Virtual Accounts in Supply Chain Finance: Improving Visibility from Supplier Payment to Goods Delivery

December 15, 2025 by diadem445c3650ff Supply chains run on trust, timing, and transparency. Yet for many manufacturers and distributors, one of the most critical links in the chain—payments—remains surprisingly opaque. Money moves, but visibility lags behind. Finance teams release funds, operations teams wait for confirmation, suppliers hesitate to ship, and logistics timelines slip. In a world where supply chain efficiency can make or break margins, this disconnect is no longer sustainable. Virtual accounts are emerging as a powerful tool in supply chain finance, helping businesses link supplier payments directly to shipments, instalments, and delivery triggers—bringing financial clarity to physical goods movement. According to research from McKinsey, companies with strong end-to-end supply chain visibility can reduce inventory costs by up to 30 percent while improving service levels by more than 20 percent. Yet visibility is often discussed in terms of logistics, inventory tracking, and forecasting—rarely in terms of how payments move. For many global supply chain players, payments still flow from a small number of corporate bank accounts. Funds are sent in batches, references are inconsistent, and reconciliation happens after the fact. When suppliers cannot immediately identify what a payment is for—or whether a payment has been made at all—shipments slow down and disputes arise. The cost is not just administrative. Delayed payments can stall production, strain supplier relationships, and ultimately impact delivery timelines downstream. Virtual accounts change this dynamic by adding structure to how payments are made and tracked. Rather than relying on one shared bank account, businesses can issue unique virtual accounts under a single master account. Each virtual account serves as a dedicated identifier—tied to a supplier, a shipment, a purchase order, or even a specific stage of delivery. In supply chain finance, this means payments are no longer abstract transfers. They become clearly attributable events that align directly with operational milestones. For example, a manufacturer sourcing components from multiple suppliers can assign a dedicated virtual account to each supplier. When funds arrive in that account, both the buyer and the supplier know exactly what the payment represents. There is no ambiguity, no waiting for reconciliation, and no back-and-forth emails to confirm receipt. Imagine a distributor operating across several regions, importing goods from overseas manufacturers. Payment terms require an upfront deposit, a mid-production instalment, and a final payment upon delivery. In a traditional setup, tracking these payments across multiple bank accounts is time-consuming and error-prone. Operations teams may delay shipment releases until finance confirms payment status, often relying on screenshots or manual confirmations. With virtual accounts, the distributor assigns a unique account to each shipment. All instalment payments flow into that account. The moment a payment lands, the system reflects it in real time. Operations teams can immediately see which milestone has been met and trigger the next step—whether that is releasing goods from the factory or approving customs clearance. Payments become part of the supply chain workflow, not a separate finance process running in parallel. Supplier relationships depend heavily on predictability. According to the World Economic Forum, uncertainty around payment timing is one of the top reasons suppliers deprioritize orders, particularly in emerging markets. Virtual accounts help restore confidence by giving suppliers a clear and dedicated payment endpoint. When suppliers know that funds are allocated specifically to them—or even to a specific shipment—they are more willing to prioritize production and release goods quickly. This transparency reduces disputes, accelerates delivery timelines, and strengthens long-term partnerships. In competitive supply chains, that trust can be the difference between meeting demand and falling behind. Distributors often operate at the intersection of multiple buyers and suppliers, managing complex flows of incoming and outgoing funds. Without structured payment systems, visibility quickly breaks down. Virtual accounts allow distributors to segment payments by buyer, region, or channel, while still maintaining centralized liquidity control. Incoming funds from customers can be matched directly to outgoing payments to suppliers, improving cash flow management and reducing reconciliation delays. For cross-border distributors, this becomes even more valuable. When payments move across currencies and jurisdictions, clarity and speed are essential to maintaining operational momentum. Beyond operational efficiency, virtual accounts generate rich financial data that can be analyzed alongside logistics and inventory metrics. Over time, businesses gain insight into how long it takes for payments to translate into deliveries, which suppliers respond fastest to payment milestones, and how much cash is tied up in goods in transit. Deloitte reports that organizations with real-time financial visibility are twice as likely to make faster and more confident operational decisions. Virtual accounts contribute directly to this visibility by transforming payments into structured, trackable data points. This data enables better forecasting, more accurate working capital planning, and more informed negotiations with suppliers. WeWire provides the infrastructure that supply chain players need to implement virtual accounts at scale. Manufacturers, distributors, and platforms can issue virtual accounts to suppliers or sub-suppliers, create sub-customer structures, and operate across major currencies such as GBP, USD, and EUR. By integrating virtual accounts into existing finance and operations workflows, WeWire helps businesses link payments directly to supply chain events—without overhauling their entire treasury stack. The result is improved visibility, faster settlement, and more resilient supplier relationships. As supply chains grow more global and interconnected, unstructured payments become a bottleneck. Virtual accounts offer a way forward—bringing order, transparency, and intelligence to how money moves alongside goods. The most successful supply chain organizations will be those that treat payments not as a back-office afterthought, but as a core operational lever. From supplier payment to goods delivery, visibility matters. WeWire helps make that visibility possible.

diadem445c3650ff

The Hidden Cost of Poor Payment Visibility

Virtual Accounts: Linking Money to Movement

A Realistic Scenario: Payments as Delivery Triggers

Building Supplier Trust Through Transparency

Managing Complexity Across Distributors and Regions

Turning Payment Data into Supply Chain Insight

How WeWire Supports Supply Chain Finance

The Future of Supply Chain Finance

The Modern Treasury Dashboard: Combining Virtual Accounts, Bank Accounts & Stablecoin Flows for Global Corporates

December 10, 2025 by diadem445c3650ff Global treasury teams are operating in an era of unprecedented complexity. A single multinational enterprise might manage dozens of bank accounts across regions, hundreds of virtual accounts tied to customers or subsidiaries, and—more recently—digital asset flows such as stablecoins used for cross-border settlements. Each system speaks a different language. Each reports on a different timeline. And none, by default, offers a unified picture. This results in fragmented visibility, slower decision-making, and trapped liquidity. Forward-thinking enterprises are solving this problem by building modern treasury dashboards—centralized views that combine virtual accounts, traditional bank accounts, and stablecoin rails into a single source of truth. This is a reporting upgrade and a strategic shift in how global businesses manage money. According to PwC, over 60% of CFOs cite lack of real-time cash visibility as a major operational risk. In a global environment shaped by FX volatility, rising interest rates, and supply-chain disruptions, delayed or incomplete treasury data directly impacts profitability. Traditional treasury models were built for a slower world—one where cash moved predictably, reconciliations happened overnight, and banking systems were region-locked. Today’s enterprises operate across borders, currencies, and payment rails in real time. To compete, treasury leaders need answers to questions like: A unified treasury dashboard makes these answers instantly accessible. Virtual accounts have become a cornerstone of modern treasury architecture. Unlike traditional bank accounts, virtual accounts allow enterprises to create dedicated account identifiers for customers, subsidiaries, business units, or use cases—without opening separate physical bank accounts. For example: The advantage is precision. Every inflow is automatically attributed, eliminating manual reconciliation and enabling real-time balance tracking. With WeWire, enterprises can issue virtual accounts in major currencies such as GBP, USD, and EUR, and extend those accounts to sub-customers seamlessly. These virtual account balances become the first layer of insight in a treasury dashboard—showing exactly where funds originate and how they are segmented. Despite the rise of fintech infrastructure, traditional bank accounts remain essential. They serve as: However, bank data is often siloed. Enterprises may hold accounts across multiple banks, each with different reporting formats, cut-off times, and APIs. Modern treasury dashboards integrate bank account data directly—pulling balances, transaction histories, and FX positions into the same interface as virtual accounts. This creates continuity between legacy banking infrastructure and new financial rails. By integrating WeWire’s virtual accounts with existing bank accounts, treasury teams can: Stablecoins are no longer experimental. According to Chainalysis, stablecoin transaction volume surpassed $7 trillion globally in 2023, driven largely by corporate and institutional use cases such as cross-border settlement and treasury optimization. For global corporates, stablecoins offer: When integrated responsibly, stablecoin rails become a powerful complement—not a replacement—to traditional banking. In a treasury dashboard, stablecoin balances and flows provide visibility into: The most advanced enterprises treat stablecoins as another treasury instrument, alongside bank balances and virtual accounts. Imagine a global manufacturing company operating across Africa, Europe, and North America. Previously, the treasury team relied on: Decision-making lagged by days. By building a unified treasury dashboard, the company now sees: This consolidated view enables: WeWire sits at the intersection of global payments, virtual accounts, and enterprise-grade financial infrastructure. With WeWire, global corporates can: Rather than forcing enterprises to overhaul their entire treasury stack, WeWire acts as a connective layer—bringing structure, attribution, and clarity to global cash movement. The role of treasury is evolving. It is no longer a back-office function focused solely on reconciliation and compliance. It is becoming a strategic command center—guiding decisions on liquidity, risk, and growth. Enterprises that succeed in this new era will be those that: A modern treasury dashboard is not just about visibility. It is about control, speed, and confidence. And with the right infrastructure—combining virtual accounts, bank accounts, and digital asset flows—global corporates can finally see their financial operations as one connected system. WeWire helps enterprises build that system.

