How Stablecoins Are Redefining Savings in High-Inflation Economies

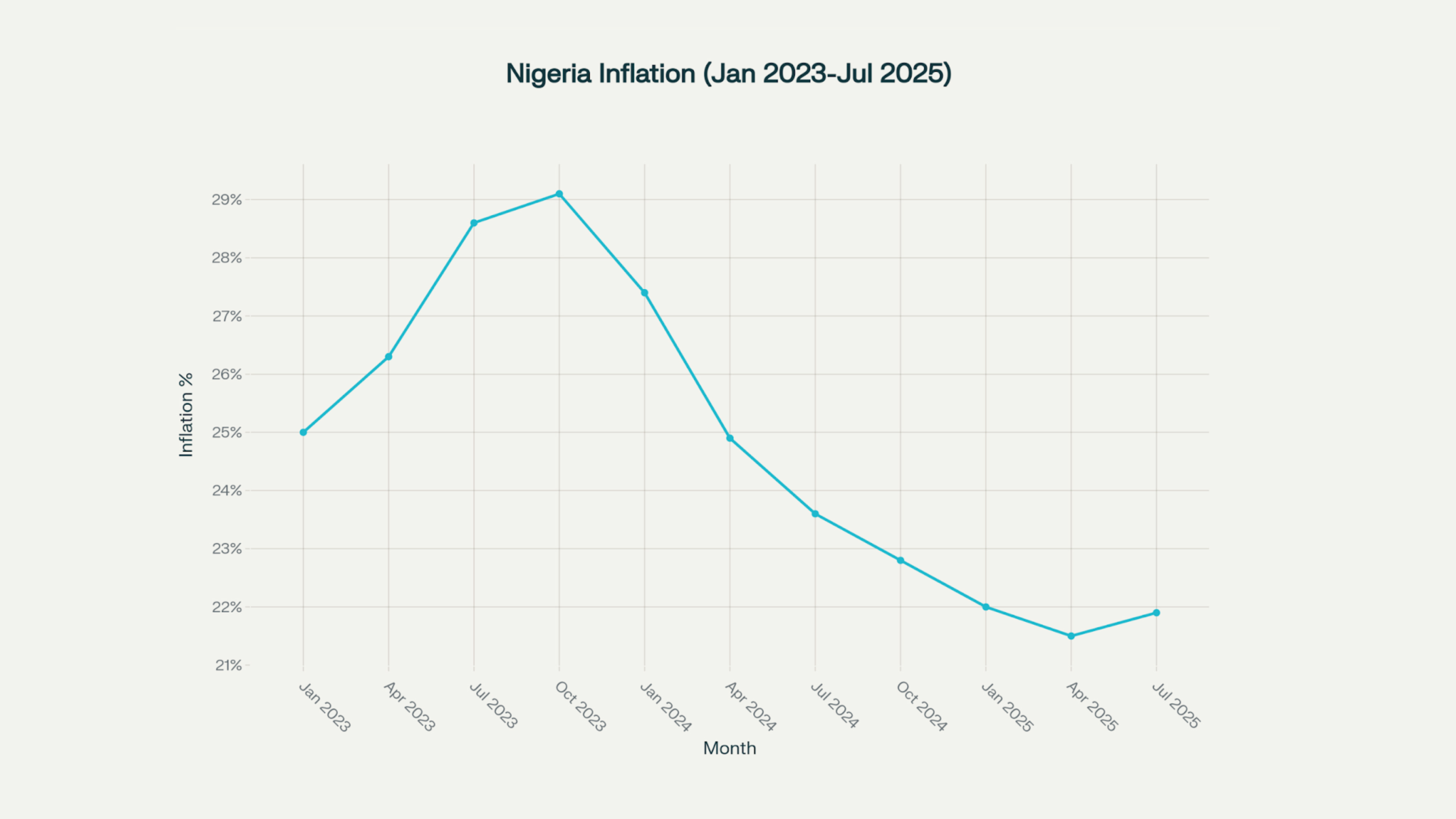

October 8, 2025 by diadem445c3650ff Across many emerging markets, blockchain-based stablecoins like USDT and USDC are supplanting traditional dollar savings. In countries where inflation is rampant and foreign exchange is restricted, people increasingly keep value in tokenized dollars rather than local cash. Stablecoins are crypto tokens pegged 1:1 to the U.S. dollar and backed by reserves, so they effectively act as digital dollar accounts. For example, Nigeria’s inflation ran near 21.9% in mid-2025 – so a Nigerian saver might move funds into USDT to prevent the naira’s erosion. As Morgan Stanley notes, in such environments stablecoins “are often considered a store of value, protecting against local currency depreciation”. In short, USDT provides 24/7 access to dollars through a smartphone, a practical hedge for households and businesses when official dollar accounts are scarce or expensive. In high-inflation economies from Nigeria to Argentina, local currencies are losing value fast. Nigeria’s consumer prices hit 21.9% (year-on-year) in July 2025, and many African currencies have weakened dramatically. Governments often impose strict foreign‐exchange (FX) controls, making legal dollar accounts hard to open. This erodes trust in fiat and pushes savers to alternatives. A recent Chainalysis study finds that Nigeria has received roughly $92.1 billion in crypto inflows over 12 months, nearly three times South Africa’s volume, driven largely by inflation and limited forex access. In this context, crypto analysts and reporters emphasize that stablecoins can “mirror the strength of the U.S. dollar” and fill the vacuum. Data from African crypto platforms confirm the trend. A Yellow Card–sponsored report finds stablecoins now represent about 43% of all crypto trading volume in sub-Saharan Africa, with Nigeria alone accounting for ~$22 billion over a one-year period. Practically every young trader or remittance sender there is increasingly using tokens like USDT instead of withdrawing dollars. Yellow Card itself says 99% of its transactions are in stablecoins (USDT alone is 88.5% of their volume). Roughly 70% of Yellow Card’s users report using these tokens for personal remittances or savings. This data highlights the point: for many people, USDT isn’t speculation – it’s a lifeline. Savers use it as a “digital dollar account” to park money. The technical plumbing behind this shift involves crypto exchanges and mobile‐money interfaces. Africans often buy USDT on P2P networks or fintech apps. For example, global exchanges’ peer-to-peer desks (like Binance P2P) allow users to trade naira or shillings for Tether directly at market rates. Local startups such as Yellow Card, Bitnob or Bundi provide instant rubicon between Tether and mobile wallets or bank accounts. As Cointelegraph reports, some freelancers in Kenya now invoice clients in USDC and receive payouts in M-Pesa within minutes. In Nigeria, reporters note traders maintain working capital in USDT to avoid naira crashes. Chainalysis data back this up: in Nigeria, every transaction under $1 million in one quarter was in stablecoins, totaling about $3 billion. This dollarization trend isn’t limited to Africa. Latin America’s high-inflation economies show similar patterns. Chainalysis notes that four LatAm countries rank among the top 20 globally for grassroots crypto adoption. In Argentina – which saw inflation over 100% – stablecoins dominate local crypto trading. About 61.8% of Argentina’s crypto transaction volume is now in stablecoins (versus ~44.7% global average). Every time the peso fell last year, Argentinians quickly piled into USDT on local exchanges. Venezuela’s population has also fled into crypto (BTC and stablecoins) as the bolívar collapsed; indeed, Venezuelan crypto inflows grew 110% YoY even while the government experimented with its own “petro” token In summary, USDT and its peers have quietly become the new “dollar accounts” for many in high-inflation countries. Instead of speculating, everyday users treat these tokens as simple tools to protect their savings from eroding local currencies. This shift is still a small fraction of the global monetary system – stablecoins today represent a few tenths of a percent of world money supply – but the growth is striking. The total stablecoin market cap jumped from about $5 billion in early 2020 to roughly $300 billion by late 2025, driven in part by usage in emerging markets. Looking forward, stablecoins could become even more mainstream: financial giants and tech firms are racing to integrate them into payments, and a wave of central bank digital currencies (CBDCs) is on the way as governments try to offer an official digital alternative.

diadem445c3650ff

Regulatory Regimes for Stablecoin Payments in Africa & Emerging Markets

