What Are Stablecoins? Business Starter Guide

June 8, 2026 by diadem445c3650ff Stablecoins are digital currencies that are changing how businesses think about cross-border payments. They offer a faster and more predictable way to move money globally. For businesses, this matters because cross-border payments are often where delays, costs, and uncertainty become most visible. Most times, the impact is felt during something as simple as paying an overseas supplier. The funds are sent, but they are trapped in transit for days. You look at the exchange rate, and it has moved against you. You pay fees, then intermediary fees, then lose even more money in the spread. By the time the funds arrive, part of your profit margin has already disappeared. In this post, we’ll explore what stablecoins are and how businesses can save up to 50% with stablecoins. A stablecoin is a digital asset whose value is linked to another stable asset, often a fiat currency such as the U.S. dollar. Unlike highly volatile cryptocurrencies, they are designed to stay closely pegged, making them perfect for cross-border payments. In addition, stablecoins are also being adopted by businesses that want to reduce payment fees and avoid the hidden costs often associated with traditional cross-border transfers. They are a preferred option for businesses looking for cheaper international transfers without the unpredictability of traditional banking spreads. It means both parties are working with a relatively consistent value. This kind of setup is the reason they are good for business payments rather than trading. It means you get digital transfer speed without the price swings associated with crypto. Stablecoins are digital money designed for stability, fast movement and easy settlement. So how do they really work? First, the stablecoin is created to reflect a reference value. Then, the stablecoin moves around the networks of the blockchain. It can then be exchanged into the local fiat value at any time. What this means for businesses is that each stage directly contributes to stablecoin cost savings by removing unnecessary intermediaries and reducing settlement delays. For high-volume businesses, this shift can translate into as much as 50% savings on international transaction costs, depending on payment routes and frequency. Why do businesses need stablecoins? One of the key reasons businesses adopt them is to reduce payment fees in stablecoin systems by eliminating multiple intermediary banking charges. Businesses care about speed because speed impacts operations. They care about cost because cost impacts the bottom line, and certainty because certainty impacts planning. Stablecoins can support all three. For businesses making cross-border payments, stablecoins trade and settle in shorter timeframes than traditional bank transfers. That can decrease supplier lead times and improve cash flow for contractors and partners. It can also make the payment process feel smoother for teams that handle transfers regularly. Stablecoins can also help to reduce uncertainty. Because stablecoins are created to maintain a stable value relative to an underlying asset, they offer businesses more clarity about how much each payment will actually be worth over time. That makes budgeting, reconciliation, and cash management a lot easier. With stablecoins, businesses can access cheaper international transfers as part of their broader payment optimization strategy. These changes in global payments are driving measurable stablecoin cost savings for businesses that rely heavily on international transactions. Stablecoins add value by solving specific payment pain points: Overall, stablecoins bring in frictionless payment flows that help scale operations without bottlenecks. Compared to legacy systems, stablecoins consistently enable cheaper international transfers by reducing both processing fees and FX inefficiencies. The weaknesses of traditional payment methods become clear in the international business space. On the other hand, stablecoins offer a cleaner path to moving funds across borders. Here is a closer look at how stablecoins perform against traditional transfers: Stablecoins take place on digital tracks with fewer intermediaries, faster and more direct payments than their traditional counterparts. It is a perfect payment option for cross-border businesses. Over time, stablecoin cost savings become more significant for businesses processing frequent cross-border payments at scale. Adopting stablecoins is not just about choosing a digital asset. Businesses also need a secure and reliable way to send, receive, convert, and manage those payments. For many global companies, the shift to digital settlement is not just about speed but about the ability to reduce payment fees that stablecoin infrastructure makes possible at scale. WeWire helps businesses integrate stablecoins into their payment operations without the complexity often associated with blockchain-based transactions. Businesses can send and receive payments using supported stablecoins such as USDT and USDC, convert between stablecoins and fiat currencies, and settle transactions across multiple markets from a single platform. Businesses using platforms like WeWire have seen up to a 50% reduction in cross-border transaction costs compared to traditional banking systems. By combining stablecoin infrastructure with global payment capabilities, WeWire makes it easier for businesses to take advantage of the speed and efficiency that stablecoins offer. In today’s increasingly interconnected world of commerce, fast and reliable sending and receiving of payments is no longer a competitive advantage; it is a competitive necessity. As businesses work towards speedier payment mechanisms, lowered friction and more streamlined international payment processing, stablecoins offer a vital tool. At WeWire, we assist businesses in bridging the gap between traditional finance and modern payment rails. Whether you are looking to pay international vendors, clear interborder invoices, or streamline the payment process for global business transactions, our stablecoin payment solutions enable you to transact with speed, clarity, and trust.

diadem445c3650ff

What are Stablecoins?

How Do Stablecoins Work?