diadem445c3650ff

Why Treasury Visibility Has Become a Strategic Priority

The Three Pillars of a Modern Treasury Dashboard

1. Virtual Accounts: Granular Control and Attribution

2. Traditional Bank Accounts: The Institutional Backbone

3. Stablecoin Flows: Speed and Global Liquidity

Bringing It All Together: A Single Source of Truth

How WeWire Enables Modern Treasury Architecture

The Future of Treasury Is Unified

Bank Transfers vs Stablecoins: What’s the Cheapest Way to Pay Your Suppliers?

December 8, 2025 by diadem445c3650ff For businesses that source goods from China and other parts of Asia — especially those operating from Africa and other emerging markets — paying suppliers efficiently can make or break your margins. Every percentage point lost on fees, poor FX rates, or slow settlement times compounds into higher landed costs and reduced competitiveness. Two methods dominate cross-border trade today: traditional bank transfers (SWIFT) and stablecoin-based payments. For decades, traditional bank transfers (via SWIFT, ACH, or wire) were the only viable option. Today, digital assets, particularly stablecoins, present a powerful, cost-effective challenger. Both have advantages, costs, and risks, but only one consistently delivers the speed, affordability, and predictability that modern global trade demands. In this guide, we compare bank transfers vs stablecoins, break down their true costs, and explore why platforms like WeWire are redefining the economics of paying suppliers overseas. For decades, the default way to pay suppliers has been through international wire transfers via the SWIFT network. While familiar, this system was never designed for emerging-market businesses, and its shortcomings are felt most by importers paying suppliers in China or Asia. The multi-day settlement time of traditional banking is a major liquidity constraint. In fast-moving industries like ecommerce, manufacturing, and wholesale trade, slow money movement means lost opportunity. Traditional international wire transfers rely on the SWIFT network, a chain of correspondent banks. Every bank in the chain takes a cut, leading to cumulative fees that are difficult to predict. Many African businesses struggle to secure foreign-currency liquidity due to: This adds friction and cost before you even initiate the payment. Payments may be delayed or blocked due to: The result is a system that is expensive, slow, and unpredictable Once a SWIFT transfer is initiated, tracking its exact location or arrival time can be nearly impossible, leading to frustrating inquiries and reconciliation delays for both you and your supplier. Bank transfers are the entrenched method for global B2B payments, but their comfort comes at a hidden price—a price paid in fees, time, and transparency. Stablecoins such as USDT or USDC have exploded in popularity in B2B global trade because they solve many of the issues bank transfers cannot. A stablecoin is a digital currency pegged to a stable asset like the US dollar, meaning its value stays consistent. When used for cross-border payments, they offer: Payments clear in seconds or minutes, not days. Stablecoin transfers typically cost less than $1 on certain chains. Businesses can convert from local currency to USD stablecoins at competitive rates — especially when using a platform that blends traditional and alternative rails, like WeWire. Chinese and Asian suppliers increasingly accept stablecoins because they: In industries like electronics, textiles, manufacturing, and ecommerce sourcing, this has become a competitive advantage. Below is a simplified comparison assuming a $10,000 payment to a supplier in China: It’s not even close. Stablecoins offer up to 97% cost savings and drastically faster timelines. A 2024 analysis by a global payments firm noted that businesses using stablecoins for cross-border B2B payments saw average transaction costs drop by over 80% compared to traditional wire transfers for amounts exceeding $1,000. While stablecoins solve speed and cost, many businesses struggle with: This is where WeWire becomes a game-changer. WeWire provides a unified global banking infrastructure specifically built for businesses in emerging markets. Rather than forcing a choice between bank transfers or stablecoins, WeWire blends both into a single, flexible payment system. 1. Virtual Accounts in USD, EUR, GBP, NGN, GHS and more Easily collect, store, and pay suppliers in the currencies they prefer — including China’s most common settlement currencies. 2. Stablecoin Payment Rails for Instant Supplier Settlement Fund your account via: Then send stablecoins directly to suppliers within minutes. This eliminates the SWIFT delays importers hate. 3. Better FX Rates Because WeWire uses both traditional banking rails and deep liquidity stablecoin rails, you access more competitive FX than traditional banks offer. 4. Compliance Built for Emerging Markets Unlike many payment providers, WeWire is licensed in: This ensures payments are fast and compliant — not risky shortcuts. 5. One Dashboard to Manage All Supplier Payments Send USD, stablecoins, or any supported currency from a single platform designed for importers. Many of the fastest-growing importers today use a hybrid strategy: WeWire makes this effortless. Paying suppliers in China and Asia shouldn’t be slow, expensive, or unpredictable. Stablecoins offer: And when paired with a modern infrastructure platform like WeWire, you get the speed of stablecoins, the trust of regulated banking, and the cost-efficiency needed to scale your business. If you want to reduce your payment costs, improve your supplier relationships, and accelerate your entire supply chain, stablecoin-enabled payments through WeWire are the smartest move you can make.

diadem445c3650ff

The Problem With Traditional Bank Transfers

1. Slow Settlement Times

2. High Transaction Fees and Intermediary Charges:

3. Limited Access to USD, EUR, or CNY

4. Compliance Red Tape

5. Lack of Transparency:

Why Stablecoins Are Emerging as an Alternative

1. Near-Instant Settlement

Suppliers receive funds almost immediately, meaning they can start production or ship goods sooner.2. Lower Transaction Costs

And because they bypass correspondent banks, there are no intermediary fees eating into your payment.3. Better FX Efficiency

4. Suppliers Are Already Using Them

Cost Comparison: Bank Transfers vs Stablecoins

Cost Component

Bank Transfer (SWIFT)

Stablecoin Payment

Transfer Fee

$20–$70

$0.10–$1

Intermediary Fees

$20–$60

$0

Supplier Bank Fee

$15–$30

$0

FX Spread

3–8%

0.2–1% (via fintechs)

Settlement Time

3–7 days

seconds–minutes

Typical Total Cost:

But Stablecoins Alone Are Not Enough — You Need Infrastructure

How WeWire Makes Stablecoin + Banking Rails Work Seamlessly

With WeWire, you get:

Which Method Should You Choose? Bank Transfer or Stablecoins?

Choose Bank Transfers When:

Choose Stablecoins When:

Best Approach: Use Both With WeWire

Conclusion: Stablecoins Are The Cheapest Way to Pay Suppliers — and WeWire Makes It Frictionless

Traditional bank transfers carry high fees, long settlement times, and tight compliance restrictions — especially painful for businesses in emerging markets.

CBDCs vs Stablecoins: Convergence or Competition?

