How Stablecoins Work for Fintech Payments

June 20, 2025 by diadem445c3650ff The world of digital finance is rapidly evolving, and at its core, a quiet revolution is underway, powered by stablecoins. These digital assets are far more than just “crypto” – they are designed to bring the efficiency and speed of blockchain to the predictability of traditional money. For fintech companies, understanding precisely how stablecoins work for fintech payments isn’t just about staying current; it’s about unlocking unprecedented opportunities for faster, cheaper, and more inclusive global transactions. At WeWire, we’re helping forward-thinking fintechs unlock the full potential of stablecoin-powered payments. Through our API infrastructure, businesses can easily transition between fiat and stablecoins, issue virtual accounts, and make direct stablecoin payouts across Africa and beyond—without taking on the heavy lifting of compliance or infrastructure management. Stablecoins are digital assets pegged to the value of traditional currencies like the U.S. dollar or euro. Unlike volatile cryptocurrencies, stablecoins maintain price stability, making them ideal for payments. Popular stablecoins like USDC, USDT, and EUROC are widely accepted, liquid, and built on public blockchains such as Ethereum or Solana. According to Chainalysis, Africa’s cryptocurrency market grew over 1,200% between 2020 and 2021, with stablecoins playing a major role in cross-border settlements and business payments. This growth reflects rising demand for alternative rails that bypass the delays and fees of SWIFT and legacy banking systems. Stablecoins are digital tokens pegged to stable assets, predominantly fiat currencies like the U.S. dollar. This peg allows them to maintain a consistent value, unlike volatile cryptocurrencies such as Bitcoin. Their stability, combined with the speed and transparency of blockchain technology, makes them ideal for financial applications. Here’s how stablecoins work for fintech payments, solving the pain points of traditional systems: Stablecoins enable instant, borderless, and low-cost transactions. Here’s how WeWire helps fintechs—remittance providers, PSPs, and payroll services—tap into this innovation: Remittance businesses are under pressure to cut costs and improve settlement speed. Traditional corridors from Europe, the U.S., or Asia into African markets often face delays of 2–5 days with up to 10% in fees, especially in markets like Nigeria, Ghana, or Kenya. How WeWire Helps: Result: Faster settlements, reduced FX exposure, and complete compliance coverage handled by us. Payment service providers across Africa face fragmented banking rails, high FX risk, and regulatory complexity. Merchants want faster settlement and lower fees, especially for cross-border sales. How WeWire Helps: Result: Seamless integration, reduced settlement risk, and global reach for your merchants. As more companies hire globally, cross-border payroll is becoming a headache. Paying developers, contractors, or teams in Africa involves multiple intermediaries, FX losses, and long delays. How WeWire Helps: According to a 2023 report by Deel, over 70% of remote workers in Africa prefer to be paid in USD or stablecoins due to local currency volatility. ✅ Result: Streamlined, fast, and globally compliant payroll for distributed teams. At WeWire, we’ve built a robust, compliant and developer-friendly platform that bridges the gap between fiat and stablecoins for African and global fintechs. WeWire provides all the backend infrastructure, so your team can focus on building great customer experiences—not rebuilding banking rails. Join leading fintechs using WeWire to simplify payments, cut costs, and expand globally. Let’s build the future of digital finance—together.

diadem445c3650ff

What Are Stablecoins and Why Do They Matter?

How Stablecoins Revolutionize Fintech Payments

For Remittance Companies: Issue Accounts, Settle in Stablecoins

For PSPs: Convert Fiat to Stablecoins, Settle Merchants Globally

For Payroll Platforms: Pay Remote Teams in Stablecoins

Why Choose WeWire for Stablecoin Payments?

🔧 Key Features:

Ready to Embed Stablecoin Payments into Your Product?

👉 Talk to Sales

Stablecoin vs Crypto: What’s the Difference and Why It Matters in the Future of Digital Finance

June 16, 2025 by diadem445c3650ff The world of digital assets often feels like a blur of complex terminology. Two terms frequently used, and often confused, are “crypto” and “stablecoin.” While both exist on the blockchain, their core functions and, crucially, their risk profiles are as different as night and day. Understanding the distinction between Stablecoin vs Crypto isn’t just for blockchain enthusiasts; it’s vital for any business navigating the modern global economy, especially those involved in cross-border payments. Cryptocurrency is no longer just a buzzword—it’s a building block of modern finance. But if you’ve ever tried to explain Bitcoin to a non-crypto friend, you’ve probably hit a wall right around the “price dropped 20% overnight” part. That’s where stablecoins enter the picture. In this post, we’ll break down what makes stablecoins and cryptocurrencies different, why that matters, and how WeWire is using stablecoin rails to make cross-border payments faster, cheaper, and less risky. Whether you’re an individual, a startup, or a business operating across borders, understanding the differences can help you make smarter financial decisions. When we talk about “crypto” in the general sense, we’re typically referring to cryptocurrencies like Bitcoin (BTC) or Ethereum (ETH). Cryptocurrencies like Bitcoin (BTC), Ethereum (ETH), and Solana (SOL) are decentralized digital assets. Their value is driven by market forces—supply, demand, investor sentiment—and in many cases, hype. These digital assets represent a revolutionary shift in how value can be transferred and stored, operating on decentralized blockchain networks without the need for traditional banks. However, the defining characteristic of these traditional cryptocurrencies is their inherent volatility. Their value is largely driven by market speculation, investor sentiment, and global economic shifts. This makes them highly unpredictable: This is where stablecoins enter the picture as a game-changer. Unlike their volatile cousins, stablecoins are specifically engineered to maintain a stable value. They achieve this by pegging their value to a more stable asset, most commonly a fiat currency like the U.S. dollar, or sometimes other major currencies or even commodities. Think of a stablecoin as a digital representation of traditional money that lives on a blockchain. It offers the speed and efficiency of crypto transactions but without the dizzying price swings. Here’s why stablecoins are fundamentally “less risky” for business operations than volatile cryptocurrencies: For any B2B company operating internationally, understanding the fundamental difference between Stablecoin vs Crypto is paramount. Trying to manage payroll or pay suppliers using a highly volatile asset would introduce unacceptable financial risk. Stablecoins, however, open up a world of possibilities for streamlining global payments: So where does that leave us in the stablecoin vs crypto debate? Both have a place in the future of finance. But for businesses looking to cross borders and scale globally, stablecoins are the bridge between the volatility of crypto and the rigidity of traditional banking. At WeWire, we’ve built our payment solutions with a clear vision: to make cross-border payments seamless, efficient, and reliable for businesses worldwide. We recognize that while the broader “crypto” market is innovative, it’s the stability and utility of stablecoins that truly offer a practical advantage for B2B operations. Our platform strategically integrates stablecoin rails, allowing your business to unlock these benefits directly: The distinction between Stablecoin vs Crypto is not just semantic; it’s foundational. While cryptocurrencies push the boundaries of decentralized finance, stablecoins are providing the stable, reliable digital infrastructure that businesses need to thrive globally. For any enterprise seeking to reduce risk, cut costs, and accelerate payments in the interconnected world, embracing stablecoins through a trusted partner like WeWire is no longer an option – it’s a strategic imperative.