1. Creation of value reference

2. Blockchain transfer

3. Conversion into fiat value

Why Stablecoins Are Useful For Businesses

Stablecoins Increase Payment Speed

Stablecoins Increase Payment Certainty

Where Stablecoins Fit In A Real Payment Flow

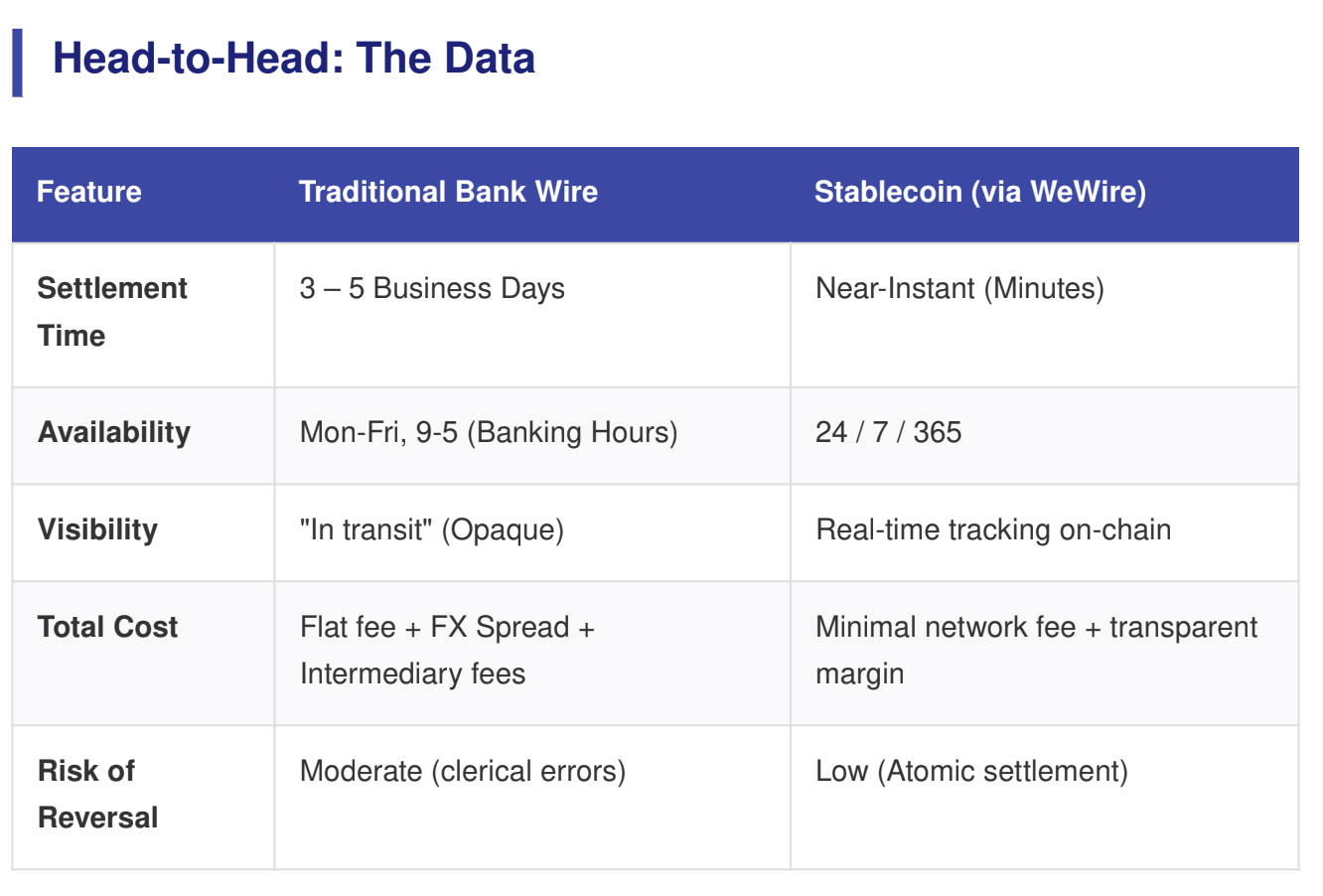

Stablecoin Payments vs Traditional Transfers

Traditional Transfers

Stablecoins

How WeWire Helps Businesses Adopt Stablecoins

Final Takeaway

How to Send & Receive Stablecoins for Your Business with WeWire

June 8, 2026 by diadem445c3650ff If you are reading this, then you are fully aware of how frustrating and inefficient, not to mention time-consuming and expensive, it is to send money internationally via traditional banks. You want to know how stablecoins work and how they can impact your business operations. In this guide, we will walk you through exactly how to send stablecoins for your business and receive stablecoins for your business using WeWire. We’ll cover what the stablecoin payment process looks like from start to finish, which stablecoins make the most sense for B2B use, common pitfalls to avoid, and how WeWire sits at the centre of it all Getting your business set up correctly at the start saves you from headaches later. Here is a quick checklist of everything you need to send and receive stablecoins with Wewire: WeWire handles the regulatory complexity on its end, but your business should also ensure internal records are in order, especially for high-value transactions. Read our guide on Stablecoin AML/KYC: What Businesses Need to Know for a full breakdown. The stablecoin payment process on WeWire is designed to be fast and straightforward. Here’s how to send stablecoins for your business from start to finish: Log in to your WeWire business account. On your WeWire dashboard, you can get the latest wallet balance of all currencies and stablecoins. Fund stablecoins in your WeWire account. If there are not enough stablecoins in your WeWire wallet, you can fund your stablecoins wallet by either: Converting the fiat held in your WeWire account (USD, EUR, GBP) to USDT or USDC, or by depositing stablecoins to the WeWire wallet address from an external wallet. Click “send” and choose stablecoin. Then select the type of stablecoin you are sending (USDT or USDC) and the amount, as well as the network. TRON (TRC-20) is generally the quickest and cheapest network for many of the corridors, while Ethereum is preferred in some regulated institutional contexts. Paste in your receiver’s wallet address accurately. WeWire provides an address verification; please utilize it. If the receiver’s wallet address is entered incorrectly, the funds are lost. No ‘reverse wire’ on blockchain! You will see all details regarding the transaction, including the amount, network, estimated fee, and receiver’s wallet address. Press ‘confirm’ and the stablecoin transaction will be initiated immediately. You can track the transaction in real-time from your WeWire account. You may share the transaction hash with your counterparty, who will be able to view the received payment on the blockchain. Both parties get transaction transparency without calls to the bank! If a supplier, client, or partner wants to pay you in stablecoins, receiving stablecoins for your business is even simpler than sending. Step 1: Locate Your WeWire Wallet Address Log into your WeWire dashboard and then your stablecoin wallet. You’ll find a unique deposit address for each supported network and stablecoin pair. Step 2: Send The Right Address and Network Details Share your wallet address along with the network with the paying party. This needs to be explicitly stated, as many B2B stablecoin payment errors happen when someone attempts to send USDT on the TRC-20 to an ERC-20 address, and the payment is irrevocably lost. Step 3: Monitor Payment Confirmation In Real Time Once your paying party sends you money, you can track the confirmation on the blockchain in real time directly on your WeWire dashboard. There is no more waiting until the ‘end of day clearing’. There is no calling your bank at 4:58 PM. Step 4: Convert or Spend As soon as it has arrived, your stablecoins are fully under your control. Hold them in your WeWire wallet, exchange it into local fiat currency, withdraw them to your linked bank account, or use them to pay your next vendor. This is possible due to WeWire’s multi-currency infrastructure that ensures the stablecoins you receive for your business do not just sit idle – they can be used to fuel your next payment out. Even a smooth, stablecoin payment process can go sideways when these basics are missed: Wewire offers users a payment confirmation process to ensure these mistakes are avoided. Once you understand the process, you can send and receive payments without any glitches using WeWire. WeWire was created to be an easy, operational way to send stablecoins for your business, or to receive stablecoins for your business, without needing your finance team to become blockchain specialists. All of this lives in a single, compliance-grade dashboard where you get: From a regional importer paying a Shenzhen manufacturer to a fintech managing hundreds of thousands of B2B payments monthly, to a services company billing international clients, WeWire gives you the infrastructure to receive stablecoins for your business consistently and send stablecoins for your business smoothly at a cost and speed that banks simply can’t compete with. Create and send stablecoin invoices that are payable in stablecoin, making it frictionless to bring both your clients and suppliers to stablecoin payments. With Wewire, stablecoin payment becomes smooth, easy, and straightforward. Once you have processed your first transaction and seen it reflected in under 2 minutes and with complete transparency, your question moves from ‘Should I use stablecoins?’ to ‘Why was I ever using bank wires?’ Send and receive stablecoins for your business. Through a platform that takes care of the compliance, coverage, and infrastructure, allowing you to concentrate on your business. WeWire.

diadem445c3650ff

What Do You Need To Send & Receive Stablecoins for Your Business with WeWire

How to Send Stablecoins for Your Business with WeWire

Step 1: Log in to your WeWire account.

Step 2: Fund your account.

Step 3: Send via Wewire

Step 4: Add Receiver’s Wallet Address

Step 5: Review and Send

Step 6: Track your transaction

How to Receive Stablecoins for Your Business with WeWire

Mistakes Businesses Make in the Stablecoin Payment Process

Mistake

Why It’s Costly

How to Avoid It

Wrong network selected

Funds sent to the wrong network can be unrecoverable

Always confirm the network with the counterparty before sending

Sending to a wrong/mistyped address

Blockchain transactions are irreversible

Use copy-paste, not manual entry.