October 5, 2025 by diadem445c3650ff The rise of stablecoins is nothing short of a financial revolution, quietly transforming how money moves across borders. For businesses and individuals in Africa and other emerging markets, stablecoins offer a powerful antidote to traditional banking inefficiencies, currency volatility, and high transaction costs. Yet, this promise of faster, cheaper, and more inclusive payments operates within a complex and rapidly evolving legal landscape. Understanding the diverse regulatory regimes for stablecoin payments in Africa & Emerging Markets isn’t just an academic exercise; it’s a critical imperative for any business looking to leverage this technology. At WeWire, we are not merely observers of this evolution; we are active participants, building compliant infrastructure that empowers businesses to navigate these complexities and thrive in the digital economy. Before diving into regulation, it’s crucial to grasp the outsized impact stablecoins have in these regions: For many, stablecoins are not a luxury, but a necessity – a digital dollar that can be accessed and transferred with unprecedented ease. Initially, many emerging markets reacted to cryptocurrencies with outright bans or extreme caution. However, as the utility of stablecoins became undeniable, especially for remittances and trade, regulators began shifting their approach. The trend is clearly moving from restriction towards structured licensing, sandbox regimes, and comprehensive legal frameworks. Let’s compare how different regions are approaching this: Africa is a hotbed of crypto adoption, driven by clear use cases. Regulators are now trying to catch up with the pace of innovation. Once known for its strict crypto ban, Nigeria has significantly evolved. The Securities & Exchange Commission (SEC) now classifies cryptocurrencies as securities, providing a framework for oversight. Crucially, the Central Bank has allowed banks to service exchanges and stablecoin platforms, reversing previous restrictions. Imagine a Nigerian tech startup, “NaijaConnect,” sourcing components from China. Before, they battled FX shortages and long bank transfer delays. Now, with regulated stablecoin access, they can quickly convert Naira to a USD-pegged stablecoin, pay their supplier instantly, and hedge against Naira depreciation. This shift from a blanket ban to supervised sandboxes like ARIP demonstrates a pragmatic approach. Kenya is proposing its first comprehensive crypto bill. This legislation will require crypto businesses to be licensed and will introduce robust AML/KYC rules. The Central Bank of Kenya (CBK) and Capital Markets Authority (CMA) will share oversight, aiming for a coordinated approach. This move provides much-needed legal clarity for fintechs operating in Kenya, encouraging investment and innovation within a regulated environment. Ghana is poised to roll out a new regulatory framework led by the Bank of Ghana (BoG). The new law aims to license Virtual Asset Service Providers (VASPs), providing legal clarity and helping to formalize the country’s $3 billion crypto market. For a Ghanaian remittance company, this means moving out of the regulatory grey area, gaining legitimacy, and leveraging stablecoins to offer even cheaper and faster services to the Ghanaian diaspora. South Africa has formally classified crypto assets as financial products, bringing them under the oversight of the Financial Sector Conduct Authority (FSCA). This means strict licensing requirements for crypto service providers. It is also actively building specific rules for cross-border transactions involving digital assets. The result is a clear, if stringent, path for businesses to operate, focusing on consumer protection and financial stability. Regardless of the specific jurisdiction, several core compliance requirements are becoming universal for stablecoin issuers and service providers: For businesses looking to harness stablecoins for payments, navigating these varied and complex regulatory environments is no small feat. It requires: We designed an eBook “The Business Guide to Stablecoins – Unlocking Cost-Effective Cross-Border Payments” which reveals how this new wave of digital money is helping exporters, importers, and SMEs streamline transactions, cut costs, and expand globally without the traditional banking bottlenecks. Get a copy now At WeWire, we don’t just facilitate stablecoin payments; we provide a fully compliant and licensed bridge for businesses operating in and out of Africa and other emerging markets. Our understanding of the complex regulatory regimes for stablecoin payments in Africa & Emerging Markets is built into the very fabric of our operations. The future of global payments is undoubtedly digital and stablecoin-powered. As regulatory clarity grows, the opportunities for businesses in Africa and emerging markets will only expand. By partnering with a compliant and forward-thinking provider like WeWire, you ensure your business can seize these opportunities with trust, efficiency, and full peace of mind.