diadem445c3650ff

What is “Crypto” (Cryptocurrencies) and Why They Come with More Risk

Stablecoin vs Crypto: The Case for Stability and Lower Risk

Why the Distinction Between Stablecoin vs Crypto Matters Immensely for Global Businesses

Stablecoin vs Crypto: Use Each for What They’re Best At

WeWire: Leveraging Stablecoin Rails for Your Global Advantage

Why Your Business Needs a Virtual Account in Its Own Name

June 13, 2025 by diadem445c3650ff Every day, payments are being made, whether on a large scale or just for personal needs, locally or internationally. But things get a bit more complex with international business transactions. Whether you’re a freelancer receiving international payments, an SME expanding into new markets, or a large corporation managing complex cross-border transactions, the efficiency and trustworthiness of your payment infrastructure are paramount. This is where a virtual IBAN in your business name becomes a game-changer. Before diving into the benefits, let’s clarify what we’re talking about. A traditional IBAN (International Bank Account Number) is a unique identifier for a bank account, typically linked directly to a physical bank account held with a financial institution. On the other hand, a virtual IBAN (International Bank Account Number) or Virtual account is a unique account number issued by a virtual banking provider or payment institution. Unlike traditional IBANs tied to a physical bank account, virtual IBANs are digital proxies that route payments to a master or pooled account. What makes a business virtual account especially powerful is that it’s registered in the company’s legal name—not a generic or third-party name. This small shift has big implications: clients see your company name on payment instructions, invoices, and statements, enhancing trust and eliminating confusion. A virtual bank account for companies isn’t just a modern convenience—it’s a strategic advantage. Here’s why: Having a virtual IBAN in your business name helps establish legitimacy in the eyes of partners, suppliers, and clients. It reinforces that they’re dealing directly with your company—not a payment aggregator or third party. When each customer or revenue stream is assigned a unique virtual IBAN, incoming payments are automatically tagged and routed, reducing manual reconciliation and accounting errors. Virtual IBANs are tailor-made for cross-border payments for businesses. They allow you to collect payments in multiple currencies, often locally, reducing FX fees and settlement times. Unlike pooled accounts where multiple transactions are lumped together, virtual IBANs provide detailed visibility into who paid what and when—improving cash flow management and audit readiness. Transparency is a non-negotiable in modern business. With a business virtual IBAN account, your clients and vendors can verify payment origin and destination, as your business name is clearly attached to all transfers. This is especially critical in industries where trust is paramount—like legal services, fintech, e-commerce, and professional consulting. Using a virtual account for international payments removes the ambiguity often associated with third-party payment processors, preventing delays or flagged transactions. Whether you’re a entrepreneur or a scaling enterprise, a virtual account in your company’s name offers serious advantages: Getting a virtual account in your business name is a straightforward process, especially with specialized providers like WeWire. While specific steps may vary, the general process involves: By leveraging the power of a virtual account in your business name, your company can significantly enhance its trust, transparency, and global reach, ultimately paving the way for smoother international operations and accelerated growth. Ready to future-proof your cross-border payments with a virtual IBAN in your business name?

diadem445c3650ff

What is a Virtual Account in Your Business Name?

Benefits of Having a Virtual Account Registered to Your Company

1. Boosted Professional Credibility

2. Faster Reconciliation

3. Streamlined Cross-Border Payments

4. Enhanced Control and Visibility

How It Improves Payment Transparency and Credibility

Use Cases: Virtual Accounts for Freelancers, SMEs, and Global Businesses

How to Get a Virtual IBAN in Your Business Name

Let’s cross borders together—Explore WeWire’s virtual account solutions.

