An Analysis of How the Cedi, Naira, and Rand Performed in H1 2025 Amid Trump’s Tariff Shock

July 14, 2025 by johneb492254456

In the first half of 2025, African currencies navigated a volatile global landscape shaped by shifting U.S. trade policies, fluctuating commodity prices, and evolving domestic reforms. Central to this period was the shockwave triggered by former President Donald Trump’s unexpected reimposition of broad-based tariffs in April 2025, a policy pivot that rattled global markets, disrupted trade flows, and tested the resilience of emerging market currencies.

For Africa’s key economies, Ghana, Nigeria, and South Africa, the tariff shock arrived amid distinct local challenges and macroeconomic transitions. Ghana was in the middle of an IMF-backed recovery, Nigeria continued to push through bold monetary and fiscal reforms, and South Africa faced structural growth constraints while navigating the impacts of elevated public debt and political realignment.

This report provides an in-depth analysis of how the Ghanaian Cedi (GHS), Nigerian Naira (NGN), and South African Rand (ZAR) performed against the U.S. dollar during this turbulent period. Beyond currency movements, we explore a comprehensive set of macroeconomic indicators, including GDP growth, inflation trends, interest rates, fiscal balances, current account dynamics, foreign exchange reserves, credit ratings, investor sentiment, and sectoral developments.

We also unpack the differentiated impact of Trump’s tariff policy on these three economies, highlighting why Ghana’s commodity-heavy export mix largely shielded it from direct tariff exposure, while South Africa’s vehicle and metals sectors faced significant headwinds.

Through this lens, the report offers a country-by-country breakdown, supported by detailed charts and tables, to help analysts, policymakers, and investors understand the drivers behind each currency’s trajectory and the evolving macroeconomic risks and opportunities shaping the region’s financial landscape in 2025.

Ghana: Gold-Driven Recovery and Stabilization

Ghana’s economy rebounded strongly in early 2025. Official data show Q1 2025 GDP growth of +5.3% year-on-year, up from +3.6% in Q4 2024. This outpaced the IMF’s forecast (~4.0% for 2025). Growth was broad-based, led by mining (especially gold, up over 50% exports), construction, and services. The surge in gold exports (≈$11.6 billion in 2024) has driven a current-account swing to a small surplus (~2–3% of GDP annualized). Gross reserves jumped from about $6.0 bn in early 2024 to ~$10.7 bn by April 2025, covering roughly 4.7 months of imports. Inflation remains elevated (≈21% in Apr 2025), but is falling.

On the fiscal side, Ghana is tightening. Despite higher revenues from mining, 2014’s budget slipped: the IMF reports a preliminary primary deficit of about –3.3% of GDP in 2024 (versus a target surplus of +0.5%). The 2025 budget aims for a 1.5% primary surplus, with steep spending cuts flagged by Finance Minister Forson. Debt restructuring and IMF support are key themes: Fitch recently upgraded Ghana’s sovereign rating to B- (stable) as it nears completion of debt relief (S&P likewise moved to CCC+). The upgrade reflects progress on fiscal consolidation and creditor agreements.

Investor sentiment has improved. Local bond/T-bill yields have fallen to multi-year lows (e.g. 91-day T-bill ~15.9% in mid-March 2025). The cedi has recovered and remains stable around GHS 12–13 per USD. A modest currency strength is supported by the large gold windfall and resumed IMF disbursements (USD 370m approved in Apr’25).

Summary (Ghana): Strong commodity exports drove a 5.3% GDP growth in Q1 2025, flipping the current account to surplus. Reserves are high ($10.7 bn) and ratings have been upgraded (Fitch to B-). Fiscal slippage in 2024 leaves a primary deficit (~3.3% GDP), but 2025 targets a surplus. Bond yields are falling, and reform momentum is bolstered by IMF support

Nigeria: Reform Momentum Amid Mixed Signals

Nigeria’s economy shows signs of stability but remains constrained. Official GDP figures for Q1 2025 have been delayed, but Q4 2024 growth was +3.84% (the economy grew ~3.4% in full-year 2024). Analysts expect Q1 2025 growth near 3.8–3.9%, in line with Nigeria’s IMF forecast of 3.0% for 2025. Growth is driven by oil-sector investments and a rebound in agriculture, but high inflation (≈24% in May 2025) and monetary tightening constrain demand.

On the budget front, Nigeria is tightening fiscal policy. The 2025 budget targets a deficit of ~3–4% of GDP (up from very wide deficits in 2023), financed largely by domestic bonds (N13.4 trn) and loans. Oil subsidy removal and lower inflation have eased the financing gap. The IMF notes that reforms (FX liberalization, subsidy cuts, monetary tightening) have markedly improved Nigeria’s external and fiscal position. Although fiscal data are still incomplete, markets are optimistic: Fitch upgraded Nigeria’s sovereign rating to B (stable) in April 2025 and Moody’s to B3 (stable) in May, citing better reserves and fiscal discipline. Nigeria’s debt-to-GDP has jumped (≈55% by 2024), but most borrowing is in local currency, mitigating immediate rollover risk.