November 24, 2025 by diadem445c3650ff When Akua, the finance head of a Ghanaian export firm, receives USD payments from a U.S. buyer today, she does a mental triple check: convert to stablecoin, route through a trusted wallet, then off-ramp to cedi or USD. She worries about exchange spreads, counterparty risk, and regulatory uncertainty. But two years from now, the sequence might look quite different: a Ghanaian e-Cedi (a CBDC) flows seamlessly into a USD stablecoin rail for cross-border trade, then settles in her firm’s accounts. That future is not fantasy — it’s actively under design. The question is: will stablecoins and CBDCs fight to dominate, or evolve into interoperable layers of a modern monetary stack? Central Bank Digital Currencies (CBDCs) and stablecoins are two distinct forces vying to shape the future of money, particularly in the fast-evolving financial landscapes of Africa and other emerging markets. The relationship between them is complex, marked by intense competition for dominance in payment rails, but also demanding a degree of convergence and interoperability for the global system to function efficiently. This dynamic tension—public trust versus private innovation—defines the digital money dichotomy. For a payment solutions provider like WeWire, understanding this terrain is crucial; our goal is not to choose a side, but to build the bridges that connect them both, ensuring our clients benefit from the speed of stablecoins and the trust of central bank money. Both CBDCs and stablecoins are digital liabilities designed to offer the speed and efficiency of modern blockchain technology. However, their fundamental differences place them in direct competition for the user base and control over the payment infrastructure. Stablecoins have achieved rapid adoption because they solve immediate, real-world problems for businesses: Central banks, driven by the desire to maintain monetary control in the digital age and counter the rise of private digital currencies, are accelerating their CBDC research. The competition is real, but it is unlikely to result in a “winner-take-all” scenario. For a truly efficient global payment system, managed coexistence is the most likely outcome, forcing convergence between the two systems. The most promising area for convergence is at the wholesale level: Central banks lack the customer-facing technology, marketing expertise, and existing user base of private fintechs. They will need partners to drive adoption: Particularly in Africa, central banks must balance inclusion, sovereignty, and system credibility. Many central banks prefer to move slowly and maintain control. But stablecoins still face issues around trust, regulation, reserve transparency, and final settlement risk. For WeWire, the future is about connectivity. We recognize that businesses in emerging markets will need both the dollar-pegged stability of private stablecoins for global trade and the sovereign trust of local CBDCs for domestic transactions and regulatory compliance. WeWire is building the compliant, technical infrastructure to act as the trusted hub between these two financial worlds: The future of digital payments is not CBDCs or stablecoins; it is CBDCs and stablecoins, connected by compliant infrastructure. WeWire is building that compliant bridge, ensuring our clients stay ahead in the rapidly evolving digital economy. We manage the complexity of competition and convergence so you can focus on global growth.

diadem445c3650ff

The Digital Money Dichotomy: Competition is the Default

Feature

Stablecoins (Private Money)

CBDCs (Central Bank Money)

Issuer

Private companies (e.g., Circle, Tether), often regulated.

National Central Banks (a sovereign guarantee).

Primary Goal

Usability, rapid adoption, cross-border efficiency.

Monetary oversight, financial stability, and policy alignment.

Backing

Fiat reserves, short-term securities, or a basket of assets.

Full sovereign guarantee (direct liability of the central bank).

Current Status

$145B+ USD-pegged market cap, dominating crypto payments.

114+ countries exploring; only 4 fully launched (e.g., eNaira).

Where Stablecoins Win: Speed and Global Reach

Where CBDCs Win: Trust and Sovereignty

The Inevitable Future: Convergence and Interoperability

1. Wholesale CBDC as the Risk-Free Anchor

2. Private Sector as the Distribution Agent

CBDC & Stablecoin in Emerging Markets: Risks, Opportunities, and Timing

Risks for CBDCs

Opportunities for Stablecoins

What wins depends largely on design decisions:

WeWire’s Strategic Position: Building the Interoperability Bridge

Virtual Accounts and On-Demand Banking Services in Africa’s Export Hub

November 11, 2025 by diadem445c3650ff For decades, the story of African exports was dominated by commodities, long shipping times, and the agonizing wait for payment to clear through a maze of correspondent banks. It was a story of friction, high cost, and lost opportunities. But today, a quiet revolution is happening in major commercial centers—from the manufacturing zones of South Africa and Morocco to the burgeoning tech and services hubs of Nigeria and Kenya. The new engine of growth isn’t just the sheer volume of goods leaving the continent; it’s the speed and efficiency with which the resulting revenue is collected, verified, and re-deployed. At the heart of this operational shift is the adoption of Virtual Accounts and On-Demand Banking Services. This is not a general global expansion piece. This is a story about African exporters finally commanding control of their cash flow, tackling regulatory nuance, and unlocking exponential growth potential using modern financial technology. And among the companies leading this transformation is WeWire, building the bridge between Africa’s exporters and the global financial system. Africa’s export story is changing. The continent’s total exports crossed $490 billion in 2024, driven by new sectors—agriculture, digital services, renewable energy, and value-added manufacturing. The African Continental Free Trade Area (AfCFTA) aims to create a single market of 1.3 billion people, promising a 52% increase in intra-African trade by 2035 (World Bank). But beneath this optimism lies an operational bottleneck: traditional banking infrastructure. In short, Africa’s real economy is globalizing faster than its banking rails can adapt. A virtual account is not just a digital wallet, it’s a smart, programmable sub-account that mirrors the functions of a traditional bank account but operates instantly and globally. Imagine you’re a coffee exporter in Kenya supplying buyers in Germany, the UAE, and the U.S. Instead of juggling three separate foreign bank accounts, you generate three virtual (IBAN) accounts—one per buyer or market. Each IBAN routes payments directly into your main account, automatically tagged to the buyer, currency, and invoice number. No follow-ups. No manual reconciliation. No waiting for a bank officer to confirm receipt. Key benefits for exporters: According to a 2024 African Fintech Network survey, exporters using fintech-based virtual accounts report 35–50% faster settlement times and up to 40% lower FX costs. Meet Aisha, the CEO of a textile manufacturer in Lagos, Nigeria, exporting high-end fashion to retailers in London and New York. Before adopting virtual accounts, Aisha’s team used three different banks—one for naira, one for dollars, and one for euros. Each payment must travel through 2-3 correspondent banks, incurring up to 5% in fees and exchange rate markups. The local bank processes the payment, which, due to manual reconciliation and regulatory checks, takes 5 to 7 business days to clear and notify Aisha. Crucially, Aisha has no way to easily match the incoming USD to the specific invoice, relying on vague wire references and email communication. Reconciliation was done manually, often days after goods had already shipped. This 7-day payment lag meant she couldn’t immediately purchase raw materials for her next order, creating an operational choke point. When Aisha switched to Virtual Accounts with WeWire, the difference was immediate: This transition from a 7-day blind spot to an instant, reconciled transaction is the core advantage driving adoption across Africa’s major export hubs. African financial landscapes are characterized by robust, yet often complex, regulatory frameworks, especially concerning the repatriation of export proceeds and foreign currency controls. For exporters, compliance isn’t a suggestion; it’s the gateway to growth. In key economies like Nigeria and Egypt, central banks require meticulous reporting on all foreign exchange transactions. This is where the structural integrity of Virtual Accounts provides a crucial compliance shield: The shift to digital data integrity offered by virtual accounts is often better-suited to meet modern regulatory demands than outdated physical banking processes. Governments that embrace this technology will see increased trade flow transparency. WeWire’s model aligns closely with this evolution. By obtaining licenses in multiple jurisdictions—including a Global Treasury Activities License in Mauritius—WeWire offers a compliant infrastructure that meets both international and local standards. This positions it as a trusted partner for exporters who must satisfy regulators, buyers, and auditors simultaneously. The use of on-demand banking services isn’t just saving time; it’s enabling fundamental shifts in business models across key sectors: As African companies increasingly export digital services (software, BPO, creative services), they need to be paid like any global firm. Virtual Accounts allow these businesses to collect payment as if they had a local bank account in the US or EU, removing the barrier of having to ask international clients to send costly, slow wires. The African digital economy is projected to reach $180 billion by 2025. Virtual Accounts are the treasury rail for a significant portion of this growth. For processors exporting high-quality cocoa, refined minerals, or manufactured goods, cash flow is seasonal and tight. VAM allows them to: The future of African exports is digital-first. By 2030, Africa’s digital economy is expected to exceed $712 billion, with trade digitization playing a central role (Google & IFC report). Virtual accounts and on-demand banking services will be the invisible rails behind that growth. Why? Because they solve the three problems that have long constrained African exporters: As logistics, trade finance, and digital payments converge, virtual accounts will underpin a new kind of trade infrastructure—one that’s faster, inclusive, and built for scale. At the heart of this transformation is WeWire, a platform purpose-built for emerging markets. Here’s why exporters and financial institutions choose WeWire: Whether you’re a cocoa exporter in Ghana, a logistics firm in Kenya, or a financial institution serving SME clients, WeWire gives you the control and speed global trade demands. Africa’s exporters are no longer limited by geography—they’re limited by the speed of money. Virtual accounts and on-demand banking are eliminating that barrier. And as this shift accelerates, one thing is clear: the exporters who digitize their treasury early will lead Africa’s next trade wave. With WeWire, that future isn’t theoretical—it’s live in 48 hours.

