An Analysis of How the Cedi, Naira, and Rand Performed in H1 2025 Amid Trump’s Tariff Shock

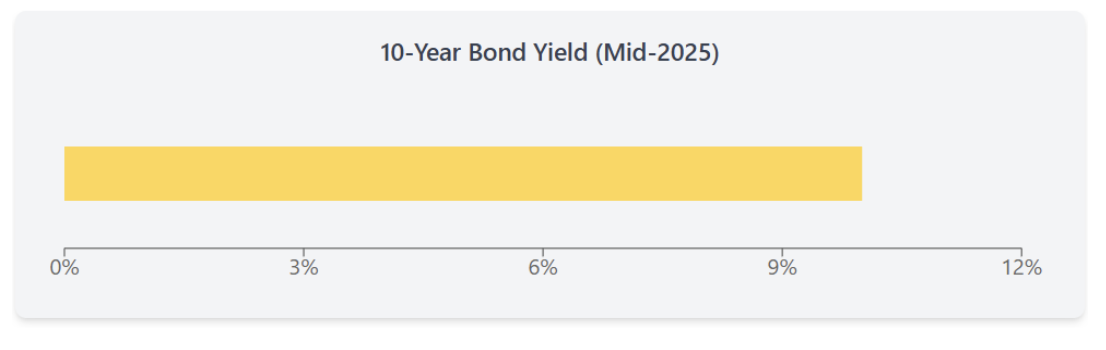

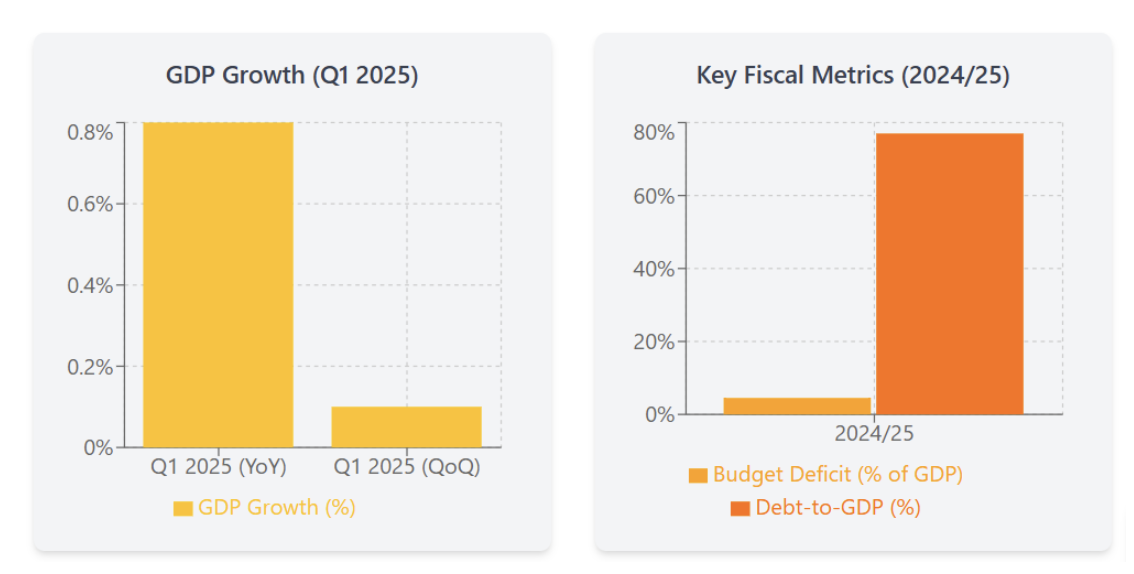

July 14, 2025 by johneb492254456 In the first half of 2025, African currencies navigated a volatile global landscape shaped by shifting U.S. trade policies, fluctuating commodity prices, and evolving domestic reforms. Central to this period was the shockwave triggered by former President Donald Trump’s unexpected reimposition of broad-based tariffs in April 2025, a policy pivot that rattled global markets, disrupted trade flows, and tested the resilience of emerging market currencies. For Africa’s key economies, Ghana, Nigeria, and South Africa, the tariff shock arrived amid distinct local challenges and macroeconomic transitions. Ghana was in the middle of an IMF-backed recovery, Nigeria continued to push through bold monetary and fiscal reforms, and South Africa faced structural growth constraints while navigating the impacts of elevated public debt and political realignment. This report provides an in-depth analysis of how the Ghanaian Cedi (GHS), Nigerian Naira (NGN), and South African Rand (ZAR) performed against the U.S. dollar during this turbulent period. Beyond currency movements, we explore a comprehensive set of macroeconomic indicators, including GDP growth, inflation trends, interest rates, fiscal balances, current account dynamics, foreign exchange reserves, credit ratings, investor sentiment, and sectoral developments. We also unpack the differentiated impact of Trump’s tariff policy on these three economies, highlighting why Ghana’s commodity-heavy export mix largely shielded it from direct tariff exposure, while South Africa’s vehicle and metals sectors faced significant headwinds. Through this lens, the report offers a country-by-country breakdown, supported by detailed charts and tables, to help analysts, policymakers, and investors understand the drivers behind each currency’s trajectory and the evolving macroeconomic risks and opportunities shaping the region’s financial landscape in 2025. Ghana’s economy rebounded strongly in early 2025. Official data show Q1 2025 GDP growth of +5.3% year-on-year, up from +3.6% in Q4 2024. This outpaced the IMF’s forecast (~4.0% for 2025). Growth was broad-based, led by mining (especially gold, up over 50% exports), construction, and services. The surge in gold exports (≈$11.6 billion in 2024) has driven a current-account swing to a small surplus (~2–3% of GDP annualized). Gross reserves jumped from about $6.0 bn in early 2024 to ~$10.7 bn by April 2025, covering roughly 4.7 months of imports. Inflation remains elevated (≈21% in Apr 2025), but is falling. On the fiscal side, Ghana is tightening. Despite higher revenues from mining, 2014’s budget slipped: the IMF reports a preliminary primary deficit of about –3.3% of GDP in 2024 (versus a target surplus of +0.5%). The 2025 budget aims for a 1.5% primary surplus, with steep spending cuts flagged by Finance Minister Forson. Debt restructuring and IMF support are key themes: Fitch recently upgraded Ghana’s sovereign rating to B- (stable) as it nears completion of debt relief (S&P likewise moved to CCC+). The upgrade reflects progress on fiscal consolidation and creditor agreements. Investor sentiment has improved. Local bond/T-bill yields have fallen to multi-year lows (e.g. 91-day T-bill ~15.9% in mid-March 2025). The cedi has recovered and remains stable around GHS 12–13 per USD. A modest currency strength is supported by the large gold windfall and resumed IMF disbursements (USD 370m approved in Apr’25). Summary (Ghana): Strong commodity exports drove a 5.3% GDP growth in Q1 2025, flipping the current account to surplus. Reserves are high ($10.7 bn) and ratings have been upgraded (Fitch to B-). Fiscal slippage in 2024 leaves a primary deficit (~3.3% GDP), but 2025 targets a surplus. Bond yields are falling, and reform momentum is bolstered by IMF support Nigeria’s economy shows signs of stability but remains constrained. Official GDP figures for Q1 2025 have been delayed, but Q4 2024 growth was +3.84% (the economy grew ~3.4% in full-year 2024). Analysts expect Q1 2025 growth near 3.8–3.9%, in line with Nigeria’s IMF forecast of 3.0% for 2025. Growth is driven by oil-sector investments and a rebound in agriculture, but high inflation (≈24% in May 2025) and monetary tightening constrain demand. On the budget front, Nigeria is tightening fiscal policy. The 2025 budget targets a deficit of ~3–4% of GDP (up from very wide deficits in 2023), financed largely by domestic bonds (N13.4 trn) and loans. Oil subsidy