Mn deposits but little output.) Traditionally, most African Mn was shipped to China and Europe for alloying.

Policy and Value-Addition Regimes

Policy and Value-Addition Regimes

African governments increasingly impose export restrictions and local-processing rules to capture more value. In late 2022–2023, Zimbabwe banned exports of raw lithium ore, and by January 2027, plans to ban even lithium concentrate exports, aiming to spur local refining. Zimbabwe extended the ban in 2023 to all unprocessed base ores, including nickel and manganese (with exceptions for existing local processors). Namibia followed in 2023, banning exports of unprocessed battery metals (crushed lithium ore, cobalt, manganese, graphite, etc.) without special approval. Nigeria outlawed most raw-ore exports in 2022 to encourage domestic refining. Tanzania also announced (2024) that raw lithium and other ores must be beneficiated locally. In the DRC, the government long imposed a cobalt hydroxide export ban (2022–25) to favor local smelting; it has now replaced the ban with a quota system effective Oct. 2025. Gabon, which has ~25% of the world’s Mineral reserves, recently announced that from 2029, no manganese may leave the country unless at least partially processed.

These policies are designed to attract downstream investment (refineries, precursor plants, battery factories). For example, South African firm Manganese Metal Company is building a $25 M plant to produce battery-grade manganese sulfate (5,000 t/yr) by 2026. The African Continental Free Trade Area (AfCFTA) is also seen as a tool to develop regional supply chains – it could allow producers like Mozambique, Madagascar, and Tanzania to export graphite concentrate to African processors rather than shipping everything to Asia. In several cases, mineral contracts and tax codes now favor local content and beneficiation: e.g. African governments have free-carried interests (e.g., Tanzania’s Kabanga nickel JV gives 16% free government equity) and new mining codes often raise royalties on pure ore exports.

Infrastructure Capacity

Infrastructure remains a mixed bag. South Africa, with the continent’s best transport network, has deep ports (Richard’s Bay, Saldanha), extensive rail linking mines (Kalahari Mn fields), and a continentalized road system – but chronic power shortages plague industry. Ghana and Mozambique have major ports (Tema, Maputo) and better power access, yet outside the main corridors, roads can be poor. The Africa Finance Corp’s 2025 report highlights the Lobito Corridor (Angola–DRC/Zambia rail) as a new corridor unlocking copper/cobalt exports. East African rail upgrades (e.g. Dar es Salaam corridor) similarly link Tanzanian graphite and copper belts to the coast. But outside these projects, most landlocked mines suffer. The AFC report notes “sharp disparities in road quality and density, with limited private participation outside mining corridors”.

Power is a critical constraint: battery and steel processing are electricity-intensive. DRC and Zambia rely on hydro (Congo and Zambezi basins) but still impose rationing during droughts. South Africa, despite having the continent’s largest grid, regularly enforces blackouts. Ghana and Namibia have relatively stable grids (Namibia draws on hydropower and solar) – a reason the EU and US favour these as secure partners. Lack of affordable, reliable power may sideline some potential producers: for example, proposals for lithium refineries in remote Zimbabwe sites could struggle without new power plants. In summary, only a few countries (South Africa, Namibia, Ghana) currently have the mix of ports, rails and grids to fully support large-scale processing; others must invest heavily in infrastructure or rely on partners (e.g. Chinese-built smelters) to bridge the gap.

Investment Trends and Geopolitical Players

China remains by far the dominant external player in Africa’s battery-mineral sector. It has funded mines and refineries across the continent – from Congolese copper/cobalt (Sicomines infrastructure-for-minerals deals) to Zimbabwean lithium mines and South African PGMs. Chinese state firms own or part-own key projects: e.g. China Molybdenum’s purchase of Congo’s Tenke Fungurume (3.3 Mt Co resource) and sponsorship of Zimbabwe’s Arcadia (Huayou Cobalt) and Bikita expansions. China also invests in African power and transport tied to resource access. In manganese, China consumes >50% of world output and sources ~20% of that from Gabon, illustrating its strategic demand for African ore.

Europe has launched “raw materials partnerships” with resource-rich African states. For example, the EU has signed agreements with the DRC, Namibia and Zambia to secure supply and promote local processing. European development finance is targeting Africa too: the EU recently labeled a Zambian cobalt sulfate plant (Kobaloni Energy) as a “strategic project,” signaling support. However, EU companies still invest far less than Chinese firms, partly due to African governments’ insistence on large stakes/value-add on-site.