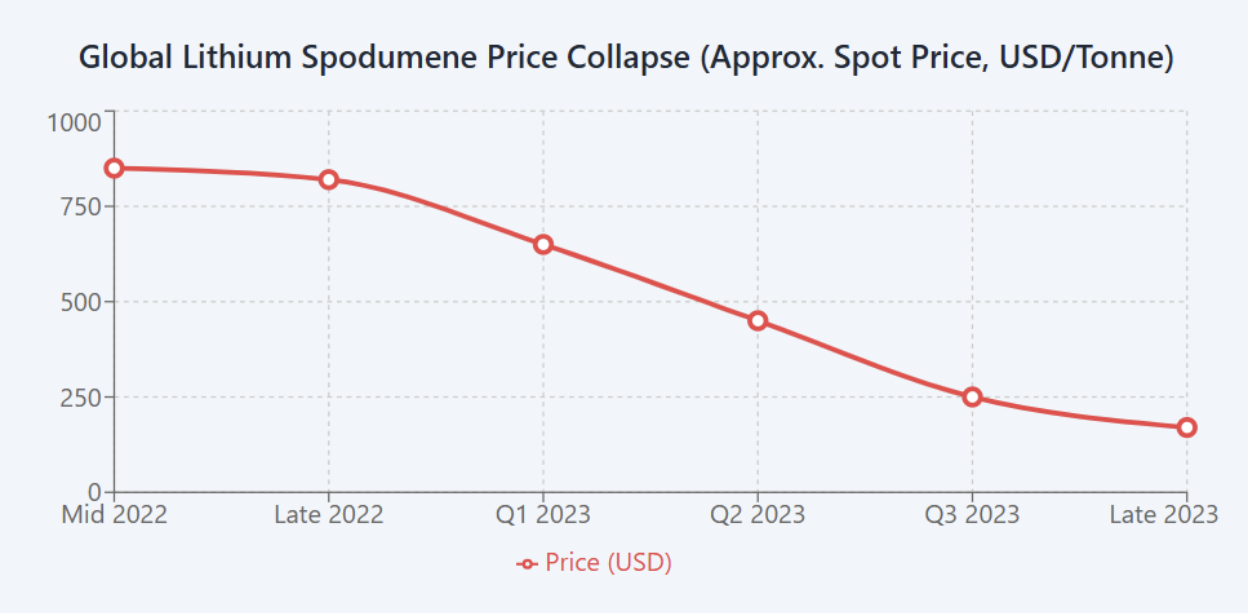

An Analysis of Africa’s Lithium Crash: From $850/T Highs to an 80% Collapse — What It Means for Exporters Like Zimbabwe