diadem445c3650ff

The Export Boom That Banking Can’t Keep Up With

Virtual Accounts: The Financial Shortcut for Exporters

The Exporter’s Cash Flow Problem: A Case of Two African Realities

Navigating Regulatory Nuance: The Compliance Advantage

Central Bank Reporting and Know-Your-Customer (KYC)

The Growth Potential: Fueling the Next Generation of African Exports

1. High-Value Services Exports (South Africa, Kenya)

2. Agro-Processing & Manufacturing (Morocco, Ghana)

The Growth Potential: Virtual Accounts as Africa’s Next Trade Enabler

WeWire: The Partner Powering Africa’s Export Revolution

How SEGEA, a Global Food Distributor, Accelerated Payments with WeWire’s Stablecoin Rails

November 10, 2025 by diadem445c3650ff Food is essential to our survival, but the food business doesn’t begin in the kitchen. From sourcing farm produce to manufacturing, packaging, and distribution, every step in this ecosystem is powered by payments. One company at the center of keeping this system running in Cyprus is SEGEA. Founded in 2010 by Geoffrey Serrurier, SEGEA is a global supplier of animal protein, sourcing products from over 20 countries. The company connects food producers, slaughterhouses, and distributors to ensure high-quality meat exports to clients around the world. For SEGEA, reliability and speed in supplier payments are crucial to maintaining smooth global operations. In this case study, we’ll explore how WeWire connected SEGEA to our global payment infrastructure, enabling faster cross-border payments and giving the company more freedom to grow. For years, SEGEA struggled with international payment bottlenecks that slowed down supplier relationships and created unnecessary friction in daily operations. “Before WeWire, paying my suppliers could take weeks. Proof of payment could take up to four weeks to arrive, and transfer fees were very high,” Geoffrey recalls. “We needed a partner we could truly trust. One who understood the pace of international trade.” While traditional payment systems promised better rates, they came with long processing times, high fees, and unpredictable liquidity, often leaving suppliers waiting and slowing down exports. These delays made doing business difficult. In search of a faster, more reliable solution, SEGEA turned to WeWire. “From the very first email, I got a quick response and a dedicated person who walked me through everything. That gave me confidence,” says Geoffrey. “The first transaction was smooth, and that’s when I knew WeWire was different.” By leveraging WeWire’s stablecoin payment rails (USDT & USDC) and OTC desk, SEGEA could pay suppliers instantly, bypassing traditional banking delays and exchange rate complications. The business also no longer had to worry about the availability of FX liquidity as WeWire’s liquidity runs deep across fiat currencies and stablecoins. The result was a more efficient, transparent, and liquid process for international trade. Within weeks of adopting WeWire, SEGEA experienced transformative operational benefits: “WeWire makes supplier payments effortless. I can send funds instantly, regardless of whether my suppliers are located in Africa or around the world. It’s the bridge that connects my business to the world,” Geoffrey says. “It’s efficient, reliable, and gives me back control over my operations.” For SEGEA, WeWire is a strategic partner that enabled the company to operate globally with confidence. By removing the pain points of cross-border banking, WeWire empowers manufacturers and exporters like SEGEA to focus on what matters most: delivering quality products on time, without worrying about payment delays or liquidity gaps. “With WeWire, we’ve gained time, trust, and transparency,” Geoffrey concludes. “It’s the kind of partner any global business needs.

diadem445c3650ff

The Challenge: Costly Delays and Broken Trust in Cross-Border Payments

The Solution: Instant Payments Through WeWire Stablecoin and OTC Rails

The Results: Speed, Efficiency, and Liquidity

Building Global Trust Through Simplicity and Speed

Treasury Management with Stablecoins: Best Practices for Businesses

November 10, 2025 by diadem445c3650ff Two years ago, “stablecoins” sounded niche. Today they’re mainstream treasury tools. As of mid–2025, the global stablecoin market surpassed $250B and keeps expanding as regulators publish clear rulebooks and enterprises seek faster, cheaper settlement across borders. Stablecoins are no longer just a niche crypto asset, dollar-pegged stablecoins like USDC and USDT are rapidly evolving into a critical tool for modern corporate treasury. For finance leaders tasked with managing global cash flows, mitigating risk, and enhancing working capital efficiency, stablecoins offer a powerful new infrastructure. This guide explores the practical strategies companies can adopt to hold, hedge, and utilize stablecoins as part of their treasury operations, addressing the core challenges of risk control, diversification, cash flows, and accounting. Traditional treasury management, especially in cross-border scenarios, is plagued by friction. Payments can take days, correspondent banking fees are high, and lack of visibility ties up capital in “float.” Stablecoins, which are digital dollars operating on blockchain rails, fundamentally solve these issues. Stablecoins facilitate near instantaneous settlement, 24/7/365, bypassing the restrictive hours and intermediary chains of the traditional system. Stablecoins aren’t a replacement for cash, they’re a complementary rail. Treasurers use them where speed, cost, or market hours matter most, then sweep back to bank money as policy dictates. Integrating stablecoins requires a robust framework to manage new digital asset-specific risks. Not all stablecoins are created equal. The collapse of algorithmic stablecoins like TerraUSD highlights the need for careful selection. The digital nature of stablecoins introduces new security concerns. Stablecoins aren’t just for payments; they are a powerful cash and cash-equivalent reserve for strategic treasury. For companies with significant US Dollar exposure and global operations, holding a portion of corporate reserves in dollar-pegged stablecoins offers unparalleled flexibility. In emerging markets, where local currencies can be extremely volatile, stablecoins act as a critical hedge against hyperinflation and devaluation. The main hurdle for corporate stablecoin adoption remains the lack of clear, consistent global accounting standards. The primary challenge is how to classify stablecoins on the balance sheet: as Cash Equivalent, a Financial Instrument, or an Intangible Asset. Regulatory clarity is increasing, exemplified by new legislation like the GENIUS Act in some jurisdictions. Businesses must proactively track compliance. A distributor in Lagos needs to settle a EUR-invoice over a weekend. They pay in USD stablecoin on Saturday; WeWire converts to EUR and credits the supplier’s Virtual EUR account Monday morning—no multi-day wire lag, no cut-off frustration. In corridors where bank fees pile up, savings are material (recall SSA’s high transfer costs). A marketplace pays hundreds of creators globally. Stablecoin rails enable T+0 batch payouts; creators who prefer banks off-ramp to Virtual USD/GBP/EUR accounts the next business day. Treasury keeps only a small on-chain float, sweeping the rest nightly per policy. A South African importer invoices in USD but reports in ZAR. To cut USD funding costs and weekend risk, they use stablecoins for just-in-time settlement and hedge the residual ZAR/USD exposure via WeWire’s OTC desk. Net effect: faster supplier payments, tighter cash buffers, less FX noise. Integrating stablecoins is a massive leap forward, but it requires the right infrastructure. WeWire is uniquely positioned to be the partner of choice for businesses seeking to revolutionize their treasury with stablecoins. WeWire recognized the pain points in global B2B transactions, particularly across emerging markets, where transaction times and costs are prohibitive. By leveraging stablecoin rails, WeWire provides an integrated suite of financial services that tackles every major treasury challenge: By partnering with WeWire, businesses don’t just adopt stablecoins; they gain a seamless, compliant, and integrated treasury system designed for the future of global finance. Stablecoins are no longer a curiosity in treasury—they’re a tactical instrument for liquidity, speed, and cost control. With clear policies, diversified rails, tight compliance, and auditor-ready accounting, finance teams can harness their advantages without compromising governance. If you’re ready to modernize treasury without adding complexity, WeWire gives you the controls, coverage, and confidence to run both fiat and stablecoin playbooks—on one pane of glass. Want the deeper dive? Grab our eBook, The Business Guide to Stablecoins – Unlocking Cost-Effective Cross-Border Payments, and see how leading teams are putting these practices to work.