diadem445c3650ff

Why Stablecoins Matter So Much in Emerging Markets

The Evolving Regulatory Landscape: From Bans to Frameworks

Africa: Shifting from Caution to Controlled Innovation

Beyond Africa: fast-maturing “reference” regimes

MAS has a final regime for single-currency stablecoins (SCS) pegged to SGD/G10 and issued in Singapore. Core requirements include high-quality reserves, 1:1 redemption at par, timely redemption windows, composition and valuation rules for backing assets, plus disclosure and audit. It’s a gold-standard template for prudentially sound payment tokens.

In May–July 2025, Hong Kong passed a stablecoin bill and published the licensing regime for fiat-referenced stablecoin (FRS) issuers, effective 1 August 2025. Rules cover reserve management, redemption, AML/CFT, custody, and transitional provisions. Expect bank-led and fintech issuers to seek licenses quickly.

Dubai’s VARA issued a comprehensive Virtual Assets and Related Activities Regulations (2023) with dedicated Issuance Rulebooks, including Fiat-Referenced Virtual Assets (FRVAs)—VARA’s term for stablecoins. It sets licensing, prudential, conduct, and AML/CFT expectations and clarifies overlaps with federal regulators.

Brazil’s Virtual Assets Law (14,478/2022) and 2023 decree empower the Central Bank (BCB) to regulate and supervise VASPs. Public consultations continue to refine custody, transfer, and stablecoin obligations—an important anchor for the region’s largest economy.

The BSP approved a peso-pegged PHPC pilot in 2024, and in 2025 the issuer exited the sandbox, enabling broader issuance and payments at scale under oversight. For remittance-heavy corridors, this is a pragmatic, risk-controlled path to real-economy adoption.Key Compliance Requirements: The Universal Language of Trust

Navigating the Landscape: A Strategic Imperative for Businesses

A practical playbook for businesses

WeWire: Your Compliant Partner in the Digital Frontier

The Business Guide to Stablecoins – Unlocking Cost-Effective Cross-Border Payments

September 24, 2025 by diadem445c3650ff Global trade is booming, but the financial rails powering it often feel stuck in the past. For many small and medium-sized enterprises (SMEs), the reality of moving money across borders means high fees, days-long settlement times, and unpredictable exchange rates. That’s where stablecoins are stepping in to rewrite the rules of international commerce. This latest eBook from WeWire “The Business Guide to Stablecoins – Unlocking Cost-Effective Cross-Border Payments” reveals how this new wave of digital money is helping exporters, importers, and SMEs streamline transactions, cut costs, and expand globally without the traditional banking bottlenecks. Unlike volatile cryptocurrencies, stablecoins are pegged to fiat currencies like the US dollar, offering the best of both worlds—blockchain speed and transparency, with fiat stability. For businesses, this means: The eBook highlights compelling case studies where stablecoins transformed payments: These aren’t future projections—they’re happening now. Far from being a gray area, stablecoins are now gaining regulatory clarity. Frameworks like the EU’s MiCA and the U.S. GENIUS Act are setting standards for full reserve backing, audits, and compliance. This ensures businesses can transact with confidence while meeting AML/KYC requirements. The guide walks businesses through practical steps: For SMEs, exporters, and importers, stablecoins are more than just a trend—they’re a competitive advantage. Whether paying overseas suppliers, managing treasury operations, or receiving cross-border revenue, stablecoins offer speed, transparency, and savings that traditional systems simply can’t match. If your business depends on global trade, the time to explore stablecoin business payments is now. Download the full eBook: The Business Guide to Stablecoins – Unlocking Cost-Effective Cross-Border Payments and learn how to future-proof your cross-border operations.