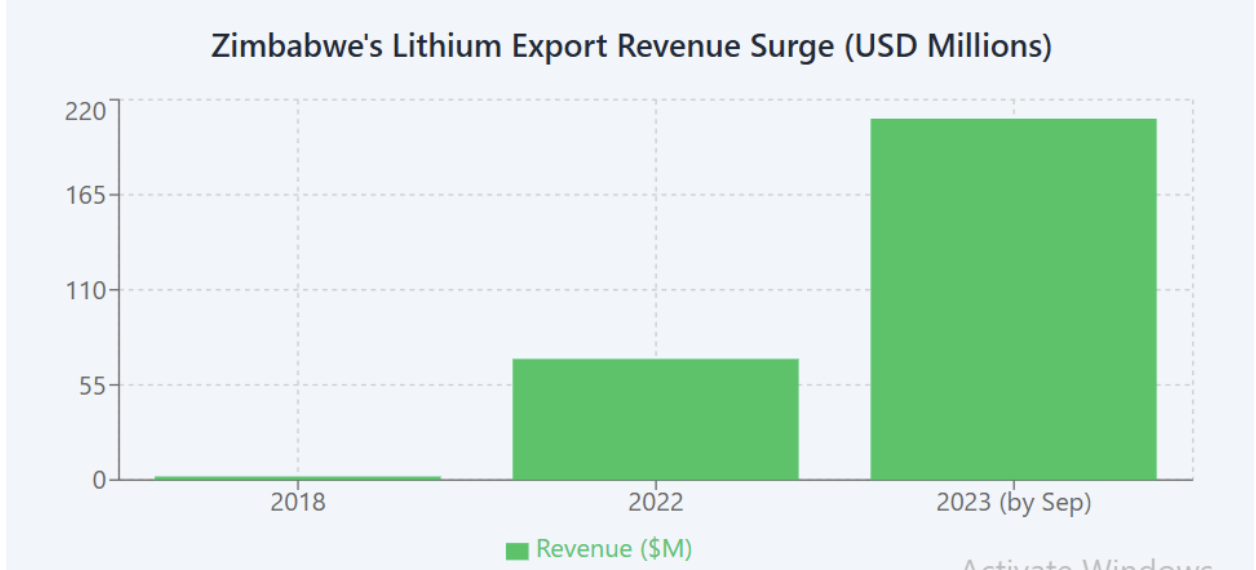

June 13, 2025 by diadem445c3650ff The lithium market saw a dramatic boom-and-bust cycle in the early 2020s. Prices for lithium products shot up through 2021–22 (for example, Chinese spot prices for spodumene concentrate briefly hit about $850/tonne) as electric vehicle (EV) and battery demand surged. However, by mid-2023, global oversupply (especially from China) and weaker-than-expected EV sales triggered a collapse of roughly 80%. By late 2023, lithium prices – from hard-rock concentrates to refined carbonate – had plunged to levels near 20% of their late-2022 highs. This reversal forced major producers (e.g., battery maker CATL) to suspend some mining operations and led top miners like Albemarle to cut costs and jobs. In short, the market turned sharply from a seller’s paradise to a buyers’ market, with prices tumbling about 80% in roughly one year. Zimbabwe holds the largest lithium reserves in Africa and is rapidly becoming a new frontier for battery minerals. Beginning around 2020, Chinese firms flocked to Zimbabwe. For example, Zhejiang Huayou Cobalt spent ≈$422 million to acquire the Arcadia lithium project, and Sinomine Resources paid hundreds of millions for the Bikita mine. By 2022, Zimbabwe’s lithium sector was tiny (≈800 tonnes produced in 2022) but poised to expand. The government moved quickly to ban raw (unprocessed) lithium exports in late 2022, aiming to force value-added processing. With these investments, production and exports surged. Output jumped to about 14,900 tonnes in 2023 and 22,000 tonnes in 2024. Export revenue reflected this boom: lithium went from less than $2 million in 2018 to roughly $70 million in 2022, then to $209 million by September 2023. By late 2023, lithium was on track to become Zimbabwe’s third-largest mineral export (after gold and platinum). In sum, a 2020s investment frenzy lifted Zimbabwe from near-zero lithium production to tens of thousands of tonnes in just a few years. Lithium concentrate being loaded at the Prospect Lithium (Arcadia) mine in Goromonzi, Zimbabwe (January 2024). Chinese firms like Huayou Cobalt and Sinomine have invested over $1 billion in Zimbabwe’s lithium projects. As of 2024, nearly all Zimbabwean lithium was shipped as concentrate to China for further refining. The sharp price collapse has put these operations under severe strain. Zimbabwe’s lithium miners – overwhelmingly Chinese-owned – have been cutting output and staff. According to government and industry reports, sustained price declines (~80% from late-2022) “have made it difficult for lithium companies to stay afloat,” forcing many to downscale production and lay off workers. For example, Sinomine (owner of Bikita) told legislators its Zimbabwe unit is operating below capacity due to the slump. In some cases, even large investors have paused new projects until prices recover. Operating challenges have exacerbated these financial pressures. Zimbabwe’s deteriorating infrastructure and economic policies raise production costs. Miners report that weak roads, unreliable power and water, and logistical bottlenecks in rural mining regions significantly increase costs. Currency controls add another burden: Sinomine notes that a rule forcing export earnings to be converted (at a loss) into Zimbabwe’s local currency erodes miner revenues. In short, “fragile power supply, capital constraints, and foreign currency shortfalls” are impeding production. At the same time, a large informal sector has sprung up around lithium. NGO investigations estimate ~5,000 artisanal miners were operating in Zimbabwe by late 2022, using primitive methods (picks, wheelbarrows) to extract ore. These small-scale miners often sell raw lithium ore at very low prices (around $100–$150 per tonne) to local buyers or traders. Much of this ore is reportedly smuggled into neighboring countries. The result is a massive leakage of value: material worth thousands of dollars on world markets is sold for only a few hundred locally. This means Zimbabwe’s impoverished artisanal diggers see little benefit from the lithium boom, while the state foregoes tens of millions in export earnings. Overall, Zimbabwe’s lithium mining sector has been forced into retreat. Initial production gains are flattening or reversing as companies cope with the downturn. Some Chinese investors are even rethinking timelines; for instance, Kuvimba Mining (state-owned) pressed ahead with a new concentrator only on the expectation of a future price rebound. But currently, most exporters are in survival mode. In response to both the boom and the bust, Harare has enacted a mix of incentives and restrictions. In December 2022, it banned unprocessed lithium exports, and in June 2025 extended this to a formal ban on all lithium concentrate exports effective January 2027. The aim is to force foreign mining companies to build processing plants in Zimbabwe. Indeed, plans are underway: Sinomine’s Bikita and Huayou’s Arcadia each have lithium-sulphate/refinery projects in development, targeting local conversion of concentrate. The Minister Winston Chitando has stated that once these facilities are ready, “the export of all lithium concentrates will be banned from January 2027”. However, as prices collapsed, the government has shown more flexibility. In late 2024, Deputy Minister Polite Kambamura said authorities would now assess miners’ plans “on a case-by-case basis” rather than enforcing blanket deadlines. Previously, companies had been given until March 2024. Facing pressure from struggling miners, the government softened these requirements while still emphasizing its value-added goals. Zimbabwe has also introduced fiscal measures on lithium exports. In 2023 it imposed a 5% export levy on lithium concentrates to raise state revenue. This policy has been controversial: Zimbabwe’s Lithium Exporters Association (including major Chinese firms) has petitioned to delay the tax until 2027, arguing it should coincide with the launch of local processing plants. Industry sources note that policy reversals and quick changes (like these bans and taxes) have created uncertainty. Indeed, NGOs describe the export ban as a “knee-jerk reaction” to the resource rush, warning that erratic rules could scare off further investment. In summary, the government’s approach balances two goals: capturing more value by building domestic refineries and keeping the mining sector alive amid a brutal price crash. It remains to be seen whether Zimbabwe can steadily develop its lithium industry without undermining investor confidence. Lithium is a strategic commodity, and Zimbabwe’s experience is tied to broader global rivalries. Chinese companies dominate Zimbabwe’s lithium sector: besides the >$1B invested overall, specific deals highlight this control (e.g., Huayou’s Arcadia, Sinomine’s Bikita). This fits China’s global strategy to secure critical minerals for its EV and battery industries. In turn, Zimbabwe’s “Look East” policy and political ties have made Beijing its favored partner for resource development. Western mining firms have largely shunned Zimbabwe due to political risk and sanctions concerns, leaving Chinese firms free to set the terms. As a result, most of Zimbabwe’s lithium is shipped to China for processing (usually via subsidiary refineries or commodity traders). Beijing’s vast battery production capacity can absorb this supply, but it also means Zimbabwe has limited leverage. In the oversupplied lithium market, Chinese consumers can squeeze exporters’ margins. Geopolitically, Zimbabwe’s rise as a lithium supplier may boost its strategic importance to China, but it also makes Harare heavily reliant on one buyer amid a volatile market. Regionally, Africa’s other lithium projects (in Namibia, DRC, etc.) are also attracting foreign interest, but Zimbabwe remains the continent’s biggest producer. Global moves to diversify away from China (e.g., U.S./EU seeking alternate sources) may put further pressure on Chinese-backed projects. For now, however, Zimbabwe sits squarely in China’s orbit for batteries – for better or worse. Zimbabwe’s lithium story shows both opportunity and risk. The country’s vast reserves and recent investments promise future growth, but the recent 80%-plus price crash exposes vulnerabilities. By adopting stable policies, supporting miners through the downturn, and investing in value-added production, Zimbabwe can maximize the long-term benefits of its lithium wealth. If it navigates these challenges wisely, Zimbabwe could emerge not just as an exporter of raw ore, but as a lasting participant in the global battery supply chain.

diadem445c3650ff

Zimbabwe’s Lithium Boom (2020–2022)

The Crash and Zimbabwe’s Mining Sector (2023–2025)