External accounts have swung to surplus. Nigeria posted a Q1 2025 trade surplus of ₦5.17 trillion (~$6.7 bn) as oil export receipts rose (+7.4% YoY) and imports cooled (-7.0% QoQ). Oil (62.9% of exports) and agricultural exports are buoyant. Net foreign reserves hit ~$40.2 bn at end-2024 (a 3-year high), partly by reducing central-bank FX swaps. The CBN notes that net reserves (after adjusting for liabilities) have risen sharply, boosting confidence. However, first-quarter 2025 saw a seasonal dip in reserves (due to debt service and FX outflows), though officials expect a recovery in H2.

Investor sentiment is cautiously positive. Nigerian government bond yields have been trending down (average sovereign yield ~18.6% in late June 2025), reflecting easing inflation and scant new bond supply. The March 2025 FGN bond auction was 6x oversubscribed. Meanwhile, the naira has stabilized around ₦750–770 per USD since FX market reforms. Portfolio inflows have risen modestly (some local analysis notes ~$3.8bn net foreign inflows in early 2025).

Sector notes: Oil remains dominant. Nigeria’s OPEC+ quota is pegged at 1.5 mbpd for 2025, limiting output (OPEC decision from late 2024). Falling global oil prices in H1 2025 (Brent $70–80) weigh on receipts. The government aims to boost non-oil growth via gas exports and agriculture (cocoa, rubber). Banking sector reforms (recapitalization, transparency) continue to shore up financial stability.

Summary (Nigeria): Growth is modest (~3–4%), supported by rebounding oil and agriculture. Fiscal austerity (subsidy cuts, tighter budgets) and monetary reform have improved Nigeria’s credit profile (Fitch to B, Moody’s B3). The trade account is in surplus (oil-led), and FX reserves are near 7-year highs. Bond markets are firming (yields falling). Risk remains from high inflation and security issues, but policies are broadly market-friendly.

Summary (Nigeria): Growth is modest (~3–4%), supported by rebounding oil and agriculture. Fiscal austerity (subsidy cuts, tighter budgets) and monetary reform have improved Nigeria’s credit profile (Fitch to B, Moody’s B3). The trade account is in surplus (oil-led), and FX reserves are near 7-year highs. Bond markets are firming (yields falling). Risk remains from high inflation and security issues, but policies are broadly market-friendly.

South Africa: Fragile Growth and High Debt

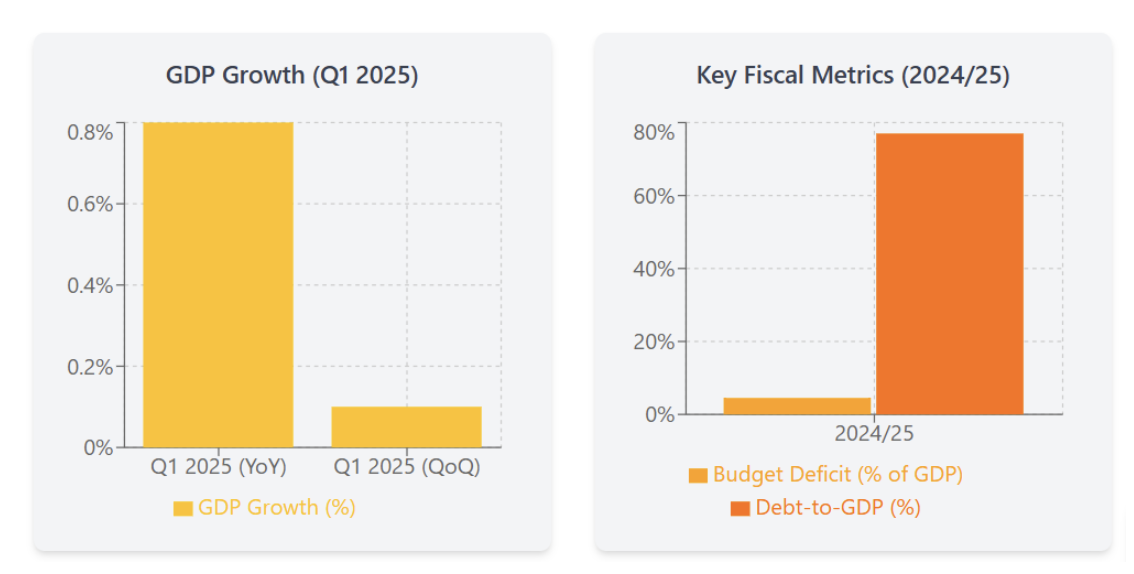

South Africa’s economy remains weak. Q1 2025 GDP grew just +0.8% YoY (+0.1% q/q), barely above stall speed. This reflects a contraction in mining and manufacturing, offset only by a surge in agriculture (+15% YoY). The new coalition government has succeeded in keeping the lights on (uninterrupted power since late 2024), but structural constraints – slow reforms and rising fiscal pressures – limit growth. The IMF sees GDP ~1.0% in 2025, in line with government forecasts.