Ignoring network congestion

Can slow settlement on Ethereum during peak times

Use TRC-20 for time-sensitive, high-frequency payments

Not keeping transaction records

Creates compliance and audit problems

Download and file transaction histories monthly

Confusing stablecoins with volatile crypto

Budgeting errors if you treat USDT like BTC

Stablecoins are pegged 1:1 to USD. Treat them like digital cash

Send and Receive Payments with WeWire

In Summary

Beyond the Swift: Why Businesses Are Choosing Stablecoins for Global Reach

June 7, 2026 by diadem445c3650ff You know that feeling if you’ve ever tried to send an international wire out at 4 PM on a Friday. The money goes into a black box of correspondent banks, time zones, and processing windows, and reappears on Tuesday, or “we’ll look into it.” For a business that needs to move at lightning speed across borders, SWIFT is less a payment network and more of a waiting room. That’s why the debate around stablecoins for global business has officially left the realm of fintech buzzwords and entered the world of the treasury department. African importers, Asian exporters, and European fintechs alike are reimagining the way they transfer money internationally – with stablecoins at the heart of the new architecture. The only question is, will you be leading this transition or lagging behind it? In the rest of this post, we will look into why businesses are choosing stablecoins for their cross-border payments and how you can also make that switch. Let’s get real about the behind-the-scenes operations of traditional banking infrastructure: Here’s the part that stings most: when you send your vendor $50,000 in wire, there’s a good chance you’re getting stung an additional $1,500 or more for FX spreads and interbank fees. It doesn’t appear as a line item on an invoice. It just evaporates from your profit. Now, imagine that over the course of a year of global payments. It starts adding up. The Financial Stability Board has noted that cross-border payments struggle with cost, speed, access, and transparency. SWIFT adjustments can only do so much to resolve a fundamentally structural issue. How do stablecoins work for businesses internationally? It boils down to a totally different model that makes stablecoins for global business an outstanding alternative. Instead of being passed from bank to bank through an intermediary chain, a stablecoin transaction is an on-chain, direct transfer that’s pegged 1:1 to fiat currencies, like the USD, and takes seconds to settle. What’s more? It works all day, every day. So how does that impact a global business? Transactions are finalized on the blockchain in under 15 seconds. A long way from the 3 to 5 days it can take to transfer funds through the banks. Sending funds on-chain costs fractions of a cent. Plus, when combined with competitive FX rates, we consistently see businesses save at least 10% on international payment costs. Banking hours? “Next business day”? Nope! A transfer made at 11:45 PM Sunday arrives at its destination before midnight. With on-chain tracking, you know exactly where your money is every second of the way. This is where stablecoins truly shine. While other cryptocurrencies fluctuate in value, stablecoins maintain their value. It means if you send $10k in USDT, $10k arrives. Price fluctuation during transit is no longer an issue. When it comes to sending money across borders, stablecoins are uniquely capable of fixing the problems banks just accept as “how it is.” If the numbers from 2025 and 2026 are any indication, stablecoins have arrived, and they are taking over. According to Rapyd’s 2026 State of Stablecoins Report, 34% of businesses are already using stablecoins, with another 48% planning to do so over the next 12 months. The top reason? Faster payments (72%), followed by ease of cross-border transactions (62%). What’s even more significant? B2B payments make up close to 97% of the stablecoin volume across major stablecoin platforms. A dramatic increase from just 36% in 2023, which signals a clear move towards enterprise-ready, business-centric stablecoin usage. At the end of the day, this is no longer a crypto conversation but a finance operations conversation. And for businesses already on stablecoins, cost savings are substantial. EY-Parthenon research from June 2025 found that 41% of corporates have achieved at least a 10% reduction in cross-border B2B payments. But for businesses in or trading with emerging markets, the benefits are even more profound. Companies that may not have a US banking relationship can achieve dollar-denominated stability with stablecoins, which is particularly advantageous for businesses in or trading with emerging markets like Africa, Southeast Asia, and Latin America. This is where WeWire comes in. WeWire offers a cross-border payment solution for businesses operating internationally, enabling businesses to pay with stablecoin and fiat rails. WeWire’s network has you covered in over 100 countries, which you won’t find with most banks’ cross-border solutions. From paying suppliers in Vietnam to receiving invoices from the UAE or even collecting from a UK client, WeWire’s corridor is there. Hold, convert, and send payments in various currencies in over 13 currencies (USD, GBP, EUR, GHS, NGN, TZS, XAF, XOF, UGX, USDT, USDC) all from one interface: no more lost time or duplicated efforts in managing separate accounts. WeWire leverages stablecoins directly into its payment workflow and bypasses the complexity of a separate crypto platform, providing companies with the cost benefits and speed of blockchain settlement without demanding the crypto know-how of your staff. It feels like banking, but the speeds are unmatched. ISO 27001 certified, regulated in various regions, and adheres to strict KYC/AML policies. Stablecoins are only sustainable for global business use if backed by an institutionally regulated platform. If you’re dealing with large volumes of money, WeWire’s over-the-counter (OTC) desk is open around the clock for customized support and competitive rates. WeWire’s answer is a single platform that combines the coverage of a global payments network with the speed and efficiency of stablecoin settlement. See how WeWire is cutting international transaction costs for businesses and what that looks like in real numbers for your bottom line. SWIFT will not disappear in a day. However, companies that are building for the future are not waiting for SWIFT to catch up. The future of global business stablecoins has shifted from a “curious experiment” to an “operational infrastructure,” and data from 2025 and 2026 illustrate this point better than a thousand sales pitches ever could. If your business is moving money internationally, paying suppliers, settling invoices, or operating in multiple currencies, then the question is not when you should investigate better international payment alternatives, but how long you can afford to be without one. WeWire offers your business the speed, coverage, and worldwide payment reach that you can not afford to wait for. Create your WeWire account today and see what your payments look like when the rails actually work for you.

diadem445c3650ff

What SWIFT Is Really Costing You

Pain Point

Reality

Settlement time

1 to 5 business days, often more.

Fees

$25 to $50 flat with 1 to 3% FX spread per transaction

Correspondent banks

Each one takes a cut before funds arrive

Availability

Business hours only. Weekends and holidays excluded

Transparency

Low. Funds can be “in transit” with no real-time visibility

Why Stablecoins Work and Why Businesses Are Paying Attention

Speed

Cost

Availability

Transparency

Stability

The Numbers That Are Moving Boardroom Conversations

WeWire: Built for the Global Business That Can’t Afford to Wait

Global Coverage (100+ countries)

Multi-currency Wallet

Stablecoin Native Infrastructure

Compliance Driven

24/7 OTC Desk

In Summary

Stablecoins vs. Bank Wires: The Real Cost & Speed for Business

June 1, 2026 by diadem445c3650ff In the world of global commerce, “the check is in the mail” has been replaced by “the wire is in flight.” But for many finance teams, that flight feels less like a modern jet and more like a hot air balloon—slow, unpredictable, and subject to the whims of every passing breeze (or intermediary bank). As businesses scale across borders, the friction of moving capital becomes a silent killer of growth. At WeWire, we talk to CFOs daily who are frustrated by the lack of transparency in international wire transfer speed and the sheer opacity of bank transfer fees. The conversation is shifting. It’s no longer just about how we send money; it’s about whether the legacy rails we’ve used for fifty years are still fit for purpose. Enter the stablecoin. When you initiate a traditional bank wire (SWIFT), you aren’t just sending money from Bank A to Bank B. You are navigating a relay race. Because most banks don’t have direct relationships with every other bank on earth, they use “correspondent banks.” Each runner in this relay takes a small “handling fee” out of the principal before passing it on. The advertised flat fee (often $35–$50) is rarely the total cost. The stablecoin vs bank wire debate starts here. A business might lose 1% to 3% on the FX spread alone. If you are moving $100,000 to pay a manufacturer in Vietnam, a 2% spread is a $2,000 “ghost fee” that never appears on an invoice but vanishes from your bottom line. 2. The Speed Trap Traditional international wire transfer speed is governed by “business days” and “banking hours.” If you send a wire on Friday afternoon from New York to Singapore, it effectively disappears into a black hole until Monday morning. For a supply chain that depends on “Just-in-Time” delivery, a three-day delay in payment confirmation can mean a week-long delay in shipping. “Efficiency isn’t just about saving a few dollars on fees; it’s about capital velocity. Money sitting in a correspondent bank’s ‘pending’ queue is dead capital.” Stablecoins, like USDC or USDT, are digital assets pegged 1:1 to a fiat currency (usually the USD). They live on the blockchain, which operates 24/7/365. When comparing stablecoin vs bank wire, the fundamental difference is architecture. One is a series of ledger updates across multiple private entities; the other is a single, instant cryptographic transfer on a public or semi-public rail. Consider GlobalGoods Inc., a mid-sized electronics distributor. They need to secure a limited batch of components from a supplier in Dubai. Using a bank wire, they initiate the transfer on Tuesday. The supplier sees the funds on Friday. By then, the stock is gone. With WeWire’s stablecoin integration, GlobalGoods Inc. sends the payment. The transaction hits the blockchain and is confirmed within minutes. The supplier receives a notification, locks in the inventory, and ships the same day. That is the competitive advantage of speed. While the benefits of stablecoins are clear, many businesses hesitate because of the perceived complexity. This is where WeWire comes in. We don’t just provide a “crypto wallet”; we provide a sophisticated financial interface that makes stablecoins feel like the banking experience you’re used to, just better this time. One major hurdle for businesses is the “compliance gap.” Traditional banks are terrified of crypto, and for good reason, regulation has been a moving target. WeWire bridges this by maintaining rigorous KYC (Know Your Customer) and AML (Anti-Money Laundering) standards. When you use WeWire, you get the speed of the blockchain with the institutional-grade security of a Tier-1 financial service. In a bank wire, settlement is “probabilistic”—you hope it gets there. In a stablecoin transfer via WeWire, settlement is “deterministic.” The math is simple: For a CFO managing cash flow, reducing that variable from days to minutes changes everything from liquidity planning to vendor relationships. We are entering an era of “Real-Time Finance.” As consumer payments (like Venmo or Pix) become instant, B2B payments can no longer afford to be the laggard. The bank transfer fees you pay today aren’t just line items; they are a tax on your ability to compete globally. Transitioning to stablecoin-based settlements doesn’t mean abandoning your bank. It means adding a high-performance engine to your treasury department. It means knowing that when you hit “send” at 10 PM on a Sunday, your partner across the globe is getting paid at 10:05 PM. Ready to upgrade your capital velocity? Stop waiting for the “next business day.” Discover how WeWire can slash your international transfer times and eliminate hidden fees today.