Zimbabwean Government Policy Response

Geopolitical Considerations

Recommendations

Conclusion

Benefits of Smart Cross-border Invoicing for B2B Payments

June 10, 2025 by diadem445c3650ff Businesses everywhere are looking beyond their local markets, reaching out to customers and partners across continents. This global ambition brings incredible opportunities, but it also introduces a familiar headache: getting paid. When you’re dealing with clients in different countries, each with their own currency and banking quirks, sending and receiving invoices can feel like navigating a complex maze. The simple act of sending a bill can quickly turn into a frustrating saga of delays, hidden fees, and reconciliation nightmares. But what if there was a way to cut through this complexity? What if you could ensure faster payments, in multiple currencies, without the usual stress? At WeWire, we’re changing that. Our smart cross-border invoicing feature helps global businesses create customizable invoices with embedded payment links—allowing customers to pay in their preferred fiat currency or stablecoin, while the business receives settlement in their own preferred fiat or stablecoin. It’s fast, seamless, and built for the realities of modern commerce. In this blog post, we’ll explore the benefits of smart cross-border invoicing, why it’s a game-changer for B2B payments, and how businesses that delay adopting this innovation could be leaving both time and money on the table. You might think a few extra days or a small percentage fee doesn’t matter much in the grand scheme of things. Think again. The inefficiencies of traditional cross-border payments are silent profit-killers, significantly impacting global businesses. Consider these realities: According to a McKinsey 2023 global payments report, B2B cross-border transactions represent over $150 trillion in value globally—but around $120 billion in associated friction costs are incurred annually due to inefficiencies, lack of transparency, and poor reconciliation. In short: businesses aren’t just spending more; they’re losing money every time they invoice internationally the old-fashioned way. Smart cross-border invoicing automates and simplifies the entire process of requesting and receiving payments across currencies and jurisdictions. With WeWire’s smart invoicing tool, global businesses can: In essence, it removes all guesswork and manual steps from the equation—making the invoicing experience frictionless for both sender and receiver. Traditional wire transfers and SWIFT payments are slow. With smart invoicing via WeWire, businesses can receive payments in minutes or hours, not days. This faster settlement cycle improves cash flow and enables faster reinvestment or restocking. When a buyer pays in their own currency and you get paid in yours—with conversion handled automatically at competitive rates—you avoid the layers of hidden FX spreads and bank charges. Over time, this can save businesses thousands of dollars per transaction cycle. According to a 2024 study by FXC Intelligence, international B2B payment fees range from 2.5% to 6% depending on route and currency. By switching to stablecoin settlement or intelligent routing via platforms like WeWire, businesses can cut this cost by up to 80%. Giving your customers the option to pay using their local currency or preferred stablecoin enhances trust and improves payment completion rates. It shows flexibility, professionalism, and cultural alignment—all of which lead to faster invoice closure and repeat business. Whether you want to receive funds in NGN, CAD, AED, GBP, UGX, EUR, USD, GHS—or stablecoins like USDC or USDT—WeWire gives you that control. This is especially powerful for businesses in emerging markets looking to hold value in USD equivalents or avoid local currency devaluation. WeWire’s smart invoicing tool is especially beneficial for African businesses trading with partners in Europe, the US, Asia, and Latin America. Here are a few scenarios that highlight the benefits of of smart cross-border invoicing: With WeWire: This setup removes traditional barriers, speeds up cash flow, and ensures regulatory-aligned compliance, making African businesses globally competitive. With WeWire, you can: Smart cross-border invoicing often raises questions around KYC, AML, and regulatory alignment. That’s why WeWire is designed with compliance built in. WeWire supports: This means you can scale internationally with confidence—without worrying about grey zones or compliance risks. Cross-border B2B payments don’t need to be slow, costly, or complicated. With WeWire’s smart invoicing tool, businesses can unlock faster settlements, reduce unnecessary fees, and offer a better experience for global clients—all while staying fully compliant. The benefits of smart cross-border invoicing are clear: improved cash flow, streamlined operations, and greater transparency in every transaction. The world is getting smaller. But your margins don’t have to. Ready to modernize your invoicing and take control of cross-border payments? Let’s cross borders together

diadem445c3650ff

The Hidden Costs of Old-School Invoicing: Are You Losing Money?

What Is Smart Cross-Border Invoicing?

Benefits of Smart Cross-Border Invoicing for Global B2B Businesses

Faster Settlements

Reduced FX Losses and Banking Fees

Better Customer Experience

Flexible Settlement Options

Unlocking Global Trade In and Out of Africa

Common scenarios:

Compliance Without Compromise

Final Thoughts

Stablecoin Market Cap Explained: Why It Matters in the Future of Digital Finance

June 10, 2025 by diadem445c3650ff The digital finance landscape is evolving at breakneck speed, and at the heart of this transformation lies the humble yet powerful stablecoin. Few indicators are as telling as the stablecoin market cap. What might seem like just another crypto metric is, in fact, a powerful signal of trust, utility, and financial innovation. More than just a bridge between traditional finance and the volatile world of cryptocurrencies, stablecoins are emerging as a fundamental building block for a more efficient, inclusive, and globally connected financial system. For anyone involved in digital payments, from fintech builders to investors and regulators, understanding the stablecoin market cap isn’t just an academic exercise, it’s a critical barometer of the industry’s health, potential, and direction. At WeWire, we’re constantly analyzing these trends, recognizing the pivotal role stablecoins play in streamlining cross-border payments and unlocking new possibilities for businesses worldwide. A stablecoin is a digital asset pegged to the value of a real-world currency, most commonly the US dollar, euro, or other fiat. Unlike volatile cryptocurrencies like Bitcoin or Ethereum, stablecoins are designed for price stability—making them ideal for payments, remittances, and international settlements. The market capitalization (or market cap) of a stablecoin is the total value of all its tokens in circulation. It’s calculated by multiplying the number of tokens issued by their current price (usually $1 for fiat-pegged coins). Why does this matter? Because the market cap reflects both demand and trust. A rising market cap often signals increased usage, while a declining one may point to regulatory pressure, reduced utility, or waning confidence. As of Q2 2025, the global stablecoin market cap stands at approximately $162 billion, up from $124 billion in early 2024—a sign of steady, renewed interest after the broader crypto cooldown. Here’s a snapshot of major players: Stablecoins saw explosive growth in 2021–2022, with the market peaking near $180 billion in early 2022. However, the collapse of TerraUSD (UST) in May 2022—a $45 billion algorithmic stablecoin that de-pegged—shook investor confidence and prompted a contraction. After a regulatory recalibration in 2023, 2024 and 2025 have ushered in a recovery—especially in emerging markets, where stablecoins are becoming financial lifelines. Increased DeFi activity, enhanced regulatory clarity, and enterprise adoption have all contributed to the rebound. At WeWire, we don’t just observe these market shifts—we build on them. WeWire leverages stablecoins like USDC and USDT to deliver instant, secure, and compliant cross-border payments for businesses across Africa and other emerging markets. By embedding stablecoin infrastructure into our business banking and smart invoicing tools, we make it possible for SMEs, platforms, and exporters to: Stablecoins eliminate the friction that has historically held African businesses back—such as high FX costs, compliance bottlenecks, and settlement lags. WeWire’s platform ensures that businesses aren’t just receiving funds faster—they’re also doing it within a compliant, KYC/AML-ready framework that regulators can trust. This is more than technology. It’s about unlocking new trade corridors, increasing export potential, and making African businesses globally competitive. A growing stablecoin market cap means more value is being stored, transacted, and relied upon outside of traditional banking systems. For regulators, this raises questions about: That’s why frameworks like MiCA in the EU and sandbox regimes in Nigeria, Ghana, and Kenya are shaping how stablecoins are used at scale. At WeWire, we’re aligned with these shifts—building with compliance in mind and engaging with ecosystem partners to ensure our solutions remain regulation-forward. The stablecoin market cap is more than a number. It reflects real-world usage, ecosystem maturity, and the next frontier of global money movement. As fintechs and businesses embrace stablecoins to: …the market cap will continue to grow as a reflection of adoption and institutional trust. At WeWire, we believe Africa shouldn’t just benefit from this shift—we should lead it. Stablecoins are rewiring global finance. Their market cap is a mirror reflecting where trust, innovation, and utility are flowing. For businesses looking to scale across borders, watching this metric isn’t just smart—it’s essential.

diadem445c3650ff

What Is a Stablecoin—and How Does Market Cap Apply?