diadem445c3650ff

Why Stablecoins Matter for Businesses

Real-World Impact: From Exporters to Freelancers

The Regulatory Landscape

How SMEs Can Get Started

The Bottom Line

How Stablecoin Rails Empower Businesses to Scale Across Borders

September 19, 2025 by diadem445c3650ff The engine of the global economy runs on trade. From the bustling ports of Jebel Ali in the UAE to the manufacturing hubs of Southeast Asia and the tech corridors of Africa, businesses are more interconnected than ever. Global cross-border payments are projected to soar from $194.6 trillion in 2024 to a staggering $320 trillion by 2032, a testament to this relentless expansion. However, for businesses in emerging markets, this hyper-connected world comes with a significant and often invisible roadblock: the traditional cross-border payment system. Relying on outdated correspondent banking networks, this system is a labyrinth of slow settlements, exorbitant fees, and opaque processes. It is a friction that stifles growth, drains cash flow, and makes global scaling an unnecessarily complex and risky endeavor. This is where the paradigm shift begins. A new financial superhighway, built on the rails of stablecoins, is emerging to solve these decades-old challenges. By combining the speed and transparency of blockchain with the stability of fiat currencies, stablecoins offer a revolutionary solution for businesses seeking to transact globally. As the world moves towards a more efficient and inclusive financial future, WeWire is at the forefront of this transformation, providing the essential infrastructure that empowers businesses to not just participate in, but to dominate the global marketplace. To appreciate the transformative power of stablecoin rails, one must first understand the deep-seated issues that plague traditional cross-border payments. For businesses in the UAE, Nigeria, Kenya, and other emerging markets, these are not mere inconveniences—they are core operational challenges. The UAE is positioning itself as a global hub for digital assets, with notable regulatory clarity across the Central Bank (CBUAE), Dubai’s VARA, and the DFSA (DIFC). In June 2024, the CBUAE approved a framework for licensing and overseeing stablecoins; on the same day DFSA amended its Crypto Token regime, tightening recognition requirements for fiat-backed tokens—clear signals of institutional maturity. VARA’s rulebooks further define activities and licensing, helping providers and enterprises operate predictably. Market momentum is real. Even large issuers are exploring AED-pegged stablecoins, reflecting regional trade demand and the UAE’s role as a payment and logistics hub (pending regulatory approvals). For firms operating across MENA, Africa, South/Southeast Asia, and Eastern Europe, this combination—modern rails + clear rules—creates a springboard for faster expansion. Stablecoins are a class of cryptocurrencies designed to minimize price volatility by pegging their value to a stable asset, typically a fiat currency like the US dollar. Unlike volatile assets like Bitcoin, stablecoins blend the stability of traditional money with the foundational benefits of blockchain technology. The stablecoin market has grown exponentially, with a market capitalization of over $271 billion as of 2025, and is projected to grow at a compound annual growth rate (CAGR) of 54.5% through 2030, according to Grand View Research. The core benefits of stablecoin rails for businesses are transformative: Finance & financial services Technology & SaaS Manufacturing & import/export Emerging-market distributors While the promise of stablecoins is immense, their practical application requires a robust, compliant, and user-friendly platform. This is the gap that WeWire was purpose-built to bridge. As a B2B cross-border payment provider, WeWire’s mission is to empower businesses in emerging markets by providing an all-in-one solution that leverages the power of stablecoin rails. WeWire is not just an observer of this change; it is an active participant, providing a comprehensive suite of tools designed for businesses in finance, tech, manufacturing, and import/export. With operational hubs in the UK, US, Canada, Dubai, Nigeria, Ghana, and Kenya, WeWire has a deep understanding of the unique challenges faced by businesses in these regions. It offers a lifeline for companies seeking to pay international suppliers, manage global treasury operations, or simply unlock new growth opportunities. The traditional cross-border payment system, with its high costs, slow speeds, and lack of transparency, is a relic of the past. For businesses in the UAE and other emerging markets, it represents a significant barrier to global competitiveness. The future of global commerce is borderless, instant, and efficient—and it is built on stablecoin rails. By embracing this new technology, businesses can cut costs, accelerate cash flow, and simplify their international operations. WeWire is the partner of choice for this journey. By providing a comprehensive, compliant, and user-friendly platform, WeWire is not just enabling a new payment method; it is forging the future of global trade. The time has come for businesses to move beyond the limitations of legacy systems and unlock their full global potential.

diadem445c3650ff

Introduction: The Global Commerce Crossroads

The Pain Points of Cross-Border Payments in Emerging Markets

Why this matters in the UAE and other emerging markets

Stablecoins: The New Financial Superhighway

Sector-specific use cases

WeWire: Pioneering the Future of Cross-Border Payments with Stablecoin Rails

Conclusion: The Path to Global Scale

How to Get Paid Online from the US and UK While Running a Business in the UAE

September 9, 2025 by diadem445c3650ff If you run a UAE-based business, chances are your customers aren’t all in one time zone. The US and UK remain two of the most attractive markets for B2B services, e-commerce, SaaS, and creators—yet getting paid across borders can still feel like a maze of fees, delays, and acronyms. The good news: with the right account setup and payment rails, you can make getting paid from these markets nearly as simple as a domestic transfer. This guide distills the essentials—what to set up, how to choose rails (ACH, SEPA, Faster Payments, wires), key compliance considerations, and how a modern provider like WeWire makes it straightforward with USD, GBP, and EUR virtual accounts designed for cross-border commerce. SMEs are the backbone of the UAE economy, contributing ~63.5% of non-oil GDP and numbering over 557,000 companies. As these firms expand online, efficient global collection becomes a strategic advantage, not just an operational task. At the same time, the cost and speed of cross-border payments are in flux. Globally, the average cost of sending remittances was reported at ~6.5%, with digital channels averaging ~4.85% in Q1 2025—a reminder that moving money across borders still carries friction and that choosing the right channel can materially reduce costs. In parallel, SMEs are adopting non-bank fintechs for cross-border more than for domestic payments; in the UK, 23% of SMEs regularly use fintech providers for international payments—a sign that businesses are prioritizing better UX, speed, and fees. The policy environment is also pushing in your favor. Global standard setters have set explicit targets to make cross-border payments cheaper, faster, more transparent, and more accessible, and are tracking measurable progress, particularly on speed and transparency. To make it easy for US and UK customers to pay you, give them local coordinates—the account and routing details they already know and trust—rather than asking them to initiate an international wire every time. Bottom line: If you can collect locally—ACH in the US, Faster Payments/Bacs/CHAPS in the UK, SEPA in the EU—you reduce friction for your buyer and typically lower your acquisition and settlement costs versus international wires. Remember that digital channels materially reduce average costs compared with non-digital methods—one reason more SMEs are shifting to modern providers. Two macro trends are worth watching: WeWire Virtual Accounts are built for UAE businesses that sell globally and want local payment details without opening foreign bank accounts. With WeWire you can: This approach dovetails with what the data already shows: SMEs are increasingly choosing specialized providers for cross-border because speed, transparency, and cost control are genuine differentiators—not “nice to haves.” Getting paid from the US and UK while operating in the UAE no longer requires juggling multiple bank relationships or resigning yourself to slow, expensive wires. By pairing local virtual accounts with the right rails for each job, you can shorten your cash-conversion cycle, lower costs, and give customers a frictionless way to pay. Ready to simplify global collections? Set up WeWire Virtual Accounts for USD, GBP, and EUR, and start getting paid like a local—wherever your customers are.

diadem445c3650ff

Why this matters now

The building blocks: local details for US & UK payers

The most common low-cost rail is ACH (Automated Clearing House). Standard ACH credits typically settle next-day (or later), while Same Day ACH supports same-day settlement within published Fed windows; availability depends on the originator’s bank and cut-offs. Card networks and wire (Fedwire) exist, but ACH is usually the lowest cost for account-to-account B2B payments.