The United States and Allies are ramping up engagement. In 2025 the US and Abu Dhabi launched a $1.8 billion Orion Critical Minerals Fund to invest globally in battery metals projects. The US DFC has approved financing for projects in Angola, Mozambique, Tanzania and Zambia (including graphite and copper/nickel developments). In 2023 the US co-founded a Tripartite Strategic Alliance with Zambia and the DRC, aiming to boost mining, refining and battery manufacturing. Renewing trade preferences like AGOA is also seen as critical to keep African minerals flowing to Western markets. Overall, Western capitals now articulate mineral diplomacy (often as security policy) to counter Chinese influence – but so far Chinese capital and offtake deals dominate the ground game.

Comparative Table of Leading vs Laggard Countries by Mineral

| Mineral | Leading African Suppliers (Reserves/Output) | Lagging/Untapped Countries |

| Lithium | Zimbabwe (largest African reserves, Arcadia ~42 Mt), Mali (Goulamina 142 Mt), Ghana (Ewoyaa 35 Mt), Namibia (Uis, Karibib) | Nigeria (known deposits, no mining), DRC (Manono deposit under development) |

| Cobalt | DRC (>$170,000 t/yr, 6 Mt reserves), Zambia (tens of kt/yr) | Others (South Africa, Madagascar have minor Co resources but no large production) |

| Nickel | Madagascar (Ambatovy ~60 kt/yr capacity), South Africa (Mogalakwena ~15 kt/yr by-product), Zambia (Munali ~4 kt, Enterprise planned) | Tanzania (Kabanga resource), Zimbabwe (Sabi Star deposit) – both mostly undeveloped |

| Graphite | Mozambique (Balama – 16 Mt contained, 72 kt prod ‘21), Madagascar (~26 Mt reserves, 70 kt ‘21), Tanzania (Mahenge/others) | Nigeria (small reserves), South Africa (historic mines), others minimal |

| Manganese | South Africa (640 kt reserves, 7.2 Mt prod ‘21), Gabon (61 kt reserves, 4.3 Mt ‘21), Ghana (13 kt reserves, 0.94 Mt ‘21), Ivory Coast | DRC (some Mn but little investment), Nigeria (minor Mn), Botswana (tiny output) |

Opportunities and Risks: Who Rises, Who Falls

Opportunities and Risks: Who Rises, Who Falls

The best-positioned countries are those combining large resources with stable policy and improving infrastructure:

- Democratic Republic of Congo (DRC) – by far Africa’s cobalt (and second-largest copper) powerhouse. If it can stabilize its quota system and attract processing plants, it will remain critical. The US, EU and China all vie for DRC cobalt, and billions have been pledged (e.g. Western-backed Lobito Corridor, Chinese-backed smelters) – giving DRC leverage. Its governance issues (corruption, conflict in the east) are a risk, but the scale of cobalt (and copper) deposits means it’s unlikely to be bypassed.

- South Africa – already a global leader in platinum-group and manganese. Its well-developed ports/rail and manufacturing base give it an edge. For example, South Africa controls ~38% of world Mn reserves and leads production. It also hosts flows of nickel (PGM by-product) and rare earth elements. However, its energy crisis is the biggest threat. Continued load-shedding (power cuts) could make local refining uncompetitive. Still, as the region’s financial hub with investment in battery precursors (e.g. 5,000 t Mn sulfate plant), SA has strong fundamentals to scale up EV minerals if it can secure reliable power.

- Namibia – politically stable and mining-friendly, with growing lithium (Uis pegmatites) and uranium. It is on track to be Africa’s third-largest lithium producer by 2026. The Namibian government has leveraged EU/US interests (e.g., the EU raw minerals deal) and provided incentives for processing (e.g., a new lithium plant is planned). Its existing ports (Walvis Bay) and regional grid also favor export and fabrication. In short, Namibia is a “stable haven” that Western and local investors trust, boosting its role in EV supply chains.

- Zambia – known for copper-cobalt, Zambia is investing in nickel (Munali, Enterprise) and has some lithium prospects. Politically, it has been relatively stable (recent change of government was peaceful). Western agencies have established offices in Lusaka, and a US-Zambia-DRC alliance is focused on batteries. Its electricity (hydro) is ample, though loans and fiscal troubles could constrain projects. If Zambia continues to diversify beyond copper, it could become a regional refining and manufacturing hub for batteries.