removal and lower inflation have eased the financing gap. The IMF notes that reforms (FX liberalization, subsidy cuts, monetary tightening) have markedly improved Nigeria’s external and fiscal position. Although fiscal data are still incomplete, markets are optimistic: Fitch upgraded Nigeria’s sovereign rating to B (stable) in April 2025 and Moody’s to B3 (stable) in May, citing better reserves and fiscal discipline. Nigeria’s debt-to-GDP has jumped (≈55% by 2024), but most borrowing is in local currency, mitigating immediate rollover risk. External accounts have swung to surplus. Nigeria posted a Q1 2025 trade surplus of ₦5.17 trillion (~$6.7 bn) as oil export receipts rose (+7.4% YoY) and imports cooled (-7.0% QoQ). Oil (62.9% of exports) and agricultural exports are buoyant. Net foreign reserves hit ~$40.2 bn at end-2024 (a 3-year high), partly by reducing central-bank FX swaps. The CBN notes that net reserves (after adjusting for liabilities) have risen sharply, boosting confidence. However, first-quarter 2025 saw a seasonal dip in reserves (due to debt service and FX outflows), though officials expect a recovery in H2. Investor sentiment is cautiously positive. Nigerian government bond yields have been trending down (average sovereign yield ~18.6% in late June 2025), reflecting easing inflation and scant new bond supply. The March 2025 FGN bond auction was 6x oversubscribed. Meanwhile, the naira has stabilized around ₦750–770 per USD since FX market reforms. Portfolio inflows have risen modestly (some local analysis notes ~$3.8bn net foreign inflows in early 2025). Sector notes: Oil remains dominant. Nigeria’s OPEC+ quota is pegged at 1.5 mbpd for 2025, limiting output (OPEC decision from late 2024). Falling global oil prices in H1 2025 (Brent $70–80) weigh on receipts. The government aims to boost non-oil growth via gas exports and agriculture (cocoa, rubber). Banking sector reforms (recapitalization, transparency) continue to shore up financial stability. South Africa’s economy remains weak. Q1 2025 GDP grew just +0.8% YoY (+0.1% q/q), barely above stall speed. This reflects a contraction in mining and manufacturing, offset only by a surge in agriculture (+15% YoY). The new coalition government has succeeded in keeping the lights on (uninterrupted power since late 2024), but structural constraints – slow reforms and rising fiscal pressures – limit growth. The IMF sees GDP ~1.0% in 2025, in line with government forecasts. Fiscal deficits are high. The main budget deficit was roughly 4.5% of GDP in 2024/25, one of the world’s largest for a middle-income country. Debt is rising (~77% of GDP). The May 2025 budget projects narrowing deficits (3.4% by 2027) through spending cuts and a gradual VAT increase, but these are politically sensitive. Revenue has underperformed due to weak growth, and debt service consumes ~20% of revenue. Rating agencies keep South Africa in sub-investment grade: S&P and Fitch at BB- (stable), Moody’s Ba2 (stable), citing heavy debt and reform risk despite some political improvements. The external position is moderately stable but prone to shocks. In Q1 2025, South Africa ran a current account deficit of ~0.5% of GDP, unchanged from late 2024. Merchandise trade has a small surplus (R221.2 bn in Q1) as exports (minerals, vehicles) roughly match imports. However, services and income outflows widen the overall deficit. Gross international reserves (including gold) are ample (~$68 bn in May 2025), though the core (non-gold) reserves are ~50 bn. The rand is volatile but roughly flat in H1 2025 (≈ZAR 17–18/USD). Debt markets demand high yields. South Africa’s 10-year bond yield is around 10% (as of mid-2025), reflecting risk from fiscal widening and global rate uncertainty. Investors are cautious: local institutional funds dominate the debt market, and foreign participation is limited. However, confidence has ticked up on the hope that the coalition government can implement reforms (ratings analysts note that reaching sustained ~2% growth and stabilizing debt would be needed for an upgrade). Key sectors: South Africa’s exports include minerals (gold, platinum), agricultural products, and automobiles. Notably, vehicle exports to the US (~$2 bn/year) are now hit by Trump’s 25% tariff on foreign cars. More broadly, Trump imposed a 31% tariff on South Africa in Apr 2025 as part of a “reciprocal” tariff list. These duties (also hitting steel, wine, etc.) threaten to erode AGOA preferences and could shave ~0.2–0.3 percentage points off GDP. On the domestic front, long-delayed energy-sector reforms (rail, ports, telecoms) are underway but will take time to yield growth.