For domestic GBP, Faster Payments supports near-instant account-to-account transfers for most retail and many business transactions; Bacs handles bulk, lower-value direct credits (typically 3 working days), while CHAPS is the high-value, real-time gross settlement rail used for large and time-critical transfers.

If you also sell into the EU, SEPA credit transfers provide low-cost EUR transfers across 36 countries. For cross-border beyond SEPA, SWIFT is the messaging network coordinating bank-to-bank payments and remains the default for many corridors (with variable fees and FX). Step-by-step: setting up to get paid

Virtual accounts give you local account numbers in key markets without opening a full foreign entity bank account. Your US client can pay you via ACH to a US account/routing number; your UK client can pay via Faster Payments to a GB sort code/account number. This “local-to-local” feel is what improves conversion and payment speed.

Invoicing US clients in USD and UK clients in GBP removes the cognitive load of FX for them and reduces disputes. Hold balances in those currencies to time FX conversions strategically.

Expect verification on your business, UBOs, and activity. Choosing a provider with streamlined onboarding reduces time-to-first-payment. (Global bodies are also nudging providers to simplify while maintaining standards.)

Use virtual account sub-accounts or payment references to auto-match inbound credits to invoices. Feed this into your ERP/accounting so your team isn’t chasing spreadsheets.

Convert when rates are favorable and avoid double conversions. Where possible, collect and hold in USD/GBP and do a single conversion when you need AED or another currency. Choosing rails: a quick decision framework

UK: Faster Payments or CHAPS (if large value). US: Same Day ACH or wire (Fedwire) if the amount justifies the cost.

ACH (US), Bacs/Faster Payments (UK), SEPA (EU). These are typically cheaper than card acceptance or international wires for B2B.

Use SWIFT (variable speed/cost). For many corridors, fintech providers can route intelligently to reduce hops and charges. A note on market momentum

Where WeWire fits

Putting it all together: a practical playbook

Final thought

How to Open a US Bank Account from the UAE (No LLC or EIN Needed)

September 6, 2025 by diadem445c3650ff Expanding your business internationally is exciting, but one of the biggest hurdles entrepreneurs in the UAE face is accessing US banking infrastructure. Traditionally, opening a US business bank account requires a ton of paperwork, including setting up an LLC, securing an EIN, and navigating a maze of compliance hurdles. The good news? That’s no longer the only way. Today, fintech platforms like WeWire make it possible for UAE and other emerging market-based companies to open a US bank account without an LLC, EIN, or foreign company registration—all with your local documents. This guide walks you through how it works, why it matters, and what steps you can take to start accepting US payments within hours. For decades, US banks have operated under rigid frameworks, requiring foreign businesses to register as US entities before granting access to accounts. This created barriers for freelancers, startups, and SMEs in regions like the UAE and Africa. But with the rise of cross-border fintech solutions, businesses can now: This shift is driven by technology and partnerships that bridge global payments networks, allowing you to run your business globally, without borders slowing you down. Opening a US bank account via a modern fintech provider like WeWire gives you more than just an account number. Here’s what you gain: For businesses in the UAE, this levels the playing field with US competitors. Here’s how you can get started—no LLC, no EIN required: The ability to open a US bank account from the UAE without forming a US entity is more than just a convenience—it’s a strategic advantage for industries that rely on speed, trust, and seamless cross-border operations. In short, this innovation removes friction from global commerce. It ensures that businesses in emerging markets like the UAE aren’t left behind in the global economy. Q: Do I need an LLC or EIN to open a US account from the UAE? Q: How long does account approval take? Q: Can I receive payments directly from US clients or partners? Q: How do settlements to my UAE bank work? Borders no longer need to slow your business down. With solutions like WeWire, you can open a US bank account from the UAE—without an LLC or EIN—and start receiving payments from clients in the US, UK, and Europe within 24 hours. The global payments system is finally catching up to the speed of business. The only question is: are you ready to take advantage of it?

diadem445c3650ff

Table of Contents

Why You Don’t Need an LLC or EIN Anymore

Why you need a US Account from the UAE

How to Open a US Bank Account with WeWire (Step-by-Step)

Why This Matters for UAE Businesses

Common Misconceptions

Truth: With fintech platforms like WeWire, local UAE documents are enough.

Truth: Digital onboarding allows same-day approval.

Truth: Fintech rails and stablecoin options mean instant or near-instant transfersFAQ

A: No. With WeWire, you can open a US account using only your UAE business documents. Whether you’re in manufacturing, import/export, fintech, or supply chain, the process is the same.

A: Businesses are approved within 2-3 business days, depending on the availability of verified documents. For industries like fintech and supply chain, where transaction speed is critical, this means you can start moving funds almost immediately.

A: Yes. For instance, manufacturing and import/export firms can collect USD payments from distributors or suppliers. Fintech and finance companies can settle customer transactions in real-time, and supply chain companies can pay or receive funds from logistics partners directly.

A: Funds from your US account can be transferred to your UAE bank the same day.Final Thoughts