- Ghana – one of Africa’s most stable countries, Ghana has manganese (through Abu Dhabi’s acquisitions) and is developing lithium (Ewoyaa). Its government is encouraging value addition (e.g. negotiating for a planned Li refinery). Ports (Tema, Takoradi) are efficient and linked to power projects. If Ghana builds processing plants (possibly with foreign partners) it could become West Africa’s EV metals hub. Its fiscal discipline and mining code stability make it attractive to investors.

- Madagascar – holds major nickel (Ambatovy, Fenelon) and graphite (Molo) projects. The island’s relatively strong infrastructure (port of Toamasina, improved roads) and friendly investment laws help. Security is better than the mainland, though occasional political unrest remains a watchpoint. Its new exports (nickel, graphite) are poised to grow, making Madagascar an important player if global buyers can be secured.

- Gabon – with the world’s highest-grade Mn ore (44–48% Mn) and ~25% of global reserves, Gabon announced a bold plan to ban raw Mn exports by 2029. Its “Industrial Gabon 2035” strategy aims to attract alloy plants and battery precursor facilities. If Gabon builds the planned processing, it could capture much more value from its Mn. It has the Benin Gulf port and relatively good roads from the Moanda mines to Owendo. For now it is still a raw-ore exporter, but its policies and high-grade resources mean it could rise quickly in the EV chain.

- Mozambique and Tanzania – each has a mix of high-grade minerals. Mozambique’s Balama is already scaling graphite production, and its government plans a nickel smelter (Moma project) to use hydropower. Tanzania has the largest undeveloped nickel deposit (Kabanga) and booming graphite projects (Mahenge, Nachu). Both countries still need better power (Tanzania’s grid is improving, Mozambique invests in gas power) and greater investor confidence. If they stabilize their mining codes, they could become significant producers.

Conversely, the laggards or at-risk countries are those with one or more of: modest deposits, poor governance/infrastructure, or unstable policy. Examples include:

- Nigeria – despite being Africa’s largest economy, Nigeria has essentially no EV mineral industry (outside small rare-earth/radar minerals). It has some lithium and cobalt deposits on paper but lacks any active mines or refining, and is focused on oil/gas. Corruption, land disputes and lack of infrastructure have deterred mining investment. Without major reforms and infrastructure projects (rail, power), Nigeria will lag in the EV metals space.

- Fragile Sahel States (Mali, Burkina, Niger) – they have discovered lithium, gold, and other minerals, but successive coups and instability have scared away much investment. For instance, Mali’s Goulamina (lithium) was on track to be Africa’s largest Li mine, but now its future is uncertain under the junta. Burkina has lithium and gold, but dangers of conflict. These countries risk being left behind unless stability returns.

- Zimbabwe – a paradox. It has Africa’s largest lithium reserves (2nd globally) and substantial nickel and other minerals. However, chronic governance issues (hyperinflation, policy unpredictability, corruption) and weak law enforcement mean mines often export illegally. Although the government has progressive plans, much raw ore reportedly leaves the country clandestinely. Unless Zimbabwe improves its rule of law and genuinely enforces value-added policies, it may see less benefit than its resource potential warrants.

- Zambia (conditional) – Zambia has many strengths but faces risks. Its debt burden and policy changes (royalties, taxes, expropriation fears) have spooked some investors. Further, recent energy shortages (drought-hit hydro) have caused rolling blackouts. If these political and infrastructure challenges are not managed, Zambia’s momentum in new nickel/cobalt projects could slow, making it a slower-than-expected EV player.

- Other producers without added value: Several countries (like South Africa for manganese, Madagascar for graphite) are currently mainly exporting concentrates overseas. Even though they are leaders in supply, they risk being overshadowed by competitors who move up the value chain. For example, while Mozambique led global graphite output in 2019, militias and COVID shut it down, showing how security and logistics can quickly halt production

In summary, Africa’s EV minerals scene is at a crossroads. Countries with large endowments and stable, business-friendly environments (DRC, South Africa, Namibia, Zambia, Ghana, Madagascar, Gabon) are best poised to become major suppliers and possibly processors. Those with resources but facing governance or infrastructure shortfalls (Nigeria, Zimbabwe, unstable Sahel states) risk being left behind or remaining mere raw suppliers. Continental initiatives (like the African Union’s 2024 Green Minerals Strategy) signal a collective ambition to “industrialize through local beneficiation”, but realizing this will require massive investment in power, transport, and skills. The coming decade will likely see an acceleration of investment in African battery minerals – with winners and losers determined by policy choices and the ability to build a local value chain alongside extraction.