johneb492254456

Ghana: Gold-Driven Recovery and Stabilization

Nigeria: Reform Momentum Amid Mixed Signals

Summary (Nigeria): Growth is modest (~3–4%), supported by rebounding oil and agriculture. Fiscal austerity (subsidy cuts, tighter budgets) and monetary reform have improved Nigeria’s credit profile (Fitch to B, Moody’s B3). The trade account is in surplus (oil-led), and FX reserves are near 7-year highs. Bond markets are firming (yields falling). Risk remains from high inflation and security issues, but policies are broadly market-friendly.

Summary (Nigeria): Growth is modest (~3–4%), supported by rebounding oil and agriculture. Fiscal austerity (subsidy cuts, tighter budgets) and monetary reform have improved Nigeria’s credit profile (Fitch to B, Moody’s B3). The trade account is in surplus (oil-led), and FX reserves are near 7-year highs. Bond markets are firming (yields falling). Risk remains from high inflation and security issues, but policies are broadly market-friendly.South Africa: Fragile Growth and High Debt

Summary (South Africa): Growth is weak (~0.8% in Q1) and fiscal deficits are large (~4.5% of GDP). The current account is nearly balanced, and reserves are high, but debt/GDP is rising. Credit ratings are low (BB-/Ba2), reflecting persistent policy risks. Investor confidence is still fragile, keeping bond yields around 10%. A positive development is a stable power supply, but trade shocks loom: Trump’s steep tariffs (31% on South Africa, including 25% on autos) could cut exports, slow growth, and fuel inflation.

Summary (South Africa): Growth is weak (~0.8% in Q1) and fiscal deficits are large (~4.5% of GDP). The current account is nearly balanced, and reserves are high, but debt/GDP is rising. Credit ratings are low (BB-/Ba2), reflecting persistent policy risks. Investor confidence is still fragile, keeping bond yields around 10%. A positive development is a stable power supply, but trade shocks loom: Trump’s steep tariffs (31% on South Africa, including 25% on autos) could cut exports, slow growth, and fuel inflation.