Key Players and Their Share of the Market

Market Cap Trends: Growth, Crashes, and Recovery

How WeWire Is Using Stablecoins to Power Cross-Border Trade

Regulatory and Monetary Implications of Market Cap Growth

The Road Ahead: How Market Cap Signals the Maturity of Stablecoins

Final Thought

WeWire Secures Mauritius Treasury License to Power Trade Finance Innovation

June 9, 2025 by diadem445c3650ff WeWire has secured a Mauritius Global Treasury Activities License from the Financial Services Commission (FSC), signalling our strategic focus on strengthening its transaction capacity globally. This milestone reinforces WeWire’s vision to serve as a banking and trade bridge for businesses trading between Africa and the world and vice versa. With this new treasury license, WeWire becomes the only African fintech offering fully integrated cross-border payments and trade finance solutions under one platform. This move empowers businesses globally to not only send and receive cross-border payments, but also access working capital and trade finance tools with faster approvals than traditional banks. For businesses in emerging markets, navigating international payment is often complex and burdened by compliance delays, bank rejections, or high-risk labels. WeWire offers a streamlined alternative. The WeWire platform simplifies global transactions by combining regulatory-compliant fiat and stablecoin payment rails with trade finance, enabling faster, more reliable access to global markets. Since launching three years ago, WeWire has processed over $2.2 billion in transactions for 3,000+ businesses across 80+ countries. Headquartered in the UAE with operational headquarters in Ghana, WeWire has expanded its footprints to Nigeria, Kenya, Uganda, the UK, Canada, and Dubai—demonstrating the scalability of its infrastructure and its commitment to supporting global commerce from Africa outward. With the continued challenges businesses face with international payments from lengthy compliance processes to outright denial or account closure due to being wrongfully tagged high risk, WeWire is keen on transforming and simplifying B2B cross-border payments across emerging markets. By replacing costly, inaccessible and fragmented payments systems with off-shore banking services and efficient stablecoin rails, WeWire is placing access to global markets in the hands of the average business owner. Over the past few years, lots of progress has been made in the remittance industry for individuals while hurdles continue to show up for businesses and other high value/volume payments. WeWire understands these problems and has built solutions that address these challenges and make payments faster. With the licenses that WeWire possesses from Canada, Mauritius and the newly coming UK, WeWire would be able to provide banking services that are compliant, cost-effective and understanding of the risks on African markets. Speaking on the new developments, Eben Ghanney, the CEO of WeWire, said, “The world runs on trade. For us at WeWire, we are building solutions that sit at focal points to power seamless trade transactions across multiple currencies. This license takes us a step further in achieving our vision to provide a bridge for global multinational businesses and corporations to trade in and out of Africa easily. We aim to achieve this by providing treasury services, allowing corporations to hedge their FX risk and access trade finance, local currency liquidity lines, and so much more. Raising funds to ensure liquidity means we can focus on growth and identify business opportunities in more sectors”. As WeWire secures Mauritius Treasury License, it signals a significant leap forward for WeWire’s mission: to build a truly borderless, business-first financial ecosystem that connects Africa to the world—and the world to Africa.

diadem445c3650ff

Why Stablecoins Are the Future of Cross-Border Payments for Businesses

June 3, 2025 by diadem445c3650ff When you hear “need for speed,” your mind might jump to fast cars, racing, and all that adrenaline. But business owners need speed too—especially when it comes to global payments. Unfortunately, traditional cross-border transactions are often slow, expensive, and tangled in complex currency conversions. High fees and delayed processing times can choke cash flow and stunt growth. That’s why stablecoins for cross-border payments are gaining traction as a powerful, modern alternative. With the rise of blockchain technology, stablecoins have emerged as a powerful solution for businesses seeking smarter and faster ways to move money across borders. At WeWire, we’re helping businesses tap into the power of stablecoins to simplify global payments, reduce costs, and improve cash flow. Here’s a deep dive into why stablecoins are becoming a game-changer for cross-border payments—and how your business can benefit. Stablecoins are a type of cryptocurrency pegged to the value of a stable asset, such as the US Dollar (USD) or Euro (EUR). Unlike volatile cryptocurrencies like Bitcoin or Ethereum, stablecoins are designed to maintain a stable value, making them ideal for commercial transactions. Two of the most widely used stablecoins are: These digital currencies are available on multiple blockchain networks, enabling businesses to move funds globally with speed and reliability. At WeWire, we provide stablecoin rails that allow businesses to send and receive global payments in USDT and USDC across multiple chains. Whether you’re paying vendors overseas or collecting payments from international clients, our platform ensures the process is smooth, secure, and affordable. With WeWire, businesses can: While the stablecoin ecosystem is growing rapidly, security and compliance remain top priorities. At WeWire, we work with trusted liquidity partners and follow best practices to ensure your funds and data are safe. As regulations evolve, we’re committed to staying compliant and secure, so you can transact with confidence. Stablecoins are not just a passing trend—they’re actively reshaping how businesses move money across borders. With faster settlement times, reduced fees, and broader financial access, stablecoins for cross-border payments offer a compelling alternative to outdated global payment systems.By choosing a partner like WeWire, your business gains access to powerful tools like: Whether you’re expanding into new markets or just looking to streamline your international payments, stablecoins offer the speed, savings, and security your business needs. Join the many businesses already using stablecoins to simplify cross-border payments.

diadem445c3650ff

What Are Stablecoins?

