How AfCFTA Payment Systems Are Chipping Away at Dollar Dependence

October 14, 2025 by johneb492254456

The African Continental Free Trade Area (AfCFTA) aims for a single continental market, but its success depends on seamless cross-border payments. To that end, Afreximbank and the African Union launched PAPSS in January 2022 as a centralized RTGS platform for local-currency settlements. PAPSS is designed to let African businesses pay each other in their own legal tenders (for example, Egyptian pounds to Kenyan shillings) in near–real time, bypassing USD intermediaries. In the words of PAPSS’s CEO, this infrastructure keeps payment flows inside Africa (avoiding expensive routes via New York or London) and unlocks a $3.4 trillion intra-African market.

Mechanics and Processes

PAPSS operates as an RTGS payment infrastructure connecting African central and commercial banks. According to its official description, it “enables the efficient flow of money securely across African borders” by collaborating with central banks and payment service providers. Key features include:

- Flow of transactions: A payer initiates a cross-border transfer through their local bank or PSP in the payer’s currency. The payment instruction is sent via PAPSS through the originator’s central bank to the beneficiary’s central bank, which ultimately credits the recipient’s account in the local currency.

- Validation and routing: PAPSS validates each instruction (fraud checks, balances, compliance) and routes it to the correct destination central bank, which in turn settles it with the local receiving bank. This avoids the need for correspondent banking relationships.

- Pre-funding and instant settlement: Banks and PSPs pre-fund PAPSS accounts to guarantee liquidity. In practice, transactions clear in roughly 2 minutes, as the system ensures funds are available before sending.

- Daily net settlement: At the end of each day, all bilateral obligations are netted out. PAPSS instructs each central bank (using Afreximbank as a settlement agent) to settle remaining net differences. Recipients receive final credit in their local currency once settlement is complete.

These processes transform what used to take days or involve multiple currencies into a single-step transfer. For example, when PAPSS launched in Comoros (Aug 2024), its central bank highlighted that payments between Comoros and any other African country could now be completed in ~120 seconds in Comorian francs, without first converting to a foreign currency.

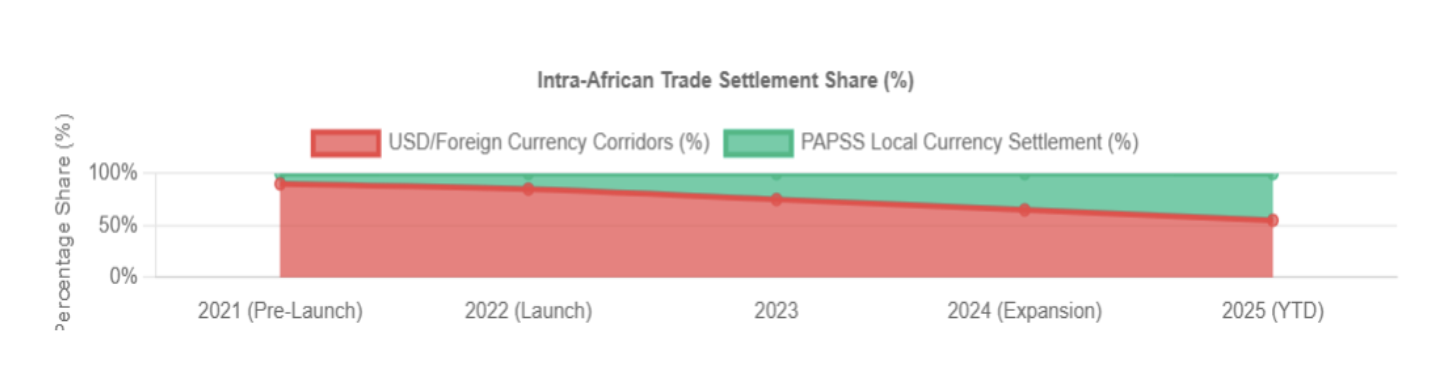

Local-Currency Settlements and Dollar Bypass

By settling in local legal tenders, PAPSS drastically cuts costs and time compared to legacy U.S.-dollar corridors. Internal estimates suggest a $200 million cross-border payment could incur 10–30% in fees under the dollar-based system, whereas using PAPSS in local currencies cuts it to about 1%. Africa could therefore retain an estimated $5 billion annually that would otherwise leak out in foreign exchange fees. Crucially, PAPSS keeps funds on the continent. Before PAPSS, “over 80% of our trade payments” had to route through New York/London bank networks. Now those funds can remain within African banking systems.