Dollars or Death: Why African SMEs Are Addicted to a Currency They Don’t Print

July 14, 2025 by johneb492254456 African Small and Medium Enterprises (SMEs) form the backbone of the continent’s economy, driving job creation, innovation, and economic growth. However, these businesses face a critical challenge: an overreliance on the US dollar, a currency they neither print nor control. This dependency has become a matter of survival, as the US dollar is essential for importing goods, servicing debts, and conducting international trade. With approximately 70% of African countries experiencing foreign exchange (FX) shortages, SMEs struggle to secure the dollars needed to import essential goods, threatening their operations and growth. The real import crisis is not just about cargo—it’s about currency. This week’s StayWired presentation explores why African SMEs are so dependent on the US dollar and investigates whether alternative currencies, such as stablecoins or trade tokens, can provide a viable solution to this pressing issue. The US dollar’s dominance in the global economy profoundly impacts African economies. As the world’s primary reserve currency, it accounts for over 50% of low and middle-income countries’ sovereign debt, including many African nations. In Africa, the dollar is indispensable for international trade, with most commodities priced in dollars and the majority of imports paid for in dollars. Countries like Nigeria, Ghana, and Zambia rely heavily on dollar-denominated transactions to import essential goods such as machinery, raw materials, and food. However, this dependency has significant drawbacks. A rising US dollar increases the cost of servicing dollar-denominated debt, as evidenced by Nigeria’s expenditure of $3.5 billion on foreign debt servicing in the first nine months of 2024. African SMEs operate in a challenging environment, with limited access to finance and foreign exchange posing significant hurdles. Only one-third to one-fifth of SMEs in Sub-Saharan Africa have access to financial instruments like bank loans, and approximately 28.3% are entirely credit-limited, restricting their ability to grow or sustain operations. The scarcity of US dollars exacerbates these challenges, as SMEs require dollars to import critical goods such as raw materials and machinery. For example, Nigerian SMEs face significant obstacles in accessing dollars, with the country’s total debt surpassing $100 billion, straining foreign exchange reserves. The rising dollar increases import costs, eroding profit margins and hindering growth. The import crisis in Africa is fundamentally a currency crisis. With 70% of African countries facing FX shortages, SMEs struggle to secure the dollars needed to pay for imports, leading to supply chain disruptions and increased costs. Countries like Nigeria, Ghana, and Zambia have experienced severe dollar shortages, which have impaired their ability to import essential goods. For instance, Nigeria’s naira has weakened significantly, making imports more expensive and reducing the competitiveness of local businesses. Stablecoins, such as USDT (Tether) and USDC (USD Coin), are emerging as a promising solution to Africa’s FX shortages and currency volatility. These digital currencies, pegged to the US dollar, provide a stable medium of exchange that is not subject to the volatility of local currencies. In Africa, stablecoins are gaining traction for cross-border payments and trade. In Nigeria, stablecoins account for a significant portion of crypto transaction volumes, with USDT representing around 5% of the total trading volume on platforms like Paxful. Ethiopia saw a 180% year-over-year growth in stablecoin transfers in 2024, following the devaluation of its currency, the birr, by 30%. Stablecoins enable SMEs to hedge against local currency devaluation, store value, and conduct international trade without relying on traditional banking systems. Stablecoins are already transforming the operations of African SMEs. In Nigeria, small merchants are increasingly using stablecoins like USDT and USDC for business-to-business (B2B) payments with exporters, particularly from Asia. For example, Nigerian SMEs use peer-to-peer transfer options to pay Chinese suppliers, bypassing the need to travel with cash or navigate restrictive banking systems. This shift was spurred by the Nigerian government’s restrictions on dollar transfers, which have pushed businesses toward alternative solutions. However, regulatory challenges persist. South Africa’s Financial Sector Conduct Authority (FSCA) has classified crypto assets as financial products, indicating a move toward greater oversight, but many African countries still lack clear regulatory frameworks for stablecoins. Despite these hurdles, the growing adoption of stablecoins underscores their potential to address Africa’s FX challenges and support SME growth. The dependency of African SMEs on the US dollar is a double-edged sword: it is essential for participating in global trade, yet it exposes them to the risks of currency volatility and FX shortages. The import crisis highlights the urgent need for alternative solutions, and stablecoins have emerged as a viable option. With Africa leading the world in stablecoin adoption—particularly in countries like Nigeria and South Africa—these digital currencies could play a transformative role in the continent’s economic future. Stablecoins offer SMEs a stable, accessible, and cost-effective way to conduct cross-border payments, hedge against local currency devaluation, and participate in global trade. However, for stablecoins to reach their full potential, African regulators must establish clear frameworks to ensure their safe and legal use. As the global economy moves toward digitalization, African SMEs may find that stablecoins are not just a temporary solution but a cornerstone of their long-term growth strategy. The question remains: will Africa’s financial future be defined by dollars or by digital innovation?

johneb492254456

Moreso, the dollar’s strength fuels inflation in African economies by raising import costs, with Nigeria experiencing 32.7% inflation in September 2024. Global events, such as the COVID-19 pandemic and geopolitical conflicts, have further disrupted exports and worsened terms of trade, amplifying the dollar’s impact. Historically, the dollar’s role as the world’s reserve currency, established post-World War II through the Bretton Woods system, has entrenched its influence in African trade and finance.