Why Use Stablecoins for Cross-Border Payments?

Traditional international bank transfers can take anywhere from 2–7 business days. With stablecoins, payments can be settled in minutes, regardless of time zones or banking hours.

Sending money internationally through banks or payment providers can come with high fees—sometimes up to 10%. Stablecoin transfers via WeWire’s rails can cut those costs by up to 50%, improving your bottom line.

Stablecoins are pegged to fiat currencies, reducing the risk of price fluctuations during transactions. This makes them more predictable and secure for business use.

Blockchain-based transactions are recorded on public ledgers, offering clear traceability and reducing the chances of fraud or errors.

Businesses in Africa, the Middle East, Asia, and beyond can bypass traditional banking limitations and transact globally with ease.

How WeWire Uses Stablecoin for Cross-border Payments

Who Benefits Most from Stablecoin Payments?

Avoid banking delays and currency volatility by receiving stablecoin payments in real time.

Get paid faster and more affordably across borders without waiting for SWIFT transfers.

Reduce payment costs and access international markets without the overhead of traditional banking.

Enable global users to pay or withdraw in stablecoins, reducing reliance on localized payment rails.

Stablecoins vs. Traditional Cross-Border Transfers

Feature

Traditional Bank Transfers

Stablecoin Payments via WeWire

Transfer Speed

2–7 business days

Minutes

Transaction Fees

3–10%

Up to 50% cheaper

Currency Volatility

Medium to High

Low

Access Requirements

Bank account needed

Wallet or payment link only

Settlement Transparency

Low

High (on-chain)

Security and Regulation

The Future of Global Payments Is Here

Ready to Rewire the Way You Move Money?

Get started with WeWire today.

Cross-Border Invoicing: Get Paid Faster in Multiple Currencies

May 30, 2025 by diadem445c3650ff Businesses everywhere are looking beyond their local markets, reaching out to customers and partners across continents. This global ambition brings incredible opportunities, but it also introduces a familiar headache: getting paid. When you’re dealing with clients in different countries, each with their own currency and banking quirks, sending and receiving invoices can feel like navigating a complex maze. The simple act of sending a bill can quickly turn into a frustrating saga of delays, hidden fees, and reconciliation nightmares. But what if there was a way to cut through this complexity? What if you could ensure faster payments, in multiple currencies, without the usual stress? As a finance expert who’s seen the evolution of digital payments firsthand, I can tell you that the key lies in intelligent, streamlined cross-border invoicing. Let’s dive into how this powerful tool is changing the game for B2B payments. Imagine you are based in Germany and you have just completed a significant project for a client in a Kenya. You send your invoice, anticipating prompt payment. However, the traditional cross-border payment system often kicks off a cascade of inefficiencies: According to a 2023 study by Deloitte, nearly 60% of B2B cross-border payments take more than 3 days to settle, and 22% take over a week. These delays hurt small to medium-sized enterprises (SMEs) the most, tying up working capital and creating cash flow uncertainty. Add fluctuating exchange rates and complex compliance regulations to the mix, and you have a recipe for lost revenue and strained client relationships. Cross-border invoicing refers to the process of generating and sending invoices to clients in other countries—often in a different currency and within a different regulatory environment. It involves: Cross-border invoicing bridges the gap between buyer and seller and accelerates the payment lifecycle.. Many businesses still rely on manual invoicing tools like PDFs, emails, and spreadsheets. While this may work for local transactions, it falls apart at the global level. Here’s why: All of this adds up to a frustrating experience for both the seller and the buyer—and ultimately, a delayed payment. WeWire is changing the game by enabling businesses to create and send cross-border invoices that are easy to pay, fast to settle, and flexible in currency. Whether your client prefers USD, EUR, NGN, GBP, KES, or stablecoins like USDT and USDC, WeWire lets them pay how they want—while you receive funds in your currency of choice. This not only removes barriers for your clients but also ensures liquidity for your business—no more waiting a week for funds to clear. Whether your clients are in Europe, North America, Asia, or Africa, WeWire supports a wide range of fiat and stablecoin currencies, giving them the flexibility to pay how they want. You can invoice in USD and receive in NGN or USDT—whatever works best for your operations. Traditional banking channels can take days to settle. With WeWire’s infrastructure, payments can be completed in real-time or within hours, significantly improving your cash flow. By eliminating intermediaries and using efficient stablecoin rails, WeWire reduces fees typically associated with SWIFT transfers and bank charges. WeWire is licensed in Canada, Mauritius, and soon the UK, ensuring that all transactions are AML and KYC compliant, so you can operate globally with peace of mind. A seamless payment experience for your clients improves your chances of getting paid faster. No logins, no complex forms—just a simple, intuitive payment process. Imagine you run a software development agency in Kenya and you’re working with a US-based e-commerce firm. You send an invoice for $10,000. That’s a faster payment cycle, better margins, and a stronger relationship with your client. As global commerce continues to grow—cross-border B2B e-commerce alone is expected to reach $1.8 trillion by 2027—the businesses that win will be the ones that remove friction from their payment and invoicing processes. Cross-border invoicing is no longer just a finance function. It’s a strategic growth enabler. With tools like WeWire, SMEs and large enterprises alike can: At WeWire, we’re building the future of B2B payments. Our cross-border invoicing tools are designed for businesses that want to scale globally without the typical headaches. Let your clients pay in their currency. Get settled in yours. Quickly. Reliably. Securely. ➡️ Get started with WeWire today and take the hassle out of global payments.

diadem445c3650ff

The Hidden Costs of Traditional Cross-border Payments: Why Speed and Currency Matter

What Is Cross-Border Invoicing?

Why Traditional Invoicing Methods Don’t Work Anymore

Cross-Border Invoicing with WeWire: Get Paid Faster

How It Works:

Benefits of Using WeWire for Cross-Border Invoicing

1. Multi-Currency Support

2. Faster Settlements

3. Lower Costs

4. Automated Compliance

5. Client-Friendly UX

Real-World Example

Cross-Border Invoicing Is No Longer Optional

Ready to Get Paid Faster?

What is Cross-Border Invoicing and How Can It Simplify B2B Payments?