diadem445c3650ff

Why stablecoins belong in modern treasury

Best Practices for Risk Control and Diversification

1. Counterparty and Issuer Risk Due Diligence

2. Operational and Security Risk Mitigation

Holding and Hedging Strategies

Strategic Holding

Hedging Currency Volatility

Accounting and Regulatory Challenges

The Accounting Conundrum

Navigating the Regulatory Landscape

Three practical scenarios

1. Cross-border supplier payments (Africa → EU)

2. Marketplace payouts

3. FX volatility buffer

Risk checklist

Why teams pick WeWire for stablecoin-enabled treasury

The takeaway

Africa’s EV Critical Minerals Push — Which Countries Are Poised to Be Suppliers, and Which Are Left Behind

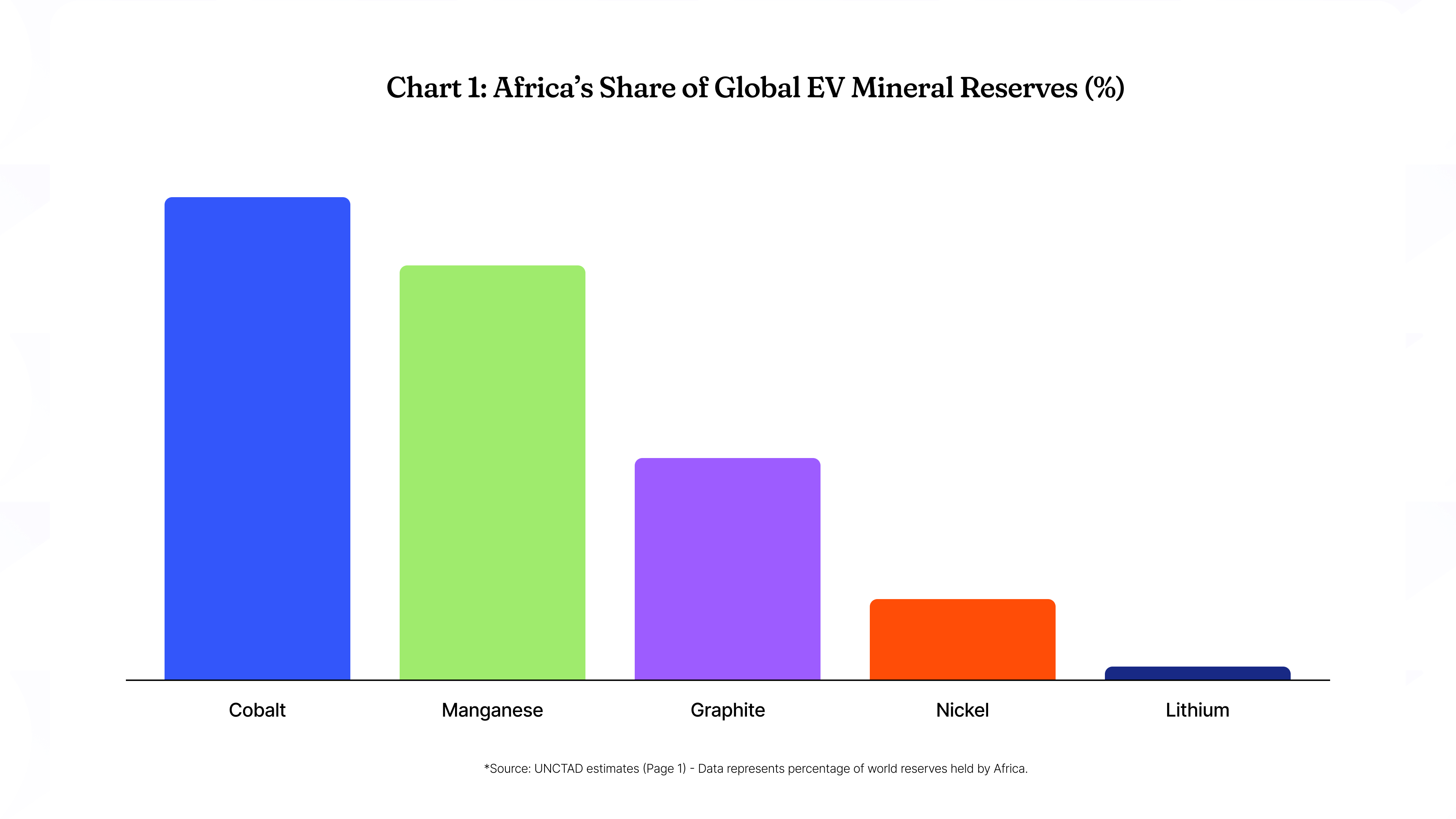

October 27, 2025 by diadem445c3650ff Africa is richly endowed with the minerals needed for electric vehicles (EVs) – in fact, UNCTAD estimates Africa holds roughly 55% of the world’s cobalt reserves, 47.7% of manganese, 21.6% of natural graphite, 5.6% of nickel, and 1% of lithium. As global EV demand surges, these deposits have drawn intense interest. African governments and companies are racing to expand mining and processing of lithium, cobalt, nickel, graphite, and manganese, the key battery metals. However, success varies widely. Some countries have the right mix of resources, policy suppor,t and infrastructure to become long-term EV-supply hubs, while others risk falling behind due to weak regulations, poor infrastructure or governance challenges. African mines like this rare-earth operation in South Africa underscore the continent’s mineral wealth. Global demand for EV battery materials is shifting the calculus of African resource development. Lithium: Africa’s largest lithium reserves are in Zimbabwe and Mali, with growing deposits in Namibia, Ghana and the DRC. For example, Zimbabwe’s Arcadia project alone hosts ~42.3 million tonnes of lithium (Li₂O) reserves – among the world’s largest hard-rock deposits. Bikita (Zim.) can output ~300,000 t of spodumene concentrate per year. Namibia’s Karibib mine is mining spodumene (773,000 t over its life) for export. New mines are coming online: Mali’s Goulamina holds ~142.3 Mt @1.38% Li₂O, and Ghana’s Ewoyaa 35.3 Mt @1.25%. The DRC’s Manono lithium project (401 Mt @1.65%) is under development. By contrast, West Africa’s Nigeria and Burkina Faso have lithium occurrences but very limited exploitation. Overall, African lithium output is small today but poised to grow (Zimbabwe and Namibia are already shipping concentrates). Cobalt: The DRC dominates African cobalt – and the world – producing over 70% of global cobalt (around 170,000 t in 2023) and holding ~6.0 Mt of reserves (about half of the world total). Zambia produces modest cobalt (Munali mine ~4,000 t/yr) and has ambitious projects (FQM’s 30,000 t-planned Enterprise mine). No other African country is a significant cobalt player. Cobalt ore and hydroxide from the DRC are mostly exported to China and, increasingly, to Europe for refining. Other African nations have negligible cobalt output, so they are neither leaders nor major laggards in this mineral. Nickel: Africa’s nickel output is modest. Madagascar’s Ambatovy mine (co-owned by Sumitomo) has a nameplate capacity of ~60,000 t of Ni per year, though production has been disrupted by a pipeline issue. South Africa produces a few thousand tonnes annually as a byproduct of its PGM operations (e.g., Mogalakwena, Impala). Zambia recently opened Munali (≈4,000 t/yr) and is developing the 30,000 t/yr Enterprise project. Tanzania holds Africa’s largest undeveloped nickel deposit (Kabanga, ~4.4 Mt @2.2% Ni), but no production yet. Zimbabwe has major nickel projects (Sabi Star, Bindura) on hold due to financing. In sum, Africa has potential (notably Madagascar and Southern Africa), but its nickel production is small relative to global demand. Graphite: Major African graphite producers are Mozambique, Madagascar, and Tanzania. These three hold 69 Mt of reserves (≈21% of global). Mozambique’s Balama mine (Syrah Resources) has the world’s largest known graphite reserves (~16 Mt contained graphite) and produced 72,000 t in 2021. Madagascar’s Molo and Sahamamy mines together produced ~70,000 t in 2021. Tanzania has burgeoning projects (Mahenge, Nachu, Bunyu) expected to add hundreds of kt/year. (By contrast, countries like Nigeria or South Africa have minimal graphite output.) Africa supplied roughly 9% of global graphite in 2021 but stands to climb above 26% by 2026 if new Tanzanian mines come online. Almost all African graphite is currently exported as concentrate; downstream processing (flakes, anodes) is virtually non-existent on the continent. Manganese: Africa is a global powerhouse. South Africa alone has ~38% of world manganese reserves (~640 Mt) and was the world’s largest producer in 2021 (7.2 Mt, 36% global). Gabon has vast ore fields (250 Mt reserves by some accounts; 4% global according to one profile) and in 2021 was the #2 producer (4.34 Mt, 22% global). Ghana and Côte d’Ivoire also mine Mn (Ghana ~0.94 Mt in 2021). Combined, these four countries hold 43% of global manganese reserves. (Others: Nigeria has small Mn deposits but little output.) Traditionally, most African Mn was shipped to China and Europe for alloying. African governments increasingly impose export restrictions and local-processing rules to capture more value. In late 2022–2023, Zimbabwe banned exports of raw lithium ore, and by January 2027, plans to ban even lithium concentrate exports, aiming to spur local refining. Zimbabwe extended the ban in 2023 to all unprocessed base ores, including nickel and manganese (with exceptions for existing local processors). Namibia followed in 2023, banning exports of unprocessed battery metals (crushed lithium ore, cobalt, manganese, graphite, etc.) without special approval. Nigeria outlawed most raw-ore exports in 2022 to encourage domestic refining. Tanzania also announced (2024) that raw lithium and other ores must be beneficiated locally. In the DRC, the government long imposed a cobalt hydroxide export ban (2022–25) to favor local smelting; it has now replaced the ban with a quota system effective Oct. 2025. Gabon, which has ~25% of the world’s Mineral reserves, recently announced that from 2029, no manganese may leave the country unless at least partially processed. These policies are designed to attract downstream investment (refineries, precursor plants, battery factories). For example, South African firm Manganese Metal Company is building a $25 M plant to produce battery-grade manganese sulfate (5,000 t/yr) by 2026. The African Continental Free Trade Area (AfCFTA) is also seen as a tool to