Moreso, the dollar’s strength fuels inflation in African economies by raising import costs, with Nigeria experiencing 32.7% inflation in September 2024. Global events, such as the COVID-19 pandemic and geopolitical conflicts, have further disrupted exports and worsened terms of trade, amplifying the dollar’s impact. Historically, the dollar’s role as the world’s reserve currency, established post-World War II through the Bretton Woods system, has entrenched its influence in African trade and finance. Moreover, SMEs often resort to informal or alternative channels to access dollars, which carry higher risks and costs. This dependency on the dollar exposes SMEs to currency market volatility, where sudden fluctuations can devastate their businesses, making it difficult to plan or invest in the future.

Moreover, SMEs often resort to informal or alternative channels to access dollars, which carry higher risks and costs. This dependency on the dollar exposes SMEs to currency market volatility, where sudden fluctuations can devastate their businesses, making it difficult to plan or invest in the future. This crisis has broader economic implications: inflation rises as import costs increase, and economic growth slows as SMEs scale back operations or shut down entirely. Global events, such as the COVID-19 pandemic, which reduced export earnings, and geopolitical conflicts, which have driven up commodity prices, have intensified these challenges. For SMEs, which lack the financial buffers of larger corporations, the inability to access dollars can be catastrophic, threatening their survival in an increasingly globalized economy.

This crisis has broader economic implications: inflation rises as import costs increase, and economic growth slows as SMEs scale back operations or shut down entirely. Global events, such as the COVID-19 pandemic, which reduced export earnings, and geopolitical conflicts, which have driven up commodity prices, have intensified these challenges. For SMEs, which lack the financial buffers of larger corporations, the inability to access dollars can be catastrophic, threatening their survival in an increasingly globalized economy. They also offer significant cost savings, with transaction fees as low as 0.1% compared to the 8.3% average cost for sending $200 to Sub-Saharan Africa via traditional remittance channels, according to the World Bank. However, challenges such as regulatory uncertainties and the need for greater financial literacy among SMEs must be addressed to ensure widespread adoption.

They also offer significant cost savings, with transaction fees as low as 0.1% compared to the 8.3% average cost for sending $200 to Sub-Saharan Africa via traditional remittance channels, according to the World Bank. However, challenges such as regulatory uncertainties and the need for greater financial literacy among SMEs must be addressed to ensure widespread adoption.

Why Stablecoins Might Be Africa’s Best Shot at Cross-Border Payment Freedom

johneb492254456

July 14, 2025 by johneb492254456

In Africa, cross-border payments are often hindered by high costs, slow processing times, and complex regulatory environments. Stablecoins, a type of cryptocurrency designed to maintain a stable value, offer a promising solution to these challenges. Using the power of blockchain technology, stablecoins can facilitate settlements between countries without a shared clearing house or a convertible currency, offering a faster, cheaper, and more accessible alternative to traditional financial systems. This week’s StayWired presentation explores how stablecoins are revolutionizing cross-border payments in Africa, their real-world applications, and their potential to reshape the continent’s financial future.