diadem445c3650ff

The Legacy Wall: Understanding the Real Cost of Bank Wires

Stablecoins: The Digital Highway

Real-World Use Case: The Agile Importer

The WeWire Difference: Bridging the Two Worlds

Compliant & Secure

Direct Comparison: Settlement Logic

Why Now? The Cost of Inaction

Instant Settlements: The Business Impact of Fast Stablecoin Payments

April 20, 2026 by diadem445c3650ff It’s 4:47 p.m. on a Friday. Your supplier in Singapore is waiting for payment before releasing a shipment. Your bank confirms the wire has been sent—but it may take two to three business days to clear due to correspondent banking checks and time zone differences. The shipment doesn’t leave the warehouse. The weekend passes. Your inventory stalls. Your customers wait. Your working capital tightens. Now imagine the same scenario—but this time, payment settles in seconds, not days. That’s the power of instant stablecoin payments. And for modern businesses navigating global markets, the impact goes far beyond convenience. It reshapes liquidity, accelerates growth, and redefines how cross-border commerce works. In this article, we explore how stablecoins for fast settlements are transforming international payments—and why forward-thinking companies are moving toward fast cross border payments as a strategic advantage. Traditional cross-border payments rely on legacy systems like SWIFT and correspondent banking networks. While they’ve supported global trade for decades, they were never built for today’s 24/7 digital economy. On average: But speed doesn’t just signify convenience, it signifies capital efficiency. When funds are “in transit,” they are effectively frozen. For businesses operating on tight margins or rapid growth cycles, delays directly impact: In a world where Amazon delivers in 24 hours and SaaS platforms deploy in seconds, waiting days for money to move feels increasingly outdated. So, how exactly do stablecoins bypass the waiting room? The answer lies in the removal of the “validation chain.” In a traditional transfer, several banks must manually reconcile their ledgers to agree that money has moved. With fast cross-border payments powered by stablecoins, the blockchain acts as a single, shared ledger. When you send USDT or USDC via WeWire, the network validates the transaction nearly instantly. There is no “middleman” who needs to wake up and click “approve.” The global economy never sleeps, but banks do. Stablecoin networks operate every second of every day. Whether it’s 2 AM on a Sunday or a public holiday in Lagos, the stablecoin settlement speed remains constant. One of the biggest time-wasters in international trade is “proof of payment.” Traditionally, a buyer sends a PDF receipt, and the seller waits days for the funds to actually hit the account. With stablecoins, the transaction hash provides immutable, real-time proof. The moment the transaction is confirmed on-chain—usually within seconds—both parties can see it. At WeWire, we see the transformative power of instant stablecoin payments across various sectors every day. An e-commerce aggregator in Johannesburg uses WeWire to pay multiple suppliers in Southeast Asia. By utilizing instant settlements, they can operate a “just-in-time” inventory model. Instead of keeping millions tied up in stock, they pay for goods the moment an order threshold is met. The stablecoin settlement speed ensures the goods are packed and shipped the same day, drastically reducing the cash-conversion cycle. A software agency in Cairo employs developers across three continents. Previously, the administrative burden of ensuring everyone was paid on time—despite varying bank holidays—was a full-time job. By switching to WeWire, they now execute payroll in a single batch. Funds reach the developers’ digital wallets in seconds, improving employee morale and reducing administrative overhead by 40%. WeWire was built with a singular focus: removing the friction from global finance. We don’t just provide access to stablecoins; we provide a high-performance dashboard designed for business leaders who value their time. Speed as a Strategic Asset As we look toward the end of 2026, the gap between “fast” and “slow” companies will continue to widen. In an environment where inflation can fluctuate and supply chains remain fragile, speed is the ultimate hedge. Businesses that adopt stablecoins for fast settlements are doing more than just saving on bank fees; they are building a more resilient, responsive treasury. They are the companies that can pivot to a new supplier in an afternoon or capitalize on a flash sale of raw materials while their competitors are still waiting for a bank manager to sign off on a wire transfer. The technology exists today to move value as easily as we move information. There is no longer a logical reason for a $50,000 payment to take longer than a 50-kilobyte email. By integrating instant stablecoin payments into your operations through WeWire, you are reclaiming your time, your capital, and your peace of mind. You are ensuring that your business is ready for a world where “business days” are a thing of the past and “instant” is the only acceptable speed. Are you ready to accelerate your business? Book a 15-minute demo with the WeWire team and see how our “seconds, not days” settlement can transform your global operations.

diadem445c3650ff

The Hidden Cost of Waiting

How Stablecoins Achieve “Seconds, Not Days”

1. Direct Peer-to-Peer Settlement

2. The 24/7/365 Financial Rail

3. Automated Confirmation

The Business Impact: Real-World Use Cases

Case Study: The “Just-in-Time” Importer

Case Study: The Global Remote Team

Why WeWire is the Engine for Instant Settlement

The WeWire Difference:

Conclusion: Stop Waiting for Your Own Money

How Stablecoins Cut International Transaction Costs & Boost Profits

April 16, 2026 by diadem445c3650ff Consider Kofi, the CEO of a fast-growing electronics distribution firm in Accra. Kofi recently secured a contract to import a massive shipment of high-end components from a supplier in Shenzhen. The deal was lucrative, but the logistics of the payment were a nightmare. Through his traditional bank, the “hidden” costs started piling up: a 3% currency conversion spread, a $50 flat wire fee, and an additional 2% lost to intermediary bank charges. To top it off, the funds took six days to arrive, during which the exchange rate shifted, costing him another $1,200 in purchasing power. By the time the supplier was paid, Kofi’s profit margin on the entire shipment had shrunk by nearly 8%. Kofi’s story isn’t unique; it is the daily reality for thousands of businesses across Africa and emerging markets. But as we move through 2026, a new financial rail has emerged. By using stablecoins, businesses are no longer just “sending money”—they are reclaiming their profits. In this post, we’ll explore how you can reduce payment fees with stablecoins and why moving away from legacy banking is the fastest way to boost your bottom line. Traditional international transfers (SWIFT) were designed in the 1970s. They rely on a “correspondent banking” model, where money bounces through multiple banks before reaching its destination. Each “hop” adds a fee and a delay. According to the World Bank, the global average cost of sending cross-border payments remains stuck near 6.25%. For many African corridors, that number can soar above 10%. Stablecoins like USDT and USDC change the math entirely. Because they operate on blockchain networks (like Tron or Ethereum), they bypass the “middlemen” of the 1970s. When you send a stablecoin payment via WeWire, the transaction goes from Point A to Point B directly on the ledger. There is no “correspondent bank” in the middle to shave off a fee. This alone can result in cheaper international transfers by removing 2-3 layers of hidden costs. One of the biggest “gotchas” in traditional banking is the lack of transparency in exchange rates. You often don’t know the final rate until the money arrives. Stablecoins allow for stablecoin cost savings through real-time, transparent pricing. On WeWire, you see the exact conversion rate from your local currency (like NGN or KES) to USDT before you hit “send.” No surprises, no “hidden markups.” On modern blockchains, the cost to move $100 is often the same as the cost to move $1,000,000. While a bank might charge a percentage-based fee that scales with your business growth, blockchain “gas” or network fees are nominal. This shift from percentage-based pricing to flat, low-cost pricing is a game-changer for high-volume importers and exporters. At WeWire, we don’t just talk about savings; we quantify them. Our data from 2025 shows that businesses switching from traditional banking to our stablecoin-powered rails saved an average of 50% to 80% on total transaction costs. Let’s look at a typical $50,000 international payment for a manufacturing company: By saving $1,200+ on a single transaction, that manufacturer just added 2.4% back to their net profit margin. Scale that across 12 months of operations, and the stablecoin cost savings could fund a new warehouse, a bigger marketing budget, or an expanded product line. While nearly every business with cross-border needs can gain from stablecoin payments, certain use cases are especially compelling: Companies dealing with international suppliers or customers can slash payment processing costs and improve predictability. Recurring billing across borders often incurs repetitive foreign exchange and settlement fees. Stablecoins reduce those overheads. With a global workforce, stablecoin payments can ensure faster and cheaper payouts across jurisdictions. For businesses scaling quickly, every percentage point saved on payment fees directly boosts runway and profitability. WeWire makes it easy to capture these savings without needing to be a blockchain expert. We bridge the gap between your local bank account and global stablecoin liquidity. Our platform is designed to handle the complexity of the backend so that your dashboard shows one thing: a successful, low-cost transaction. In 2026, high transaction fees are a choice, not a necessity. The businesses that will dominate the next decade are those that treat their payment infrastructure with the same innovation they apply to their products. By choosing to reduce payment fees with stablecoins, you aren’t just saving money, you are optimizing your cash flow, strengthening supplier relationships, and protecting your hard-earned margins.

diadem445c3650ff

The Invisible Tax: Why Traditional Transfers are So Expensive

Where the money goes:

The Stablecoin Solution: High-Speed, Low-Cost Infrastructure

1. Eliminating Intermediary Banks

2. Radical Transparency in FX

3. Near-Zero Network Fees

Quantifying the Savings: The WeWire Effect

The “Profit Boost” Breakdown

Fee Category

Traditional Bank Wire (Estimated)

WeWire (USDT/USDC)

Outward Wire Fee

$50 – $100

$0 (Platform flat fee)

FX Spread (approx. 3%)

$1,500

Competitive Mid-Market

Intermediary Bank Fees

$30 – $75

$0

Time to Settle

3-5 Business Days

< 10 Minutes

Total Estimated Cost

$1,600+

Significantly Lower

Who Benefits Most from Stablecoin Payments?

1. Exporters & Importers

2. SaaS & Subscription Platforms

3. Remote Payroll & Contractor Payments

4. Startups & Scale-ups

Integrating WeWire into Your Workflow

Conclusion: Don’t Let Legacy Fees Stifle Your Growth

Understanding Stablecoin AML/KYC: What Businesses Need to Know

April 13, 2026 by diadem445c3650ff In the fast-moving world of global trade, speed is often cited as the ultimate competitive advantage. But for the modern CFO or business owner, speed without security is just a faster way to run into a brick wall. As we navigate through 2026, the global stablecoin market has matured into a financial powerhouse, processing trillions in annual volume. However, this growth has brought a sharper focus from global regulators. The days of the “digital Wild West” are over. Today, the bridge between local operations and global markets is built on a foundation of financial compliance for stablecoins. At the heart of this foundation are two acronyms that every business leader must master: KYC (Know Your Customer) and AML (Anti-Money Laundering). While these terms might sound like bureaucratic hurdles, they are actually the “safety belts” of digital finance. In this post, we’ll break down what stablecoin AML and stablecoin KYC mean for your business and why WeWire’s rigorous commitment to these standards is your greatest asset. For years, many businesses viewed digital assets as a way to “bypass” the traditional banking system. While blockchain does offer a bypass for delays and high fees, it is no longer a bypass for accountability. According to recent data from the Financial Action Task Force (FATF), over 85% of major economies have now implemented strict regulatory frameworks for virtual assets. In 2025 alone, global enforcement actions against non-compliant crypto platforms reached a record high, signaling that regulators are no longer looking the other way. For a business, using a non-compliant platform isn’t just a “tech risk”—it’s a legal one. If your funds are processed through a pipeline that lacks proper stablecoin AML controls, those funds risk being flagged, frozen, or rejected by your local bank or international partners. Simply put, these are the digital versions of the due diligence performed by traditional banks, optimized for the speed of the blockchain. KYC is the process of verifying the identity of a client. For WeWire, this is more accurately called KYB (Know Your Business). While KYC is about who you are, AML is about what you are doing. Stablecoin AML refers to the continuous monitoring of transactions to detect and prevent suspicious activity. By 2026, the “Travel Rule” has become a cornerstone of financial compliance for stablecoins. This rule requires Virtual Asset Service Providers (VASPs) to share specific originator and beneficiary information for transactions over a certain threshold. For your business, this means that a transaction via WeWire carries the same “trust signals” as a traditional bank wire, but without the three-day waiting period. It ensures that when your supplier receives USDT or USDC, their local financial institution can see that the funds came from a verified, compliant source. At WeWire, we don’t view compliance as a “box-ticking” exercise. We view it as risk management as a service. Here is how our commitment to these standards protects your bottom line: Banks are naturally risk-averse. One of the biggest challenges for businesses using digital assets is the risk of having their traditional bank accounts closed or flagged. Because WeWire operates with a Payment Service Provider (PSP) License and maintains institutional-grade stablecoin KYC protocols, we act as a “clean” bridge. When you move funds through WeWire, you are moving them through a regulated pipeline that banks recognize and respect. On the blockchain, the history of a token is public. If you use an unregulated P2P (peer-to-peer) platform, you might inadvertently receive “tainted” tokens—stablecoins that were previously involved in a hack or a scam. These tokens can be blacklisted by issuers like Tether or Circle. WeWire’s stablecoin AML monitoring ensures that every token you interact with on our platform is “clean,” protecting your capital from being frozen by protocol-level blacklists. For a CFO, the nightmare of using digital assets is often the audit trail. WeWire provides comprehensive, audit-ready records of every transaction, including the KYC/AML status of the counterparties involved. This transparency makes month-end reconciliation and annual audits a breeze rather than a headache. In Sub-Saharan Africa, where stablecoin usage grew by over 40% in 2025, the demand for these tools is driven by the need for currency stability. But stability isn’t just about the $1.00 peg; it’s about the stability of the platform you choose. When you choose a partner that prioritizes financial compliance for stablecoins, you are choosing a partner that is built to last. Unregulated platforms often vanish or get shut down by authorities, leaving business funds in limbo. WeWire’s “compliance-first” approach is our promise to you that we will be here to facilitate your trade today, tomorrow, and ten years from now. The future of B2B payments is on the blockchain, but the ticket to entry is compliance. By embracing stablecoin AML and KYC, businesses aren’t just following rules—they are building the trust necessary to scale across borders with confidence. At WeWire, we handle the complexities of global regulations so you can focus on what you do best: growing your business. We’ve built the most secure, compliant, and efficient payment rail in the market, because we believe your money deserves nothing less. Is your business ready for compliant, instant global payments? Sign up for a WeWire Business Account and experience the peace of mind that comes with institutional-grade security.

diadem445c3650ff

The Shift: Why Compliance is Non-Negotiable in 2026

What is Stablecoin KYC and AML?