How Virtual Bank Accounts Slash Costs on Cross-Border Transactions

July 28, 2025 by diadem445c3650ff For manufacturers in Accra, exporters in Mumbai, and financial institutions across Lagos, the global marketplace beckons with immense opportunity. Yet, the traditional mechanisms for cross-border payments often feel like a relic, riddled with inefficiencies that eat into profits and stifle international ambitions. High fees, snail-paced settlements, and the sheer complexity of maintaining multiple physical bank accounts in different jurisdictions are persistent pain points. What if your business could operate globally with the financial agility of a local enterprise? What if you could receive payments from customers in London, New York, or Berlin as easily and cost-effectively as if they were next door? This isn’t a distant dream; it’s the reality offered by virtual bank accounts, and at WeWire, we’re empowering businesses in emerging markets to unlock this transformative power. This blog post dives into what virtual bank accounts are, how they work, why they matter, and why businesses across Africa, Asia, and Latin America are increasingly adopting them. Let’s dissect the common frustrations that plague businesses dealing with international payments: These challenges are particularly acute for businesses in emerging markets, where local financial infrastructure might be less developed, and access to global banking networks can be limited. Virtual bank accounts are not physical bank accounts in the traditional sense. Instead, they are digital sub-accounts linked to a main “master” account. They come with unique local account details (like USD account numbers and routing codes, GBP sort codes and account numbers, or EUR IBANs) that allow businesses to receive and send payments as if they had a local presence in that region. Key characteristics: The most significant benefit of a virtual bank account is the ability to receive local payments in major currencies. Instead of incurring expensive international wire transfer fees, your customers can pay into a local account in their currency (e.g., USD via ACH/Fedwire, GBP via Faster Payments/BACS, EUR via SEPA). This drastically reduces transaction costs for both you and your payers. Payments into virtual accounts often settle much faster than traditional cross-border wires. For instance, ACH and SEPA payments typically clear within 1-2 business days, while Fedwire transfers are often same-day. This accelerated settlement translates directly to improved cash flow for your business, enabling quicker reinvestment and greater financial agility. Many virtual bank account providers like WeWire offer the ability to generate unique virtual account numbers for different payers or purposes. Imagine assigning a specific GBP virtual account to each major customer in the UK, or a unique USD virtual account for each product line. This level of granularity makes reconciliation automatic and effortless, eliminating manual matching and reducing errors. You get a clear, real-time overview of who paid what and when. For businesses in emerging markets that struggle to open physical bank accounts abroad due to stringent requirements, virtual accounts offer an invaluable alternative. They provide the functionality of a local bank account without the burdensome setup process, enabling market entry and global expansion that might otherwise be impossible. While a virtual bank account primarily helps with receiving funds locally, when paired with a multi-currency wallet (which WeWire provides!), you can hold foreign currency funds without immediate conversion. This allows you to convert to your local currency when exchange rates are most favorable, mitigating the impact of FX volatility. Receive payments in foreign currency without costly delays. Manage working capital better and negotiate better payment terms with buyers. Collect payments across geographies while keeping funds in currency until ready to convert. Use virtual bank accounts to hold and distribute foreign currency at scale, increasing payout speed and reducing treasury friction. Streamline cross-border settlement and disbursements using a unified account structure. At WeWire, we are acutely aware of the challenges businesses in emerging markets face in connecting with the global economy. That’s why we’ve built a robust platform that empowers you with the very best in virtual bank account solutions. With WeWire, you can access: The global economy is shifting. Businesses in emerging markets are no longer waiting for traditional banks to catch up. They are leapfrogging outdated systems by adopting flexible, modern payment solutions like Virtual Bank Accounts. With WeWire, your business can transact globally as if you were local—collecting, holding, and sending foreign currency without the old-world overhead. Ready to streamline your cross-border payments?

diadem445c3650ff

Real Problems Businesses in Emerging Markets Face With Traditional Cross-Border Payment

What Are Virtual Bank Accounts?

How virtual bank accounts are revolutionizing cross-border transactions and saving businesses money

1. Local Presence, Global Reach, Lower Costs

2. Accelerate Cash Flow and Boost Liquidity

3. Simplified Reconciliation and Enhanced Transparency

4. Bypass Traditional Banking Hurdles

5. Reduced FX Risk (When Combined with Multi-Currency Wallets)

Who Benefits Most from Virtual Bank Accounts?

Exporters and Manufacturers

Freight Forwarders and Logistics Firms

Fintechs and Remittance Providers

B2B Marketplaces and Aggregators

WeWire: Your Trusted Partner for Global Payments

Create your WeWire account today and unlock your USD, EUR, and GBP virtual bank accounts in minutes.

Why Your Business Should Care About Stablecoins

July 24, 2025 by diadem445c3650ff For businesses operating in emerging markets – from manufacturers sourcing raw materials globally to exporters sending goods across continents, and the financial institutions enabling their trade – the challenges of international payments are all too familiar. High fees, agonizingly slow settlement times, opaque exchange rates, and a maze of regulatory hurdles often chip away at profits and stifle growth. But what if there was a better way? A way to transcend these traditional barriers, offering speed, transparency, and cost-efficiency previously unimaginable? Enter stablecoins, and at WeWire, we believe they are not just a trend, but the future of global commerce, especially for businesses like yours. Let’s face it: the current landscape for cross-border payments is a relic of a bygone era. Imagine a manufacturer in Lagos needing to pay a supplier in Shenzhen. The process often involves: These aren’t just inconveniences; they are significant obstacles to competitiveness and expansion for businesses in dynamic, growth-oriented markets. Stablecoins are a type of cryptocurrency designed to minimize price volatility by being pegged to a stable asset, typically a fiat currency like the U.S. dollar, a commodity like gold, or a basket of currencies. This stability, combined with the underlying blockchain technology, unlocks a revolutionary approach to payments. The most well-known are: Unlike cryptocurrencies such as Bitcoin or Ethereum, stablecoins aren’t designed for speculative investment. Instead, they function as efficient, programmable money with three core advantages: Unlike traditional bank wires that can take days, stablecoin transactions settle in minutes, sometimes even seconds. This is because they bypass the complex web of intermediary banks and operate on blockchain networks that run 24/7, 365 days a year. By eliminating multiple intermediaries, stablecoins significantly cut down on transaction fees and hidden costs. Businesses are reporting savings of over 60% on international payment costs after implementing stablecoin systems. This isn’t just a marginal improvement; it’s a fundamental shift that directly impacts your bottom line. Every stablecoin transaction is recorded on a public blockchain ledger, creating a transparent and immutable audit trail. This end-to-end visibility provides clarity on payment status, fees, and exchange rates, simplifying reconciliation and fostering greater trust between trading partners. For businesses in emerging markets often battling local currency depreciation and inflation, dollar-pegged stablecoins offer a powerful hedge. You can receive or hold value in a stable asset, protecting your capital from the erosion of local currency volatility. This is particularly crucial for maintaining consistent profit margins and predictable financial planning. Stablecoins offer a pathway to the global economy for businesses, especially SMEs, in regions with limited traditional banking infrastructure. With just an internet connection and a digital wallet, they can participate in international trade, opening up new markets and opportunities that were previously out of reach. At WeWire, we understand the unique challenges and immense potential of businesses in emerging markets. We are at the forefront of this financial revolution, offering robust and compliant stablecoin payment solutions tailored to your specific needs. WeWire empowers manufacturers, exporters, and financial institutions to leverage stablecoin rails for international payments, providing: The adoption of stablecoins is accelerating at an unprecedented pace. In 2024 alone, stablecoin transfer volume surpassed the combined throughput of Visa and Mastercard, reaching an astounding $27.6 trillion. Major financial institutions are no longer watching from the sidelines; they are actively integrating stablecoins into their services, recognizing their transformative power. For businesses in emerging markets, this isn’t just about catching up; it’s about leapfrogging traditional limitations and seizing a competitive advantage. Stablecoins are poised to reshape international trade and finance, making global commerce faster, cheaper, and more accessible than ever before. Don’t let outdated payment systems hold your business back. Embrace the future of payments with WeWire and unlock a world of possibilities for your manufacturing, export, or financial institution. Contact WeWire today to explore how stablecoins can revolutionize your international payments.