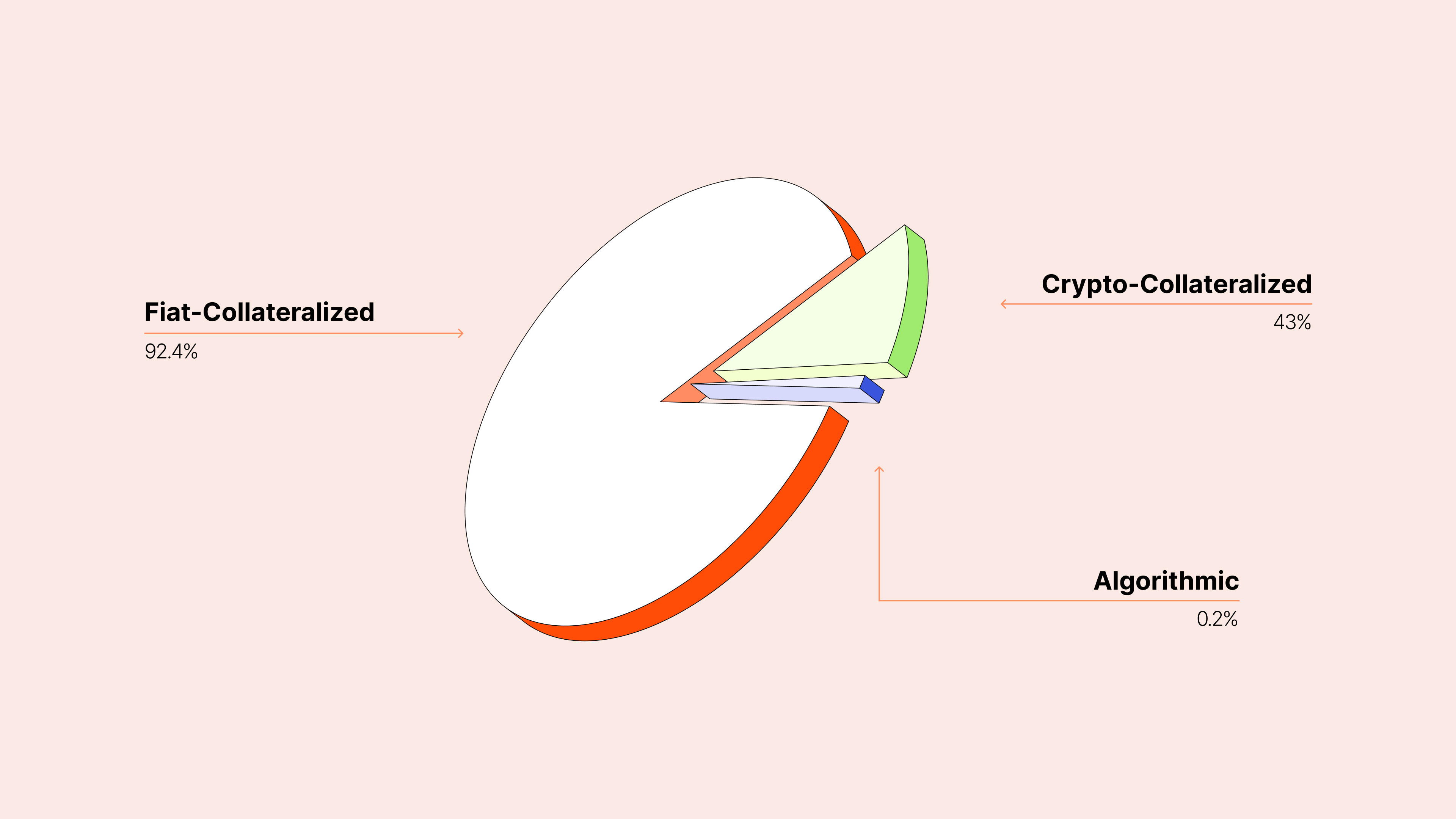

Stablecoins are cryptocurrencies engineered to maintain a stable value by being pegged to assets like fiat currencies (e.g., US dollar) or commodities (e.g., gold). Unlike volatile cryptocurrencies such as Bitcoin, stablecoins provide the benefits of digital currency—speed, security, and decentralization—without significant price fluctuations. There are three primary types of stablecoins: fiat-collateralized, backed by reserves of fiat currency like Tether (USDT) and USD Coin (USDC); crypto-collateralized, backed by other cryptocurrencies like DAI; and algorithmic, which use algorithms to control supply, such as Frax (FRAX). According to DefiLlama, as of July 2025, fiat-collateralized stablecoins dominate with approximately 92.35% of the $255 billion stablecoin market, followed by crypto-collateralized at 7.45%, and algorithmic at 0.2%.