2024–2025 Developments and Expansion

PAPSS usage has ramped up significantly. January 2024: Banque Centrale de Tunisie became PAPSS’s first North African member (the 13th overall country) under a new “commercial bank settlement” model. Tunisian officials immediately touted using dinars for intra-African trade to preserve foreign reserves. August 2024: The Central Bank of Comoros joined PAPSS; its launch announcement noted Comorians can now make continent-wide payments “directly in Comorian francs” in ~120 seconds.

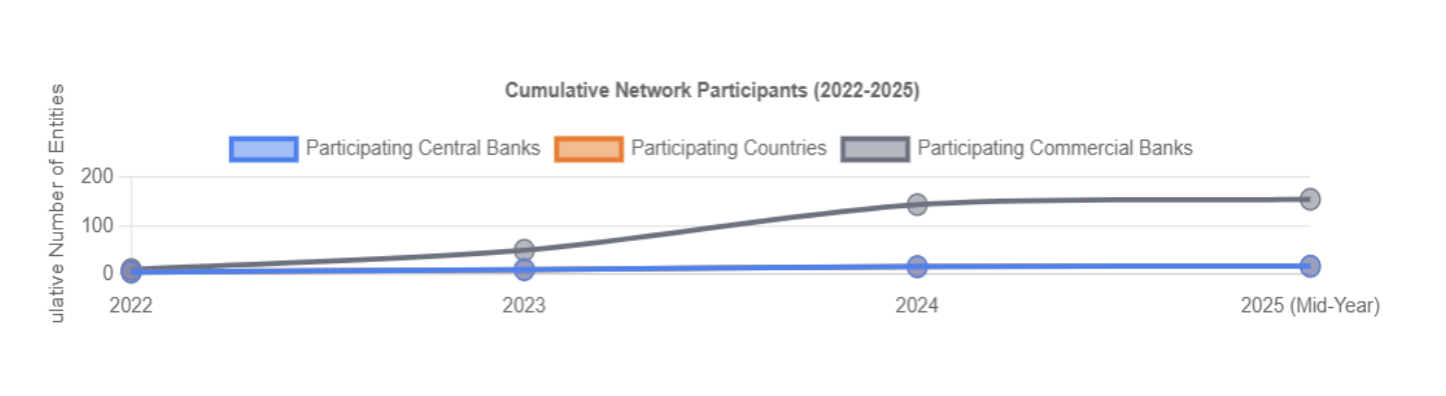

By late 2024, PAPSS had officially onboarded 16 central banks and 144 commercial banks. That year also saw the successful pilot of the PAPSS African Currency Marketplace, which settled transactions in 12 different African currencies. All told, 15+ countries – from West, East, and Southern Africa – will be live by the end of 2024.

2025 (YTD): Adoption has accelerated. By mid-2025, PAPSS connected about 17 African countries and 150+ banks. To boost usage, several member governments have taken new measures. For example, Nigeria’s central bank (April 2025) dramatically streamlined KYC/AML paperwork for PAPSS payments (requiring only basic documents on individual transfers ≤$2,000 and corporate transfers ≤$5,000). This policy explicitly aims to make PAPSS “faster, more cost-effective and more inclusive” for Nigerian businesses under AfCFTA. Also in 2025, PAPSS introduced its African Currency Marketplace commercially (announced July 2025 at the Afreximbank Annual Meeting), enabling a transparent order-book for African FX swaps.