diadem445c3650ff

The Problem with the Status Quo

Understanding Stablecoins: The New Settlement Layer

Why your business should be paying attention to Stablecoins

1. Unparalleled Speed and 24/7 Availability

2. Drastically Reduced Costs

3. Enhanced Transparency and Traceability

4. Price Stability in Volatile Markets

5. Greater Accessibility and Financial Inclusion

WeWire: Your Partner in the Stablecoin Revolution

The Future is Stable: Are You Ready?

Stablecoins & Financial Transformation in Africa and Beyond

June 26, 2025 by diadem445c3650ff The world of digital assets often conjures images of volatile cryptocurrencies, driven by speculative trading and dramatic price swings. Yet, beneath this dynamic surface, a quieter, more profound revolution is taking place—one of stablecoins financial transformation. Powered by stablecoins, these digital assets, designed for stability rather than rapid appreciation, are rapidly becoming the bedrock of modern digital finance, especially in regions like Africa where financial innovation is paramount. At WeWire, we are deeply invested in understanding and building the infrastructure that harnesses this power. We recognize that for businesses, fintechs, and individuals worldwide, stablecoins are not merely a digital novelty; they are essential tools for efficient, inclusive, and cost-effective financial operations. This exploration delves into the mechanics of stablecoins, their global impact, and why they are proving to be truly transformative, particularly across the African continent. Stablecoins are digital assets pegged to stable reserves, such as fiat currencies like the US dollar or commodities like gold. At their core, stablecoins are cryptocurrencies engineered to maintain a stable value. Unlike Bitcoin or Ethereum, whose prices fluctuate based on market demand and supply, stablecoins are pegged to a “stable” asset. The most common peg is a fiat currency, predominantly the U.S. dollar, but they can also be linked to other national currencies, baskets of currencies, or even commodities like gold. This pegging mechanism is crucial: The primary objective of a stablecoin is to serve as a reliable medium of exchange. They blend the benefits of blockchain (speed, transparency, decentralization) with the predictability of traditional currencies, making them ideal for everyday transactions, cross-border payments, and preserving value in volatile economic environments. The stablecoin market has witnessed explosive growth, reflecting their increasing utility. As of early June 2025, the collective market capitalization of stablecoins in circulation stands at over $250 billion, with approximately 99% pegged to the U.S. dollar (Brookings Institution). This immense market size underscores their role as a critical liquidity provider and a stable base currency within the broader digital asset ecosystem. Key Trends and Data: Dominant Players: Tether (USDT) and USD Coin (USDC) continue to dominate the market. As of early June 2025, Tether’s market cap hovers around $155.22 billion, while USDC stands at $61.00 billion (Kraken). Their continued leadership highlights trust and deep integration across digital finance platforms. The global financial ecosystem has witnessed a remarkable uptick in stablecoin utilization, driving what can be called a stablecoins digital transformation. According to the Cambridge Centre for Alternative Finance (CCAF), the aggregate supply of stablecoins has seen significant growth since 2020, driven by increasing demand for decentralized finance (DeFi) applications and the creation of new stablecoin variants. This surge is not confined to any single region. Emerging markets, in particular, are embracing stablecoins to circumvent traditional banking limitations, facilitate cross-border transactions, and hedge against local currency depreciation. While stablecoins are gaining traction globally, their impact on the African continent is particularly profound, often serving as a critical financial lifeline amidst unique economic challenges. African nations are not adopting stablecoins for mere speculation; they are embracing them out of necessity, seeking solutions to persistent issues with traditional finance. Key Dynamics and Statistics in Africa: Financial Inclusion: Stablecoins offer a pathway to financial services for Africa’s large unbanked and underbanked populations. With just a smartphone and a crypto wallet, individuals can access dollar-pegged assets, send and receive payments, and hedge against local currency depreciation, without needing traditional bank accounts. Stablecoins are being utilized across various sectors in Africa: Despite the promising prospects, stablecoin adoption in Africa faces challenges: However, efforts are underway to address these issues. For instance, the Africa Stablecoin Consortium (ASC) is working to integrate stablecoin technology with traditional financial systems, collaborating with regulators to drive adoption and ensure compliance. The trajectory of stablecoin adoption in Africa indicates a transformative shift in the continent’s financial landscape. As technological infrastructure improves and regulatory frameworks become clearer, stablecoins are poised to play an even more significant role in promoting financial inclusion, economic stability, and cross-border commerce. For stakeholders in the financial sector, understanding and engaging with the stablecoin ecosystem is no longer optional but essential. As Africa continues to lead in innovative financial solutions, stablecoins will undoubtedly be at the forefront of this evolution. At WeWire, we are not just observers of this exciting evolution; we are active participants, providing best-in-class solutions that empower businesses to leverage stablecoins today. We are driving the charge for stablecoins financial transformation with our robust infrastructure is designed to bridge the gap between traditional finance and the digital asset world, offering seamless integration for various business needs: Stablecoins are more than a trend; they are a fundamental shift in how value moves in the digital age. They offer unparalleled efficiency, cost-effectiveness, and accessibility, particularly for the vibrant and dynamic economies of Africa. As the momentum behind stablecoins financial transformation accelerates, more businesses are recognizing their immense potential. WeWire stands ready to provide the cutting-edge solutions necessary to thrive in this new era of digital finance, enabling organizations to harness the full power of stablecoins for real-world impact.