May 30, 2025 by diadem445c3650ff Businesses are scaling fast, and transactions no longer end at national borders. Companies are sourcing goods, services, and talent from across the globe. An exporter in Ghana is trading with a wristwatch maker in China, a freelancer on the coasts of Rwanda is offering services to a big tech founder in Atlanta, USA. As these cross-border relationships become more routine, the need for smooth, transparent, and efficient payment mechanisms becomes critical. One such mechanism that’s quietly transforming global commerce is cross-border invoicing. But what is cross-border invoicing? How does it simplify B2B payments across industries? And why is WeWire positioned as the go-to solution for businesses navigating international financial terrain? Let’s dive in. Cross-border invoicing refers to the process of issuing and managing invoices between businesses located in different countries. Unlike domestic invoicing, this involves dealing with multiple currencies, fluctuating exchange rates, regulatory hurdles, varying tax regimes, and compliance requirements. While that might sound like a logistical nightmare, cross-border invoicing—when done right—actually streamlines global transactions. It ensures that payments are traceable, timely, and compliant with international standards, reducing risk and administrative burdens for both payers and recipients. In essence, it’s the backbone of global B2B commerce. This isn’t your standard domestic transaction. Here’s why it gets complicated: Cross-border payments have historically been slow, expensive, and opaque. Traditional bank transfers often come with high fees, poor exchange rates, and settlement delays that can stretch for days. With WeWire cross-border invoicing, businesses can generate and process invoices for goods or services exchanged between businesses located in different countries, collect payment in the customer’s preferred currency and get settlement in any currency of their choice. Here’s how cross-border invoicing transforms that experience: With cross-border invoicing, businesses can invoice in the buyer’s or seller’s preferred currency. This transparency helps both parties avoid surprises due to fluctuating exchange rates and makes budgeting more predictable. WeWire allows businesses invoice their clients in up to 10 fita currencies (local and international) as well as stablecoins. Invoices can be customized to meet local tax and compliance requirements, ensuring businesses don’t inadvertently breach regulations. For example, VAT/GST details, invoice numbering, and required fields can be automatically adjusted based on region. Modern invoicing systems, like WeWire’s, also use stablecoin payment rails that bypass the delays of traditional banking systems. That means funds are settled faster—sometimes even instantly—giving businesses better cash flow and reducing working capital constraints. Digital invoicing minimizes intermediaries, allowing businesses to avoid the multiple layers of fees that traditional cross-border transactions incur—like correspondent bank charges, SWIFT messaging fees, and exchange markups. Unlike wire transfers that disappear into the void for days, cross-border invoicing solutions offer real-time tracking. Businesses can see when invoices are issued, received, approved, and paid—reducing disputes and delays. Cross-border invoicing isn’t just for massive multinationals. It’s a game-changer across a variety of industries: Whether you’re a platform paying international vendors or a merchant shipping globally, cross-border invoicing helps ensure timely and transparent settlements—fueling trust and scaling operations. With talent now sourced globally, HR teams and agencies need tools to manage payments to remote employees and contractors in multiple countries. Cross-border invoicing ensures prompt, accurate, and compliant compensation. Manufacturers working with overseas suppliers or selling to foreign distributors need invoicing systems that support multi-currency, localized tax compliance, and swift reconciliation. Subscription-based companies serving global clients must handle recurring cross-border invoices. Automation ensures that billing cycles are consistent, and payments flow smoothly across jurisdictions. Companies that manage warehousing, freight forwarding, and customs clearance across borders rely on invoicing systems to unify financial documentation and maintain cash flow consistency. At WeWire, we understand that B2B cross-border payments shouldn’t be a bottleneck—they should be a bridge. That’s why our cross-border invoicing solution is built to empower businesses of all sizes to go global with confidence. Here’s what sets WeWire apart: Whether you’re managing a handful of international invoices or thousands, WeWire handles the complexity—so you don’t have to. Our infrastructure supports high-volume invoicing with zero compromise on speed or accuracy. WeWire enables you to invoice and get paid in over 10 currencies, with built-in currency conversion and competitive FX rates. This allows you to maintain trust with clients and partners worldwide. What truly sets WeWire apart is support for both fiat and stablecoin payments. Whether your partners prefer to transact in NGN, GHS, KES, XAF/XOR USD, EUR, or regulated stablecoins like USDC or USDT, WeWire’s invoicing solution makes it seamless. This dual capability gives businesses more flexibility, faster settlement times, and increased resilience against currency volatility—especially in emerging markets. Each invoice is tracked from issue to payment. Our platform matches payments to invoices automatically, eliminating manual reconciliation and freeing up your finance team for strategic work. Our invoicing solution plugs right into your existing ERP or payment stack—so you don’t need to overhaul your systems. WeWire plays well with the tools you already use. WeWire helps you stay on the right side of global financial regulations with compliant invoicing templates and tax-ready reports for every region. Invoicing is just one piece of the puzzle. WeWire offers an all-in-one platform for global B2B payments, from collections to payouts—delivering full visibility and control across your entire payment lifecycle. Explore it here: WeWire Cross-Border Invoicing Cross-border invoicing is more than just sending a bill across borders—it’s a strategic lever that simplifies operations, accelerates payments, and unlocks global growth. In a world where business is increasingly borderless, the companies that invest in the right financial infrastructure are the ones that scale the fastest. At WeWire, we’re helping forward-thinking businesses do just that—with modern infrastructure, compliance-ready features, and the unique advantage of both fiat and stablecoin payment support. Ready to simplify your international payments? Start invoicing smarter with WeWire.

diadem445c3650ff

Understanding What Cross-Border Invoicing Is

How Cross-Border Invoicing Simplifies B2B Payments

1. Currency Clarity

2. Automated Compliance

3. Faster Settlement Times

4. Reduced Fees

5. Real-Time Tracking

Industries That Benefit from Cross-Border Invoicing

1. E-Commerce & Marketplaces

2. Freelancing & Remote Work

3. Import/Export & Manufacturing

4. Software & SaaS

5. Logistics & Supply Chain

Why WeWire is the Solution of Choice

✔️ Built for Scale

✔️ Multi-Currency Invoicing

✔️ Fiat and Stablecoin Payments

✔️ Automated Reconciliation

✔️ API Integration

✔️ Regulatory Compliance

✔️ Unified Platform

From Paperwork to Global Possibility