Barriers to True FX Integration

Despite progress, significant hurdles remain to full PAPSS integration and broad adoption:

- Liquidity/pre-funding requirements: PAPSS’s instant settlement relies on banks’ pre-funding their accounts in each local currency corridor. This ties up capital and can strain banks’ liquidity, especially in smaller economies. Many institutions may be reluctant to park large balances without established trust in the system.

- Currency convertibility controls: Numerous African currencies are subject to capital controls or low convertibility. A recent study highlights “currency-convertibility restrictions” as a binding constraint on PAPSS uptake. In practice, corporate funds often get “trapped” because strict FX rules prevent easy cross-border movement of proceeds. (Afreximbank notes, e.g., that over $2 billion in airline revenues are stuck in African currencies due to such controls.)

- Regulatory divergence: PAPSS participants face differing KYC/AML rules and data-localization laws across countries. Researchers warn that inconsistent compliance standards significantly slow cross-border payment system diffusion. Until regulators harmonize these rules (for example, by mutual KYC recognition), commercial banks may find onboarding too complex.

- Infrastructure gaps: Much of Africa remains cash-driven and underbanked, and not all regions have reliable digital payment rails. Limited internet connectivity and legacy banking systems (especially outside major cities) challenge real-time mobile and online PAPSS transactions. Enhancing fintech infrastructure and outreach is still needed in many markets.

- Trust and coordination issues: Some central banks perceive PAPSS as overlapping with national payment projects, raising questions of “ownership and alignment”. Without clear roles, there’s a risk of turf battles or duplication. Moreover, businesses and banks must trust that local currencies will hold value across borders; currency volatility can deter usage. As one expert warned, if central banks don’t cooperate and see PAPSS as complementary, “that tension could slow adoption or limit its effectiveness.”

Together, these barriers underscore why PAPSS adoption has been “patchy and uneven”. Analysts project that without phased FX liberalization, harmonized KYC rules, and a pan-African fintech passport regime, AfCFTA’s digital trade goals may not be fully achieved.

Implications for Central Banks, Commercial Banks, and SMEs

PAPSS’s rise has distinct effects on different stakeholders:

- Central banks: National monetary authorities now act as settlement agents for AfCFTA trade. They must manage pre-funded foreign currency pools and adjust FX policies to accommodate local-currency settlement. In practice, some have eased controls (e.g. Nigeria allowing banks to source FX onshore). Central banks could benefit from better cross-border liquidity and monetary integration, but they also shoulder new responsibilities for system governance. For PAPSS to scale, many experts say central banks must coordinate (e.g., agreeing on common KYC/AML frameworks) and, where possible, liberalize currency regimes.

- Commercial banks: By joining PAPSS networks, banks gain new revenue opportunities (cross-border fees, trade finance) and can offer customers intra-African services in local currency. Several large banks in Nigeria, Kenya, and other pilot countries are already connected. However, banks must integrate PAPSS into their IT and mobile platforms (CBN notes Nigerian banks will embed PAPSS in their apps). They also need to manage FX risk from operating in multiple currencies and ensure sufficient funding. Smaller banks and fintechs may face higher hurdles due to limited capital and expertise.

- SMEs and businesses: The greatest immediate beneficiaries are companies selling across African borders. Lowered paperwork (as Nigeria’s policy did for transfers up to $5k) and near-zero FX fees mean SMEs can trade more freely. A Kenyan trader, for example, can sell to partners in West Africa and receive naira instantly as shillings, without dealing in dollars. This expands market access – essentially turning a 1.3 billion-person continent into their customer base. Early adopters like ZEP-RE (a reinsurance co.) praise PAPSS as “a dream come true” for liquidity. In sum, PAPSS promises to unlock growth for small and medium enterprises by making pan-African commerce as easy as domestic transactions.

Strategic Efforts to Boost Usage and Interoperability

Recognizing these challenges, stakeholders are pursuing multiple strategies:

- Regulatory reforms: Policymakers are simplifying rules to encourage PAPSS use. Nigeria’s April 2025 circular drastically cut the documentation required for small PAPSS transfers. Continental bodies (AU/Afreximbank) are also advocating phased FX liberalization and even a “pan-African fintech passport” to harmonize standards. Such steps would make it easier for banks to operate across borders.