Fiscal deficits are high. The main budget deficit was roughly 4.5% of GDP in 2024/25, one of the world’s largest for a middle-income country. Debt is rising (~77% of GDP). The May 2025 budget projects narrowing deficits (3.4% by 2027) through spending cuts and a gradual VAT increase, but these are politically sensitive. Revenue has underperformed due to weak growth, and debt service consumes ~20% of revenue. Rating agencies keep South Africa in sub-investment grade: S&P and Fitch at BB- (stable), Moody’s Ba2 (stable), citing heavy debt and reform risk despite some political improvements.

The external position is moderately stable but prone to shocks. In Q1 2025, South Africa ran a current account deficit of ~0.5% of GDP, unchanged from late 2024. Merchandise trade has a small surplus (R221.2 bn in Q1) as exports (minerals, vehicles) roughly match imports. However, services and income outflows widen the overall deficit. Gross international reserves (including gold) are ample (~$68 bn in May 2025), though the core (non-gold) reserves are ~50 bn. The rand is volatile but roughly flat in H1 2025 (≈ZAR 17–18/USD).

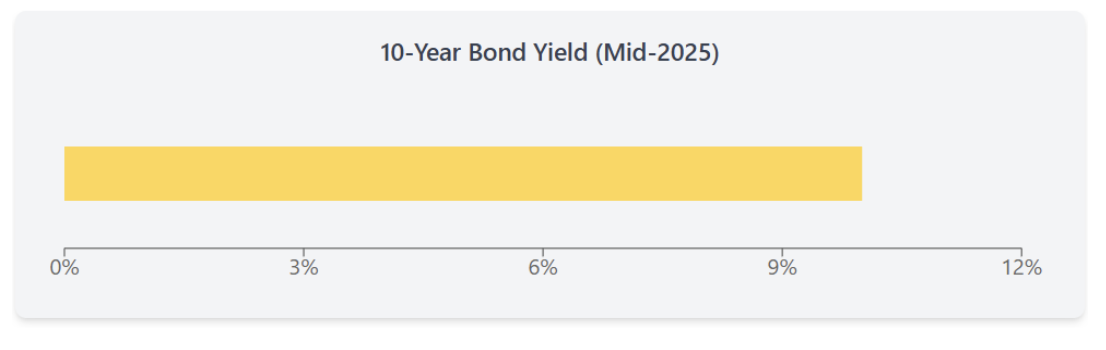

Debt markets demand high yields. South Africa’s 10-year bond yield is around 10% (as of mid-2025), reflecting risk from fiscal widening and global rate uncertainty. Investors are cautious: local institutional funds dominate the debt market, and foreign participation is limited. However, confidence has ticked up on the hope that the coalition government can implement reforms (ratings analysts note that reaching sustained ~2% growth and stabilizing debt would be needed for an upgrade).

Key sectors: South Africa’s exports include minerals (gold, platinum), agricultural products, and automobiles. Notably, vehicle exports to the US (~$2 bn/year) are now hit by Trump’s 25% tariff on foreign cars. More broadly, Trump imposed a 31% tariff on South Africa in Apr 2025 as part of a “reciprocal” tariff list. These duties (also hitting steel, wine, etc.) threaten to erode AGOA preferences and could shave ~0.2–0.3 percentage points off GDP. On the domestic front, long-delayed energy-sector reforms (rail, ports, telecoms) are underway but will take time to yield growth.

Summary (South Africa): Growth is weak (~0.8% in Q1) and fiscal deficits are large (~4.5% of GDP). The current account is nearly balanced, and reserves are high, but debt/GDP is rising. Credit ratings are low (BB-/Ba2), reflecting persistent policy risks. Investor confidence is still fragile, keeping bond yields around 10%. A positive development is a stable power supply, but trade shocks loom: Trump’s steep tariffs (31% on South Africa, including 25% on autos) could cut exports, slow growth, and fuel inflation.

Summary (South Africa): Growth is weak (~0.8% in Q1) and fiscal deficits are large (~4.5% of GDP). The current account is nearly balanced, and reserves are high, but debt/GDP is rising. Credit ratings are low (BB-/Ba2), reflecting persistent policy risks. Investor confidence is still fragile, keeping bond yields around 10%. A positive development is a stable power supply, but trade shocks loom: Trump’s steep tariffs (31% on South Africa, including 25% on autos) could cut exports, slow growth, and fuel inflation.