develop regional supply chains – it could allow producers like Mozambique, Madagascar, and Tanzania to export graphite concentrate to African processors rather than shipping everything to Asia. In several cases, mineral contracts and tax codes now favor local content and beneficiation: e.g. African governments have free-carried interests (e.g., Tanzania’s Kabanga nickel JV gives 16% free government equity) and new mining codes often raise royalties on pure ore exports. Infrastructure remains a mixed bag. South Africa, with the continent’s best transport network, has deep ports (Richard’s Bay, Saldanha), extensive rail linking mines (Kalahari Mn fields), and a continentalized road system – but chronic power shortages plague industry. Ghana and Mozambique have major ports (Tema, Maputo) and better power access, yet outside the main corridors, roads can be poor. The Africa Finance Corp’s 2025 report highlights the Lobito Corridor (Angola–DRC/Zambia rail) as a new corridor unlocking copper/cobalt exports. East African rail upgrades (e.g. Dar es Salaam corridor) similarly link Tanzanian graphite and copper belts to the coast. But outside these projects, most landlocked mines suffer. The AFC report notes “sharp disparities in road quality and density, with limited private participation outside mining corridors”. Power is a critical constraint: battery and steel processing are electricity-intensive. DRC and Zambia rely on hydro (Congo and Zambezi basins) but still impose rationing during droughts. South Africa, despite having the continent’s largest grid, regularly enforces blackouts. Ghana and Namibia have relatively stable grids (Namibia draws on hydropower and solar) – a reason the EU and US favour these as secure partners. Lack of affordable, reliable power may sideline some potential producers: for example, proposals for lithium refineries in remote Zimbabwe sites could struggle without new power plants. In summary, only a few countries (South Africa, Namibia, Ghana) currently have the mix of ports, rails and grids to fully support large-scale processing; others must invest heavily in infrastructure or rely on partners (e.g. Chinese-built smelters) to bridge the gap. China remains by far the dominant external player in Africa’s battery-mineral sector. It has funded mines and refineries across the continent – from Congolese copper/cobalt (Sicomines infrastructure-for-minerals deals) to Zimbabwean lithium mines and South African PGMs. Chinese state firms own or part-own key projects: e.g. China Molybdenum’s purchase of Congo’s Tenke Fungurume (3.3 Mt Co resource) and sponsorship of Zimbabwe’s Arcadia (Huayou Cobalt) and Bikita expansions. China also invests in African power and transport tied to resource access. In manganese, China consumes >50% of world output and sources ~20% of that from Gabon, illustrating its strategic demand for African ore. Europe has launched “raw materials partnerships” with resource-rich African states. For example, the EU has signed agreements with the DRC, Namibia and Zambia to secure supply and promote local processing. European development finance is targeting Africa too: the EU recently labeled a Zambian cobalt sulfate plant (Kobaloni Energy) as a “strategic project,” signaling support. However, EU companies still invest far less than Chinese firms, partly due to African governments’ insistence on large stakes/value-add on-site. The United States and Allies are ramping up engagement. In 2025 the US and Abu Dhabi launched a $1.8 billion Orion Critical Minerals Fund to invest globally in battery metals projects. The US DFC has approved financing for projects in Angola, Mozambique, Tanzania and Zambia (including graphite and copper/nickel developments). In 2023 the US co-founded a Tripartite Strategic Alliance with Zambia and the DRC, aiming to boost mining, refining and battery manufacturing. Renewing trade preferences like AGOA is also seen as critical to keep African minerals flowing to Western markets. Overall, Western capitals now articulate mineral diplomacy (often as security policy) to counter Chinese influence – but so far Chinese capital and offtake deals dominate the ground game. Comparative Table of Leading vs Laggard Countries by Mineral The best-positioned countries are those combining large resources with stable policy and improving infrastructure: Conversely, the laggards or at-risk countries are those with one or more of: modest deposits, poor governance/infrastructure, or unstable policy. Examples include: In summary, Africa’s EV minerals scene is at a crossroads. Countries with large endowments and stable, business-friendly environments (DRC, South Africa, Namibia, Zambia, Ghana, Madagascar, Gabon) are best poised to become major suppliers and possibly processors. Those with resources but facing governance or infrastructure shortfalls (Nigeria, Zimbabwe, unstable Sahel states) risk being left behind or remaining mere raw suppliers. Continental initiatives (like the African Union’s 2024 Green Minerals Strategy) signal a collective ambition to “industrialize through local beneficiation”, but realizing this will require massive investment in power, transport, and skills. The coming decade will likely see an acceleration of investment in African battery minerals – with winners and losers determined by policy choices and the ability to build a local value chain alongside extraction.

diadem445c3650ff

EV Mineral Endowments by Country

Policy and Value-Addition Regimes

Policy and Value-Addition RegimesInfrastructure Capacity

Investment Trends and Geopolitical Players

Mineral

Leading African Suppliers (Reserves/Output)

Lagging/Untapped Countries

Lithium

Zimbabwe (largest African reserves, Arcadia ~42 Mt), Mali (Goulamina 142 Mt), Ghana (Ewoyaa 35 Mt), Namibia (Uis, Karibib)

Nigeria (known deposits, no mining), DRC (Manono deposit under development)

Cobalt

DRC (>$170,000 t/yr, 6 Mt reserves), Zambia (tens of kt/yr)

Others (South Africa, Madagascar have minor Co resources but no large production)

Nickel

Madagascar (Ambatovy ~60 kt/yr capacity), South Africa (Mogalakwena ~15 kt/yr by-product), Zambia (Munali ~4 kt, Enterprise planned)

Tanzania (Kabanga resource), Zimbabwe (Sabi Star deposit) – both mostly undeveloped

Graphite

Mozambique (Balama – 16 Mt contained, 72 kt prod ‘21), Madagascar (~26 Mt reserves, 70 kt ‘21), Tanzania (Mahenge/others)

Nigeria (small reserves), South Africa (historic mines), others minimal

Manganese

South Africa (640 kt reserves, 7.2 Mt prod ‘21), Gabon (61 kt reserves, 4.3 Mt ‘21), Ghana (13 kt reserves, 0.94 Mt ‘21), Ivory Coast

DRC (some Mn but little investment), Nigeria (minor Mn), Botswana (tiny output)