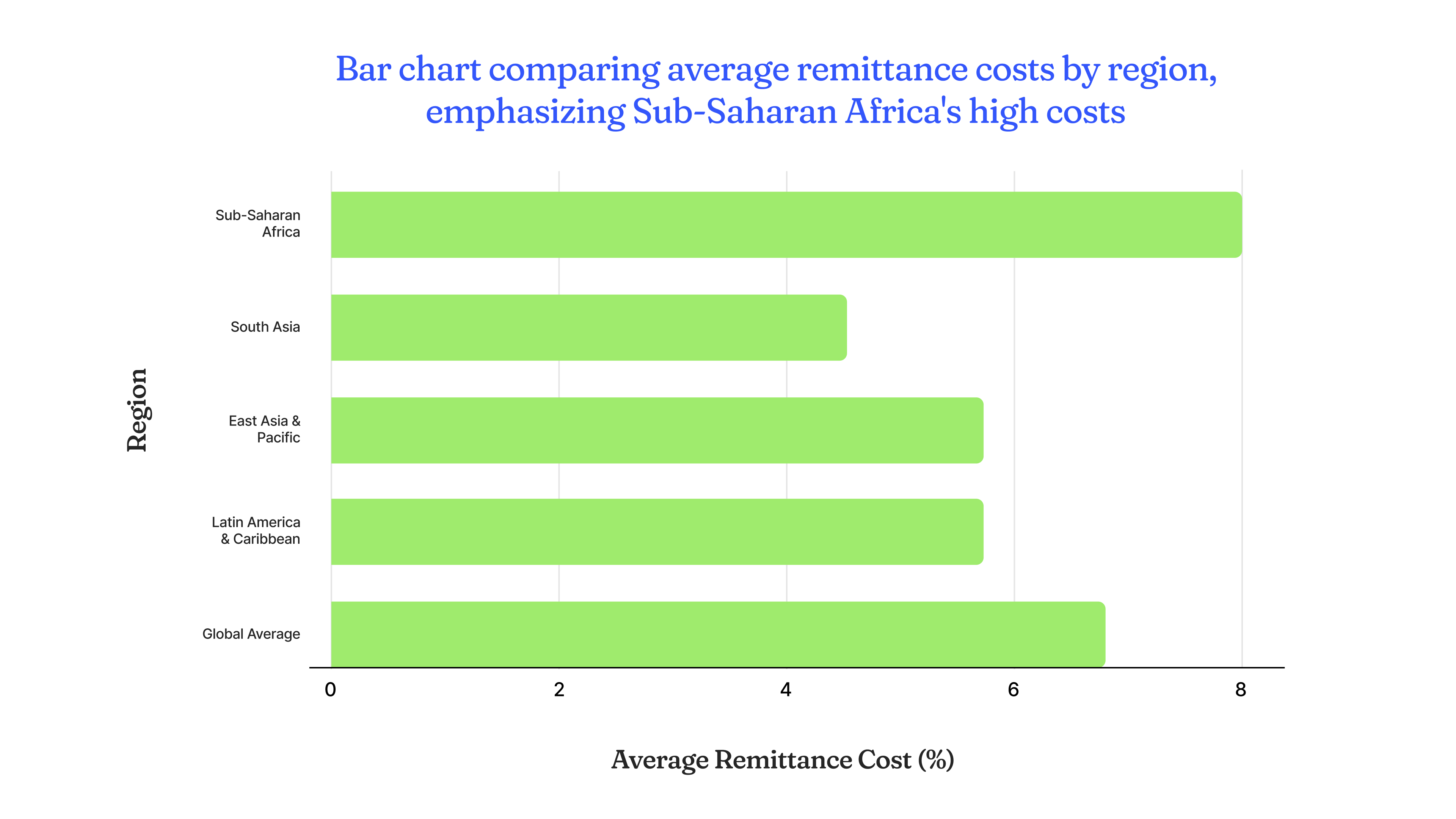

Cross-border payments in Africa face significant obstacles that hinder economic growth and financial inclusion. According to the World Bank, Sub-Saharan Africa is the most expensive region for remittances, with an average cost of 8% for a $200 transfer, compared to the global average of 6.62%. Transactions often take days to settle due to multiple intermediaries and outdated banking infrastructure. Regulatory disparities across African countries create additional complexities, as do currency exchange issues stemming from the limited convertibility and volatility of many African currencies. For instance, 70% of African countries face foreign exchange shortages, making access to stable currencies like the US dollar challenging. Security concerns, such as fraud, and infrastructure gaps further exacerbate these issues, impacting businesses, freelancers, and individuals reliant on cross-border transactions.

Stablecoins leverage blockchain technology to address the core challenges of cross-border payments in Africa. They enable transactions to settle in seconds or minutes, compared to days for traditional methods, as noted in industry reports from sources like Mural. Transaction fees are significantly lower, often less than 1%, compared to the 8% or more charged by conventional remittance services. Blockchain’s transparent ledger provides auditable records, reducing fraud risks and enhancing trust. Stablecoins are accessible to anyone with a smartphone, making them a vital tool for the unbanked, with only 49% of adults in Sub-Saharan Africa having a bank account, according to the World Bank. By reducing reliance on intermediaries like banks and clearing houses, stablecoins streamline processes and lower costs, offering a practical solution for Africa’s fragmented financial systems.