1. Stablecoin KYC (Know Your Customer/Business)

2. Stablecoin AML (Anti-Money Laundering)

The “Travel Rule”: The New Global Standard

Why WeWire’s Compliance Shield is Your Competitive Edge

1. We Protect Your Banking Relationships

2. We Prevent “Tainted” Funds

3. We Facilitate Seamless Global Audits

Beyond the Tech: The Human Element of Trust

Conclusion: Compliance is the Key to Scaling

Choosing a Compliant Partner: Why WeWire Prioritizes Trust in Stablecoin Payments

April 10, 2026 by diadem445c3650ff For years, the conversation around digital assets in Africa was dominated by two extremes: the “get-rich-quick” hype of speculative trading and the “Wild West” fear of an unregulated frontier. But as we move through 2026, the narrative has shifted. The data tells a clear story: In Sub-Saharan Africa, stablecoins accounted for 43% of total crypto transactions in 2024, with roughly $54 billion in value processed. This isn’t speculation; it is utility. Businesses across the continent are betting on stablecoins to solve the very real, very expensive problems of currency volatility and broken cross-border payment rails. However, as utility grows, so does the responsibility of the platforms facilitating these moves. At WeWire, we understand that for a business owner in Accra or a CFO in Lagos, the primary concern isn’t “how fast is the blockchain?” It’s “is my money safe, and am I compliant?” A compliant stablecoin platform is a system that meets applicable financial regulations to enable secure, transparent cross-border transactions. It implements risk-based KYC, AML/CFT controls, and sanctions screening; follows Travel Rule obligations where applicable; maintains robust recordkeeping and audits; and provides transparent reserves and reporting to maintain trust and reliability. When you use WeWire for secure stablecoin transactions, you aren’t just sending “crypto.” You are moving value through a regulated pipeline. To ensure safety, we focus on three pillars of trust: Trust without a license is just a promise. We are proud to announce that WeWire has secured its Payment Service Provider (PSP) License. In a landscape where many operate in “gray areas,” we chose the path of full regulation. This license means we operate under the oversight of financial authorities, adhering to strict capital requirements and operational standards. Compliance isn’t a hurdle; it’s a shield. Every business that joins WeWire undergoes a robust Know Your Customer (KYC) and Anti-Money Laundering (AML) process. Why does this matter to you? Because it ensures that when you receive funds, they aren’t “tainted” by illicit activity. It protects your business from the legal and reputational risks associated with unregulated peer-to-peer (P2P) transfers. We partner with issuers who prioritize transparency. By facilitating transactions primarily in top-tier stablecoins like USDT—which are backed by liquid reserves like US Treasury bills—we minimize the risk of de-pegging and ensure that your $1,000 is always $1,000. Compliance is the set of policies, technologies, and procedures that ensure a platform follows financial laws and risk standards. For stablecoin payments, core components include: Regulatory frameworks are maturing fast. The EU’s MiCA regime creates categories and obligations for issuers and service providers; U.S. state guidance like NYDFS stablecoin standards emphasize reserves and redemption; and FATF continues to push Travel Rule adoption for virtual asset transfers. For organizations that need speed and certainty, a partner like WeWire aligns controls to these trends, helping you meet bank, auditor, and regulator expectations while maintaining operational efficiency. References and current framework highlights: Trust is the deciding factor in whether funds clear smoothly or get stuck. Compliance drives that trust. When counterparties—banks, processors, PSPs, and marketplaces—recognize strong controls, they keep channels open and limits flexible. The flip side is costly. Non-compliance can trigger: Industry research shows trust remains fragile in financial services but can be strengthened through transparency, security, and clear governance. Studies such as the Edelman Trust Barometer and central bank reports consistently highlight the link between risk controls and user confidence. For finance and operations teams, the fastest way to move funds is to be the most predictable counterparty. That is the aim of WeWire’s controls—enable trusted financial transactions without adding friction to your workflows. WeWire integrates compliance into each step of the payment flow so you can scale stablecoin payouts and receivables across markets with confidence. Expert perspectives continue to show B2B payment modernization reduces cost-to-serve and error rates while improving working capital. Use this checklist to evaluate whether a stablecoin payment partner meets enterprise-grade compliance and operational needs. WeWire applies risk-based KYC/KYB, ongoing sanctions and PEP screening, and transaction monitoring that blends on-chain and behavioral signals. The platform supports Travel Rule data exchange where required, maintains audit-ready records, and follows clear governance policies aligned to evolving regulations like MiCA, FATF guidance, and relevant state or national rules. Non-compliant stablecoin platforms pose risks such as operational disruption, loss of banking and partners, regulatory exposure, and reputational harm. These issues can lead to frozen transfers, rejected payouts, investigations, fines, lower conversion, and tougher market entry. In short, the cheapest option can become the most expensive if compliance is an afterthought. A compliant stablecoin platform protects your growth. It keeps payments moving, satisfies counterparties, and reduces audit and regulatory risk—without slowing your team. See how WeWire pairs enterprise-grade controls with fast global settlement. Connect with our team to assess your payment flows and design a compliant rollout. Talk to WeWire and start building with confidence.

diadem445c3650ff

What Makes a Stablecoin Platform Compliant?

The Anatomy of a Secure Stablecoin Transaction

1. Regulatory Rigor: The PSP License

2. Institutional-Grade KYC/AML

3. Reserve Transparency

Understanding Stablecoin Compliance

Why Trust Matters in Cross-Border Payments

How WeWire Ensures Secure Transactions

Risk-based onboarding and monitoring

Travel Rule and information sharing

Asset and technology safeguards

Operational benefits for leaders

Comparison of Stablecoin Platforms

Criteria

What to Ask

Why It Matters

WeWire’s Approach

Licensing & Governance

What registrations and policies govern operations? Is there independent compliance oversight?

Demonstrates accountability and regulator alignment.

Operates under applicable registrations with board-approved policies and dedicated compliance leadership.

KYC/KYB & Sanctions

How are customers risk-scored? How often is screening refreshed?

Prevents illicit activity and reduces counterparty risk.

Risk-based onboarding, continuous sanctions/PEP screening, and periodic refresh cycles.

Travel Rule Readiness

Does the platform support originator/beneficiary information exchange?

Required in many corridors; eases bank relationships.

Supports Travel Rule data exchange with compliant partners where applicable.

Stablecoin Policy

Which stablecoins are supported and why? How are issuers vetted?

Transparency on reserves, redemption, and market risk.

Framework to evaluate issuer transparency, reserves, and chain risk before enabling support.

Transaction Monitoring

What rules/models are used? Is on-chain intelligence integrated?

Detects anomalies and enables timely reporting.

Rule- and model-based monitoring leveraging on-chain and behavioral signals.

Security & Controls

How are keys secured? Are permissions and approvals segregated?

Reduces operational and fraud risk.

Hardware-backed key management, role-based access, and multi-approval workflows.

Auditability

Are logs immutable and exportable? Are there third-party assessments?

Simplifies audits and instills trust.

Comprehensive logging and periodic independent assessments.

Settlement & Reconciliation

How fast are payouts? How are FX and fees surfaced?