- Liquidity initiatives: The launch of the PAPSS African Currency Marketplace (PACM) directly addresses inconvertibility by pooling liquidity. PACM creates an order-book for African FX, allowing participants to swap currencies peer-to-peer “without passing through hard currencies”. This builds a continent-wide reserve of local currencies, helping to eliminate trapped capital and smooth exchange flows.

- Technology integration: PAPSS is partnering with fintech firms to modernize. The blockchain-enabled PACM (built with Interstellar) improves transparency and speed. Commercial launch of PAPSS in banks’ digital channels is a priority: PAPSS leadership has urged banks to integrate the system into mobile and online banking for wider adoption. APIs and security frameworks are also being developed to connect existing national payment systems (e.g. Kenya’s or Nigeria’s instant payment platforms) into PAPSS.

- Outreach and capacity-building: Governments and Afreximbank have held roadshows, workshops and trade-fair events to educate banks and traders. For example, in August 2024 a PAPSS workshop in Moroni brought together Comoros’s banks to explain system advantages and onboarding procedures. Similar seminars in Ghana and Rwanda have aimed to spur sign-ups. These efforts build awareness and trust, making commercial banks and SMEs more comfortable with the new rail.

- Regional cooperation: African leaders continue to endorse PAPSS. In 2023 the AU Assembly directed Afreximbank to deploy PAPSS continent-wide. Related AfCFTA initiatives (like a “Guided Trade” pilot) plan to use PAPSS for invoicing and settlements. With these mandates, all countries are expected to connect by 2030, creating a truly pan-African payments union.

Country Case Studies and Adoption Insights

- Nigeria: The Central Bank of Nigeria has been proactive. In addition to the April 2025 KYC reforms, the CBN is actively onboarding domestic banks (22 Nigerian banks were live by mid-2025). By empowering banks to source FX locally and streamlining paperwork, Nigeria aims to spur its exporters to “utilise our secure, local currency-based platform” for AfCFTA trade. This model could be replicated by other large economies.

- Tunisia: As the first North African entrant (2024), Tunisia provides a clear example. The BCT joined under a “commercial bank settlement” arrangement that allows Tunisian dinars to be used in PAPSS transfers. Tunisian officials emphasize that this preserves foreign reserves (by avoiding dollar purchases) and strengthens the dinar’s role in regional trade.

- Comoros: This small island began PAPSS in 2024 as part of a development push. Its central bank announced that Comoros now enjoys cross-border payments in Comorian francs, with transactions completed in ~120 seconds at lower cost. Local banks are being urged to connect, which would allow even microfinance clients to engage in intra-African commerce without forex hurdles.

- East Africa (Kenya/Rwanda): Early adopters of AfCFTA trading, these countries are integrating PAPSS for cross-border e-commerce. For instance, Kenya Airways used PAPSS’s currency marketplace to directly swap Naira earnings into Kenyan Shillings without a third currency. Rwanda’s central bank joined PAPSS as of 2024, reflecting the region’s momentum toward digital trade settlement. Kenya is also in the running to host PAPSS’s headquarters, underlining its commitment to the project.

- Regional reach: Beyond these cases, PAPSS spans many sub-regions. Initially rooted in the West African Monetary Zone (Nigeria, Ghana, Gambia, etc.), it now includes Southern and North African members. The growing list of 17–18 countries implies that even formerly fragmented markets are lining up to participate. Each new country (or region) that joins provides another proof-of-concept, encouraging others to follow suit.

Conclusion

PAPSS represents a bold step toward African financial sovereignty. By wiring together 1.3 billion people with a common payments infrastructure, it tackles the continent’s legacy of dollar-based trade and correspondent-banking bottlenecks. Recent data show that PAPSS is gaining critical mass: tens of central banks and well over 150 commercial banks are now connected. Its innovations – like the African Currency Marketplace – directly address continent-wide pain points of convertibility and liquidity.