diadem445c3650ff

Understanding Stablecoins & Financial Transformation

Global Surge in Stablecoin Adoption

Stablecoins in Africa: An Economic Lifeline

Use Cases Driving Adoption

Challenges and Regulatory Landscape

The Road Ahead

WeWire: Enabling a Stable Digital Future

Smart Invoicing vs Manual Invoicing: What’s Costing Your Business Time and Money?

June 20, 2025 by diadem445c3650ff Every business, no matter its size or industry, relies on invoicing to get paid. It’s the lifeblood of cash flow. Yet, for many companies, the invoicing process remains trapped in the past – a manual, painstaking chore that quietly drains resources and stifles growth. In today’s fast-paced global economy, the question isn’t just how you send invoices, but Smart Invoicing vs Manual Invoicing, which of them is Costing Your Business Time and Money? At WeWire, we see how inefficient invoicing impacts businesses across the globe. We believe that true thought leadership in payments isn’t just about identifying problems; it’s about providing elegant, effective solutions that empower businesses to thrive. Let’s delve into the hidden costs of manual invoicing and why smart invoicing is the undisputed champion for financial efficiency. In this post, we’ll explore the real costs of manual invoicing, the invoicing automation benefits smart tools offer, and how WeWire’s Smart Invoicing feature is helping global businesses invoice clients and get paid faster, easier, and in any currency. If you’re still handling invoices in spreadsheets, PDFs, or through manual processes, here’s what it’s likely costing you: Manual invoice creation is time-intensive. You have to: According to a 2024 report by PayTech Journal, businesses spend up to 10 hours per week per finance team member managing invoicing manually. That’s time better spent on strategy or growth. Manually sent invoices are easy to miss, delay, or misplace. Add in cross-border challenges like currency mismatch or payment rail restrictions, and payments can take 5–10 business days or more to arrive. Typos, incorrect amounts, currency errors, forgotten taxes—it happens more often than we care to admit. And each error delays payment even further or introduces compliance risk. Let’s say you’re invoicing a client in the UK, but you’re based in Nigeria. You ask for USD, but they pay in GBP. Now what? Without smart currency handling, this adds layers of complexity and potential loss due to exchange rate fluctuations. Smart invoicing uses automation and real-time payment tools to eliminate friction from the invoicing process. Think of it as invoicing on autopilot—built for speed, accuracy, and scale. Here’s what a modern smart invoicing system looks like: ✅ Create customizable invoices No spreadsheets. No waiting. No guesswork. At WeWire, we’ve developed a smart invoicing solution specifically designed to tackle the pain points of manual and traditional cross-border payments. We understand that global businesses need flexibility, speed, and simplicity when dealing with international clients and multiple currencies. Here’s how WeWire’s invoicing feature works and benefits your business: Let’s say you run a payroll platform based in Ghana, with contractors in Nigeria, Kenya, and South Africa. You invoice your U.S. client in USD, they pay in USDC using the payment link, and WeWire settles you in GHS. Your contractors? They get paid in NGN, KES, and ZAR—seamlessly. Or, imagine you’re a SaaS platform working with merchants in the UAE. You invoice in AED, they pay in stablecoin, and WeWire settles you in EUR—automatically, quickly, and with full compliance built in. With WeWire’s Smart Invoicing, you’re not just getting paid faster—you’re: Doing a comparison of Smart Invoicing vs Manual Invoicing, you will quickly see that you’re leaving time, money, and opportunities on the table by not adopting the former. As global finance becomes more digital and decentralized, businesses that automate their invoicing and payment flows will lead the way. Smart invoicing isn’t just a convenience—it’s a competitive edge. With WeWire, you can invoice clients around the world, get paid in the way that works best for them, and receive settlement in the way that works best for you. That’s how cross-border business should work. Ready to simplify your invoicing?

diadem445c3650ff

The True Cost of Manual Invoicing

⏳ Lost Time

💸 Delayed Payments

🧮 High Error Rates

🌍 Currency Complications

What Is Smart Invoicing?

✅ Generate and share payment links instantly

✅ Accept payments in multiple currencies or stablecoins

✅ Reconcile payments automatically

✅ Get settlements in your preferred currencySmart Invoicing vs Manual Invoicing Comparison

Feature

Manual Invoicing

Smart Invoicing (e.g., WeWire)

Invoice creation

Manual entry, copy-paste

Customizable templates

Sending invoice

Email or PDF

Shareable payment link

Payment tracking

Manual reconciliation

Real-time tracking

Multi-currency support

Limited or requires separate tools

Built-in, automatic

Settlement currency

Often restricted to payer’s currency

You choose your preferred currency

Payment options

Bank transfer or card

Fiat + stablecoins (USDT, USDC)

Compliance & audit

Manual checks

Automated logs and reports

WeWire’s Smart Invoicing: Built for Global Business

Why It Matters: Real Use Cases

The Benefits Go Beyond Payments

Conclusion: Time to Get Smarter About Invoicing

👉 Try WeWire’s Smart Invoicing

👉 Talk to Sales