Impacts cash flow, unit economics, and finance ops.

Real-time settlement windows and transparent fees with reconciliation-ready data.

Data Protection

How is personal and transactional data handled?

Mitigates privacy and compliance risk.

Privacy-by-design with regional compliance (e.g., GDPR) and data minimization.

Support & SLAs

What is the incident response process and uptime commitment?

Keeps operations resilient during spikes or issues.

Structured incident playbooks and enterprise support options.

Frequently Asked Questions

How does WeWire ensure compliance in its operations?

What are the risks of using non-compliant stablecoin platforms?

Conclusion & Next Steps

Stablecoin Compliance & Regulation for Businesses in 2026

April 8, 2026 by diadem445c3650ff For a long time, the world of digital assets felt like the “Wild West.” It was a landscape defined by rapid innovation, high stakes, and a noticeable absence of a sheriff. But as we move through 2026, the dust has settled. The “sheriffs” (global financial regulators) have arrived, and they aren’t here to shut down the party; they are here to build the fences that make the territory safe for institutional expansion. At WeWire, we’ve always believed that for stablecoins to fulfill their promise of revolutionizing global trade, they must move out of the shadows and into the light of clear, robust regulation. But for businesses looking to integrate stablecoins into their treasury or supply chain, the question remains: Are stablecoins actually regulated? And what does the legal landscape look like for my company? Stablecoins are digital tokens designed to track the value of a reference asset—most commonly a fiat currency like USD or EUR. They combine the programmability and settlement speed of blockchains with the familiarity of money-like units. Common types include: Key differentiators from traditional e-money or bank deposits include 24/7 blockchain settlement, composability with smart contracts, and bearer-style transfer between compatible wallets. For businesses, that can compress settlement windows and reduce reliance on correspondent banking systems. Recent 2025 market research on stablecoin adoption points to growing institutional pilots for working capital, supplier payments, and cross-exchange settlement—driven by cost, speed, and interoperability. The short answer is: Yes, increasingly so. Gone are the days when stablecoins were treated as a monolithic “crypto” experiment. Today, regulators distinguish between different types of digital assets. Because stablecoins like USDT or USDC are designed to maintain a stable value relative to a fiat currency (like the US Dollar), they are increasingly governed under frameworks similar to “Electronic Money” or “Stored Value Facilities.” In 2026, the regulatory landscape is defined by three major pillars: Regulators now demand that stablecoin issuers prove they actually have the dollars they claim to hold. New laws in major jurisdictions require monthly, third-party audited reports. This prevents the “run on the bank” scenarios of the past and ensures that 1 USDT is always redeemable for $1. The European Union’s Markets in Crypto-Assets (MiCA) regulation set a global gold standard. It forced issuers to obtain specific licenses to operate within the Eurozone. This moved the needle globally, prompting countries from the UAE to Singapore, and notably across Africa, to develop their own bespoke frameworks. This is where the “legal” meets the “technical.” Every regulated stablecoin transaction must now adhere to Anti-Money Laundering (AML) and Know Your Customer (KYC) standards. This means that for a business to use stablecoins legally, they must partner with a provider that verifies every participant in the transaction chain. Global regulators are converging on a principle: same activity, same risk, same regulation. The implementation details, however, diverge materially. The Markets in Crypto-Assets (MiCA) regulation establishes a bespoke regime for asset-referenced tokens (ARTs) and e-money tokens (EMTs). Issuers face authorization, governance, reserve, and disclosure requirements, with tighter obligations for “significant” tokens. MiCA’s staged application began in 2024 and continues through 2025, with national competent authorities coordinating under the European Banking Authority’s oversight. Post-FSMA 2023 reforms set out a pathway to bring fiat-referenced stablecoins used for payments into the regulatory perimeter. The Bank of England, FCA, and PRA are defining responsibilities for systemic tokens, wallet providers, and service firms. Firms should expect prudential, conduct, and operational resilience standards akin to payments and e-money, with sandbox routes for innovation. The US operates a patchwork. Issuers and intermediaries typically navigate state money-transmitter regimes, New York’s BitLicense for virtual currency businesses, and federal AML/CTF obligations. Federal agencies have issued guidance on reserve quality, supervision expectations, and bank interactions, while Congress continues to debate stablecoin-specific legislation. Many enterprises partner with regulated institutions to mitigate fragmentation risk. Other active jurisdictions include Switzerland (principles-based treatment under FINMA with reserve and AML controls), the UAE (Dubai VARA and Abu Dhabi’s FSRA frameworks), and several Latin American and African markets exploring sandbox models. Across public statements, regulators emphasize “proportionate, risk-based oversight” and “interoperability with existing payments law.” As one recurring line puts it, “same risks should attract the same safeguards,” echoing 2023–2024 publications by multiple authorities. Before deploying stablecoins in live operations, weigh the trade-offs. Key risks: Primary benefits: Case studies show multinationals using fiat-backed stablecoins for supplier payments, exchanges settling balances across venues, and fintechs enabling just-in-time wallet funding for cards and remittances. EU vs. US: two paths to the same destination, with different terrain. For businesses, the takeaways are practical: the EU offers predictability and scale for compliant issuers; the US offers market depth with greater planning overhead; Singapore and Japan offer clarity with strong prudential anchors. Turn policy into process with a few disciplined steps. Industry datasets indicate sharp growth in cross-border stablecoin transactions, particularly for B2B settlement and marketplace payouts. That growth increases scrutiny. To operationalize policies with fewer engineering cycles, Discover compliance tools at WeWire that support screening, controls, and auditability. While many look to the West for regulatory cues, Sub-Saharan Africa has become a hotbed for practical stablecoin policy. In 2024, stablecoins accounted for 43% of total crypto transactions in the region, with $54 billion processed. Governments in Ghana, Nigeria, and South Africa realized early on that they couldn’t simply “ban” a $54 billion industry that was keeping their businesses afloat during currency fluctuations. Instead, they moved toward Regulatory Sandboxes. By allowing companies like WeWire to operate within a controlled environment while developing full-scale frameworks, African regulators have ensured that innovation continues without compromising financial stability. Our PSP license is a direct result of this collaborative evolution—it signals to our clients that WeWire isn’t just a tech platform; it’s a licensed financial institution. It is a common misconception that regulation kills innovation. In the fintech world, the opposite is true. Regulation provides the certainty that CFOs and Boards of Directors need to move from “testing” to “scaling.” Imagine an Accra-based manufacturing firm that sources raw materials from China. Traditionally, a bank wire takes 3–5 business days and incurs heavy intermediary fees. The firm wants to use USDT to settle the invoice in 10 minutes. Regulation is the bridge that allows a local business to use a global tool with total peace of mind. WeWire: Your Partner in Compliance At WeWire, we don’t view compliance as a “box-ticking” exercise. We view it as our primary product. To us, a transaction that isn’t compliant is a transaction that shouldn’t happen. Our integration of Full KYC/AML protocols ensures that every user on our platform is verified. When you open a WeWire Virtual Account, you aren’t just getting a digital wallet; you are getting a regulated financial tool backed by: The EU’s MiCA sets comprehensive authorization, reserve, and disclosure standards. Singapore’s MAS regime is clear and exacting for single-currency payment stablecoins. Japan limits issuance to banks, trust companies, or registered providers. In the US, New York’s BitLicense adds rigor on top of federal AML rules. Start with a jurisdiction-by-jurisdiction analysis of your flows, then align licenses, partners, and assets accordingly. Implement robust AML/CTF and sanctions controls with on-chain monitoring and Travel Rule support. Use regulated custodians, document accounting policies, and maintain incident-response playbooks. Conduct periodic reviews as rules evolve. Consult qualified counsel. The fact that $54 billion moved through stablecoins in Africa last year tells us one thing: The market has already decided that stablecoins are the future of money. People are betting on stablecoins because they solve real problems—inflation, slow borders, and high fees. The arrival of clear regulation is simply the world catching up to that reality. As a business leader, the question is no longer “Should I use stablecoins?” but rather “Who is the most compliant partner to help me use them?” We are proud to be one of the few Ghanaian companies listed in Tether’s directory, and we are even prouder to be a licensed PSP. We’ve built the infrastructure, secured the licenses, and done the legal heavy lifting. The frontier is now open. Are you ready to cross it? If you are still on the fence about the legalities of stablecoins, consider this: The world’s largest financial institutions are now launching their own stablecoins. The technology is proven. The regulators are engaged. The only risk left is the risk of being left behind by competitors who are already settling their global invoices in minutes while you wait for a bank wire to clear.

diadem445c3650ff

What are Stablecoins and How Do They Work?