Opportunities and Risks: Who Rises, Who Falls

Opportunities and Risks: Who Rises, Who Falls

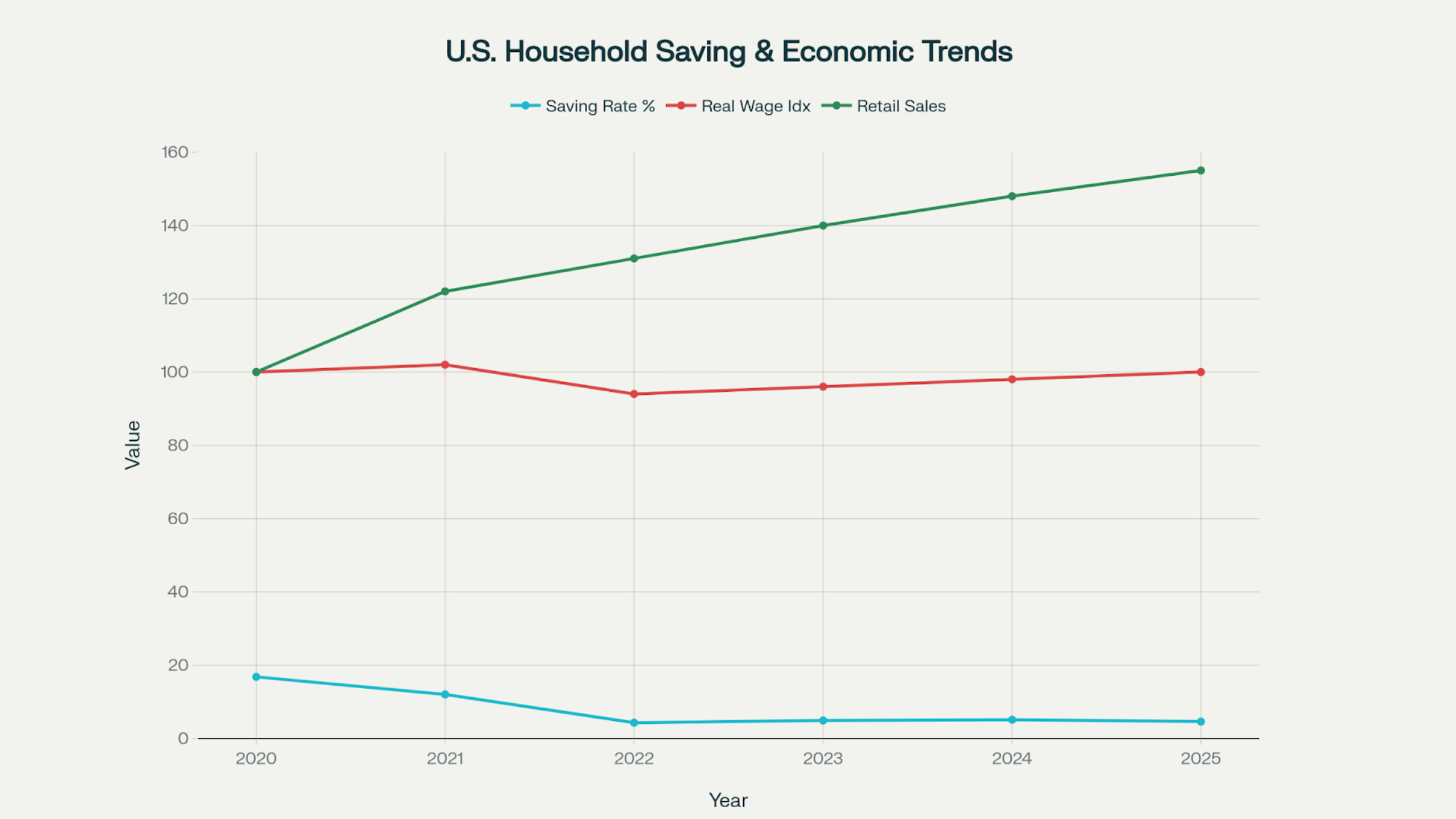

Consumers Are Broke, But Sales Are Booming: Welcome to the Credit Economy

October 22, 2025 by diadem445c3650ff Across the world, a striking contradiction has emerged: consumers report feeling financially squeezed even as retailers report rising sales. In many advanced economies household savings have plunged and real wages are barely keeping up with inflation, yet spending remains robust. For example, by 2025 the U.S. personal saving rate had fallen to only about 4–5%, among the lowest levels of the past decade, even as retail sales jumped (up ~5% year-on-year in mid‑2025). Major banks and analysts now talk of a “resilient” or “stretched” consumer: a situation where apparent demand is largely bankrolled by borrowed money rather than rising income. U.S. banking CEOs note that consumers seem to be spending freely (with credit card delinquencies below expectations), but much of this is credit-fueled rather than salary-fueled. Detailed data show the roots of this paradox. Real incomes have been weak: inflation-adjusted wages grew modestly in 2024–25, and in many countries still lag pre‑pandemic levels. An OECD study notes that even as average real wages have started to recover, in about two‑thirds of member countries they remain below their early‑2021 peaks. Meanwhile inflation and costs have surged (housing, food, energy), eroding spending power. Households have responded by cutting savings or drawing down reserves. What explains the disconnect is debt. Credit balances have surged, effectively bridging the income shortfall. In the United States, total household debt has climbed to about $18.4 trillion by mid-2025. Non-mortgage debts are rising especially fast: credit card balances reached roughly $1.21 trillion in Q2 2025 (nearly 6% higher than a year earlier), and auto loans hit $1.66 trillion. This is mirrored by an upswing in new lending: large banks report record credit-card spending and mortgage originations. Notably, much of the credit growth is tied to higher‑income households: recent Federal Reserve analysis shows that affluent consumers have raised their credit spending aggressively (and carry lower debt relative to income), whereas middle‑income and poorer households have spent less and amassed proportionally more debt. Beyond traditional loans, new forms of credit are proliferating. Buy-Now-Pay-Later (BNPL) plans and digital microloans have exploded in the past few years, especially among younger shoppers. U.S. regulators report that BNPL lending leapt from $2.0 billion in 2019 to about $24.2 billion in 2021, and industry growth suggests roughly $36 billion by 2024. Consumer surveys indicate roughly one‑fifth of Americans have used BNPL in the past year, often for clothing or electronics. Economist analyses find that BNPL significantly boosts short‑term spending (by effectively discounting immediate prices) at the expense of future liquidity. In many developing countries, mobile lending apps play a similar role: for example, in Nigeria over half of survey respondents said they took a loan or credit in the past year to meet everyday needs The flip side of the credit boom is vulnerability. With households and governments more leveraged, higher interest rates and any credit squeeze could trigger trouble. Central banks around the world have kept policy rates elevated to fight inflation, meaning debt servicing costs are climbing. U.S. consumers now pay record interest on revolving debt (credit card rates are around 20%), and many emerging‑market borrowers face even higher rates. Surveys note that a nontrivial share of households are already caught in debt spirals – for example, roughly 4% of Nigerian respondents said they were borrowing simply to repay existing loans. Credit delinquencies are still relatively low, but they have begun inching up in 2024–25 in some markets. Regulators have taken notice: the UK and EU are moving to regulate BNPL, and many banks have tightened underwriting. In sum, the “credit economy” paints a picture of temporary prosperity. Sales and GDP figures remain strong today, but this demand is increasingly financed by borrowing rather than actual income gains. Analysts note that much of the current growth may reflect consumers “front‑loading” purchases and using credit to smooth through high prices. The risk is that when borrowing stops or when debts come due under tighter money, the boom will reverse sharply. Policymakers and businesses are now charting credit trends more closely, recognizing that traditional indicators (retail sales, retail inventories, etc.) no longer tell the full story of household health. The bottom line: we live in a credit‑driven economy, where headline strength masks deeper strain. The next downturn, should one occur, may be defined by these hidden debts and the limits of synthetic demand.

diadem445c3650ff

In the U.S., the official saving rate has tumbled to roughly 4–5% of income (from double digits during the pandemic), indicating far less buffer for rainier days. Emerging markets show similar strains: for example, many Nigerians report slashing non‑essential spending or borrowing to cover basics as prices soar. Yet total consumption figures keep growing. U.S. retail sales as of late 2025 were significantly above year-ago levels, and anecdotal reports from Africa and Asia likewise note stable or rising demand for staples even as budgets pinch.