The Big Question: Are Stablecoins Regulated?

1. Reserve Transparency (The “Show Me the Money” Rule)

2. MiCA and the Global Ripple Effect

3. AML/KYC Compliance

Current Regulatory Landscape for Stablecoins

European Union (EU):

United Kingdom (UK):

United States (US):

Asia-Pacific highlights:

Risks and Benefits of Using Stablecoins in Business

Comparative Analysis of Global Regulatory Frameworks

EU (MiCA): strengths and constraints

US (patchwork + proposals): flexibility with complexity

Asia standouts

Compliance Strategies for Businesses

1) Map your use cases and exposure

2) Choose compliant assets and partners

3) Build AML/CTF, sanctions, and Travel Rule capability

4) Licensing, reporting, and consumer protections

5) Accounting, tax, and treasury controls

Regulatory Compliance Checklist for Businesses

The African Context: Leading from the Front

Why Regulation is Actually Good for Your Business

Real-World Use Case: The Global Manufacturer

Frequently Asked Questions

What countries have the strictest stablecoin regulations?

How can businesses ensure compliance with stablecoin regulations?

The Future: Betting on Stability

Are Stablecoins Safe for Business? Addressing Security Concerns Head-On

March 23, 2026 by diadem445c3650ff The phrase “time is money” has taken on a literal, digital meaning. For businesses operating across borders, whether you are a Ghanaian tech hub paying developers in Europe or a Canadian firm sourcing materials from Southeast Asia, the traditional banking system feels increasingly like a relic of the 1970s. In recent years, there has been a shift. Once a niche tool for crypto traders, stablecoins have matured into the primary “rails” for modern global commerce. They offer faster settlement, 24/7 availability, and lower fees for cross-border payments, payroll, and vendor payouts. But as adoption skyrockets, so does the skepticism. Business owners, CFOs, and compliance officers are all asking the same critical questions: Are stablecoins safe? What are the actual stablecoin risks? And can I trust my company’s payroll and liquidity to a digital asset? Stablecoin security is now a board-level topic. You need strong encryption, tight keys and access, regulatory alignment, and continuous monitoring. Anything less invites operational, financial, and reputational risk. At WeWire, we believe that transparency is the bedrock of trust. Today, we’re taking the “marketing” hat off and putting the “security” hat on to address these concerns head-on. To answer if stablecoins are safe, we first have to define what “safety” means in a corporate context. For a business, safety means three things: Value Stability, Regulatory Compliance, and Technical Security. The biggest fear for any business is waking up to find that the 100,000 “dollars” they held in stablecoins is suddenly worth 80,000. This is known as “de-pegging.” In the past, algorithmic stablecoins (which rely on code and “voodoo” math to stay at $1) proved to be high-risk. However, the industry has shifted. Today, the “Gold Standard” for business safety is fiat-backed stablecoins like USDT (Tether) and USDC. These are backed by actual cash and cash equivalents held in regulated financial institutions. The WeWire Perspective: We prioritize assets that have stood the test of time and market volatility. By integrating with established directories like the Tether USDT Ecosystem, we ensure our users are interacting with the most liquid and battle-tested assets in the world. Is it legal? Will the government seize the funds? In 2026, the regulatory landscape is much clearer than it was five years ago. Major markets—including Canada, the EU, and several African nations—have established frameworks for digital assets. Stablecoin security isn’t just about encryption; it’s about the “license” behind the platform. A stablecoin is only as safe as the gateway you use to access it. Stablecoins are digital tokens designed to track a reference asset—usually a fiat currency like USD. Common models include fiat-backed custodial coins, crypto-backed overcollateralized coins, and algorithmic designs. For businesses, the leading use cases are cross-border payments, marketplace payouts, treasury diversification, and on/off-ramps for digital commerce. Security spans much more than blockchain math. You must evaluate the issuer’s reserve quality, redemption rights, smart contract integrity, wallet and key protections, chain selection, and compliance obligations. Each layer can be hardened—or become a failure point. Regulation is tightening. Research on regulatory impacts in fintech consistently shows that clear standards around reserves, disclosures, and consumer protections improve market resilience. Expect more rigorous attestations, audits, and operational requirements on issuers and intermediaries. If you’re building a stablecoin program, lean on WeWire’s expertise to align technical controls with policy, governance, and payments operations from day one. While stablecoins offer revolutionary speed, we wouldn’t be a responsible partner if we didn’t highlight the risks. Knowledge is the best defense. This is the risk that the issuer of the stablecoin doesn’t actually have the money they claim to have. Since stablecoins live on the blockchain, they rely on code (smart contracts). If the code has a bug, a hacker could theoretically exploit it. Ironically, the biggest risk to stablecoin security isn’t the blockchain—it’s the human using it. Weak passwords, lost private keys, or falling for a phishing link can lead to total loss. Security is a program, not a point solution. Build on tested rails and enforce controls across people, process, and technology. Adoption is scaling quickly as controls mature—see the 2025 stablecoin adoption stats to benchmark your roadmap and risk posture against peers. The biggest concerns are peg and issuer risk, regulatory change, and technical vulnerabilities. You should scrutinize reserve quality, redemption rights, and banking partners; monitor rule changes; and harden smart contracts, wallets, bridges, and oracles. Operationally, access control lapses, poor reconciliations, and weak vendor oversight create avoidable exposure. Start with reputable, audited issuers and diversify across assets and chains. Use MPC/HSM custody, multi-approver workflows, allowlists, and transaction limits. Adopt audited contracts and real-time monitoring. Bake in KYC/KYB, sanctions screening, and Travel Rule compliance. Reconcile daily, test incident playbooks, and hold vendors to SOC 2/ISO 27001-backed SLAs. Stablecoins can streamline payments and treasury, but only with disciplined security. Choose robust issuers, enforce enterprise-grade custody, codify transaction policies, and align compliance from day one. Test often. Monitor continuously. If you’re evaluating or scaling a program, partner with experts who blend payments operations with crypto-native controls. Align your roadmap with security, compliance, and finance outcomes, and turn stablecoin efficiency into durable advantage.

diadem445c3650ff

The Core Question: Are Stablecoins Safe?

1. Value Stability (The De-pegging Risk)

2. Regulatory Compliance

Understanding Stablecoin Security

Real-World Stablecoin Risks: What Businesses Must Know

A. Counterparty Risk

B. Smart Contract Vulnerabilities

C. The “Human Factor” (Phishing and Key Management)

Best Practices for Businesses Using Stablecoins

Choose the right instruments and rails

Harden wallets and keys

Secure smart contracts and integrations

Compliance-by-design

Operational resilience

Security Checklist for Implementing Stablecoins

Governance and policy

Issuer and asset selection

Wallets and custody

Smart contracts and integrations

Compliance and monitoring

Operations and vendor risk

Frequently Asked Questions

What are the main security concerns with stablecoins?

How can businesses mitigate risks when using stablecoins?

Conclusion & Next Steps