In the U.S., the official saving rate has tumbled to roughly 4–5% of income (from double digits during the pandemic), indicating far less buffer for rainier days. Emerging markets show similar strains: for example, many Nigerians report slashing non‑essential spending or borrowing to cover basics as prices soar. Yet total consumption figures keep growing. U.S. retail sales as of late 2025 were significantly above year-ago levels, and anecdotal reports from Africa and Asia likewise note stable or rising demand for staples even as budgets pinch.

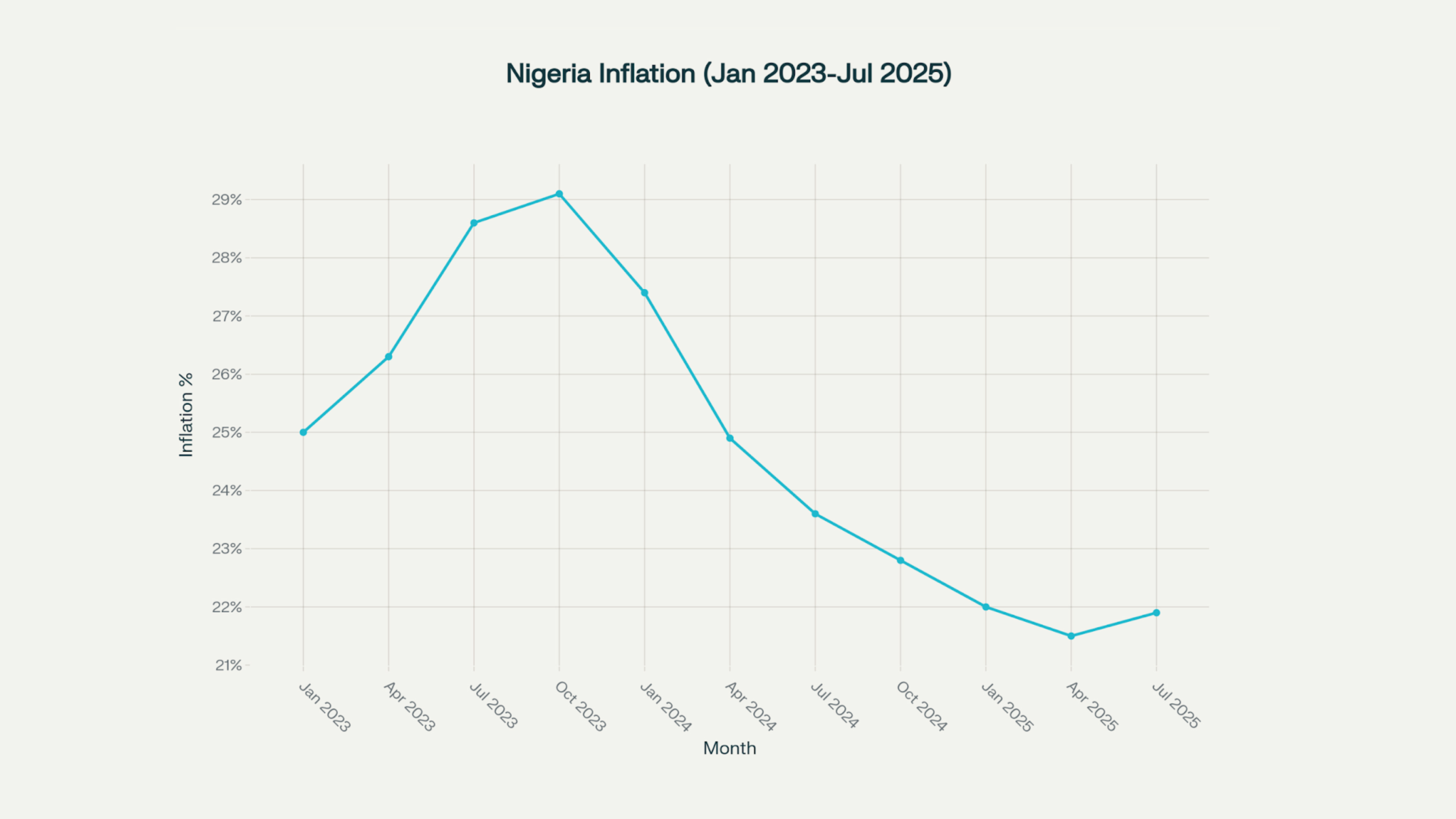

How Stablecoins Are Redefining Savings in High-Inflation Economies

October 8, 2025 by diadem445c3650ff Across many emerging markets, blockchain-based stablecoins like USDT and USDC are supplanting traditional dollar savings. In countries where inflation is rampant and foreign exchange is restricted, people increasingly keep value in tokenized dollars rather than local cash. Stablecoins are crypto tokens pegged 1:1 to the U.S. dollar and backed by reserves, so they effectively act as digital dollar accounts. For example, Nigeria’s inflation ran near 21.9% in mid-2025 – so a Nigerian saver might move funds into USDT to prevent the naira’s erosion. As Morgan Stanley notes, in such environments stablecoins “are often considered a store of value, protecting against local currency depreciation”. In short, USDT provides 24/7 access to dollars through a smartphone, a practical hedge for households and businesses when official dollar accounts are scarce or expensive. In high-inflation economies from Nigeria to Argentina, local currencies are losing value fast. Nigeria’s consumer prices hit 21.9% (year-on-year) in July 2025, and many African currencies have weakened dramatically. Governments often impose strict foreign‐exchange (FX) controls, making legal dollar accounts hard to open. This erodes trust in fiat and pushes savers to alternatives. A recent Chainalysis study finds that Nigeria has received roughly $92.1 billion in crypto inflows over 12 months, nearly three times South Africa’s volume, driven largely by inflation and limited forex access. In this context, crypto analysts and reporters emphasize that stablecoins can “mirror the strength of the U.S. dollar” and fill the vacuum. Data from African crypto platforms confirm the trend. A Yellow Card–sponsored report finds stablecoins now represent about 43% of all crypto trading volume in sub-Saharan Africa, with Nigeria alone accounting for ~$22 billion over a one-year period. Practically every young trader or remittance sender there is increasingly using tokens like USDT instead of withdrawing dollars. Yellow Card itself says 99% of its transactions are in stablecoins (USDT alone is 88.5% of their volume). Roughly 70% of Yellow Card’s users report using these tokens for personal remittances or savings. This data highlights the point: for many people, USDT isn’t speculation – it’s a lifeline. Savers use it as a “digital dollar account” to park money. The technical plumbing behind this shift involves crypto exchanges and mobile‐money interfaces. Africans often buy USDT on P2P networks or fintech apps. For example, global exchanges’ peer-to-peer desks (like Binance P2P) allow users to trade naira or shillings for Tether directly at market rates. Local startups such as Yellow Card, Bitnob or Bundi provide instant rubicon between Tether and mobile wallets or bank accounts. As Cointelegraph reports, some freelancers in Kenya now invoice clients in USDC and receive payouts in M-Pesa within minutes. In Nigeria, reporters note traders maintain working capital in USDT to avoid naira crashes. Chainalysis data back this up: in Nigeria, every transaction under $1 million in one quarter was in stablecoins, totaling about $3 billion. This dollarization trend isn’t limited to Africa. Latin America’s high-inflation economies show similar patterns. Chainalysis notes that four LatAm countries rank among the top 20 globally for grassroots crypto adoption. In Argentina – which saw inflation over 100% – stablecoins dominate local crypto trading. About 61.8% of Argentina’s crypto transaction volume is now in stablecoins (versus ~44.7% global average). Every time the peso fell last year, Argentinians quickly piled into USDT on local exchanges. Venezuela’s population has also fled into crypto (BTC and stablecoins) as the bolívar collapsed; indeed, Venezuelan crypto inflows grew 110% YoY even while the government experimented with its own “petro” token In summary, USDT and its peers have quietly become the new “dollar accounts” for many in high-inflation countries. Instead of speculating, everyday users treat these tokens as simple tools to protect their savings from eroding local currencies. This shift is still a small fraction of the global monetary system – stablecoins today represent a few tenths of a percent of world money supply – but the growth is striking. The total stablecoin market cap jumped from about $5 billion in early 2020 to roughly $300 billion by late 2025, driven in part by usage in emerging markets. Looking forward, stablecoins could become even more mainstream: financial giants and tech firms are racing to integrate them into payments, and a wave of central bank digital currencies (CBDCs) is on the way as governments try to offer an official digital alternative.

diadem445c3650ff