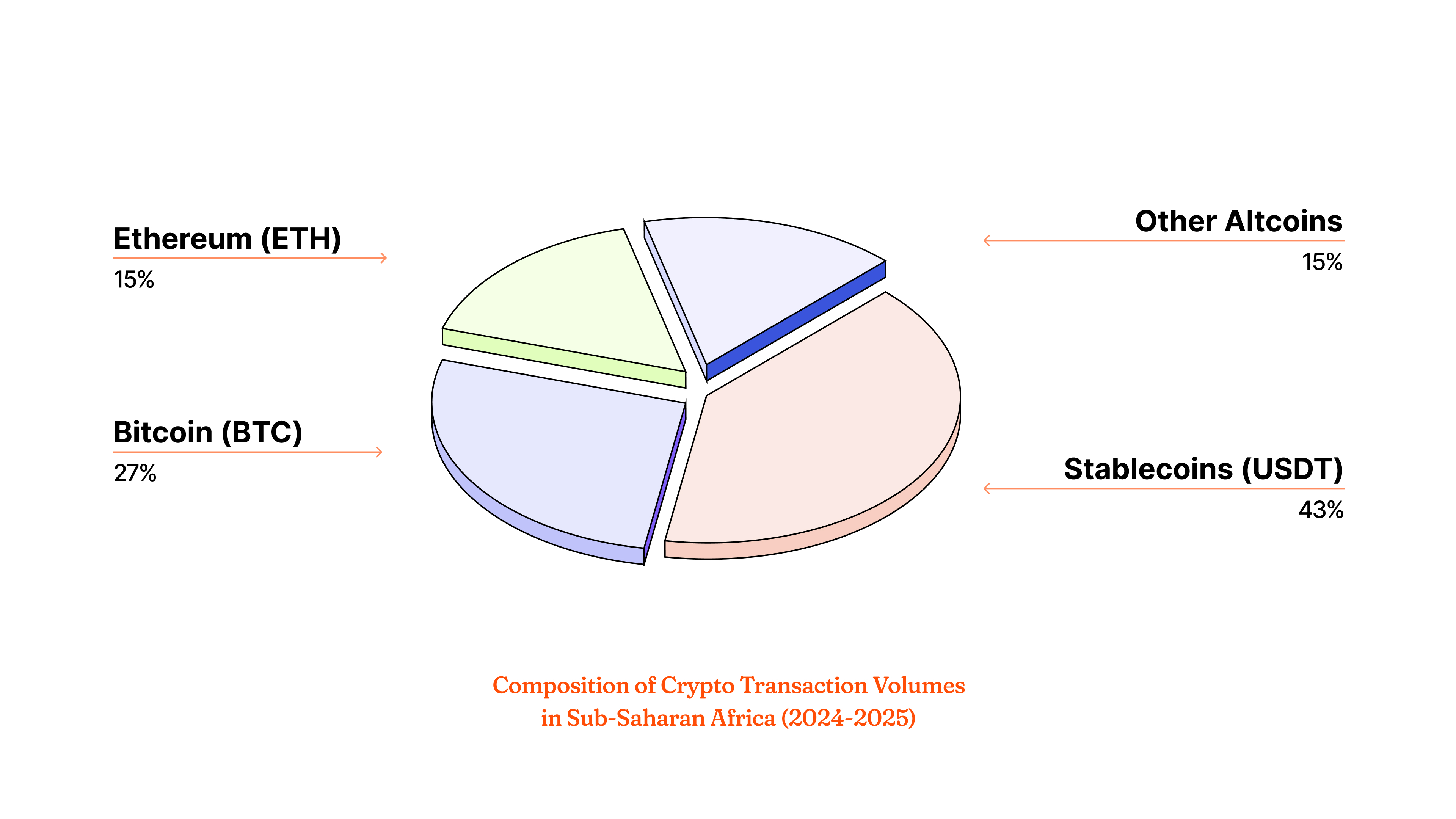

Stablecoins are already transforming cross-border payments in Africa. In Nigeria, small merchants use USDT and USDC for business-to-business payments with suppliers in Asia, avoiding the need to carry physical cash or navigate complex banking systems, as reported by Rest of World. In Kenya, mobile money platforms like M-Pesa have integrated stablecoins, enabling faster and cheaper remittances for users. According to a 2024 Chainalysis report, stablecoin transactions in Sub-Saharan Africa reached approximately $54 billion, accounting for 43% of the region’s total crypto transaction volume of $125 billion. This growth reflects stablecoins’ practical applications in remittances, small business payments, and freelance salaries, particularly in countries with volatile currencies like Nigeria and Ethiopia, where stablecoin transfers surged 180% year-over-year following currency devaluation.

The future of stablecoins in Africa is promising, driven by their ability to address financial inclusion and cross-border trade challenges. Experts predict continued growth, with stablecoins potentially becoming the primary crypto use case in South Africa within the next three to five years, according to Rob Downes of ABSA Bank. The $54 billion in stablecoin transactions in 2024 is expected to grow as infrastructure improves and awareness increases. Regulatory developments, such as South Africa’s efforts to establish stablecoin regulations, will provide clarity and foster adoption. Stablecoins could reduce remittance costs, enhance trade efficiency, and empower the unbanked, contributing to economic growth. Collaborations with global partners and investments in African fintech startups will further accelerate stablecoin integration, positioning Africa as a leader in global digital asset adoption.

The future of stablecoins in Africa is promising, driven by their ability to address financial inclusion and cross-border trade challenges. Experts predict continued growth, with stablecoins potentially becoming the primary crypto use case in South Africa within the next three to five years, according to Rob Downes of ABSA Bank. The $54 billion in stablecoin transactions in 2024 is expected to grow as infrastructure improves and awareness increases. Regulatory developments, such as South Africa’s efforts to establish stablecoin regulations, will provide clarity and foster adoption. Stablecoins could reduce remittance costs, enhance trade efficiency, and empower the unbanked, contributing to economic growth. Collaborations with global partners and investments in African fintech startups will further accelerate stablecoin integration, positioning Africa as a leader in global digital asset adoption.

Nigeria Oil & FX Outlook: H1 2025 Review and Q3 Outlook amid Iran–Israel Conflict

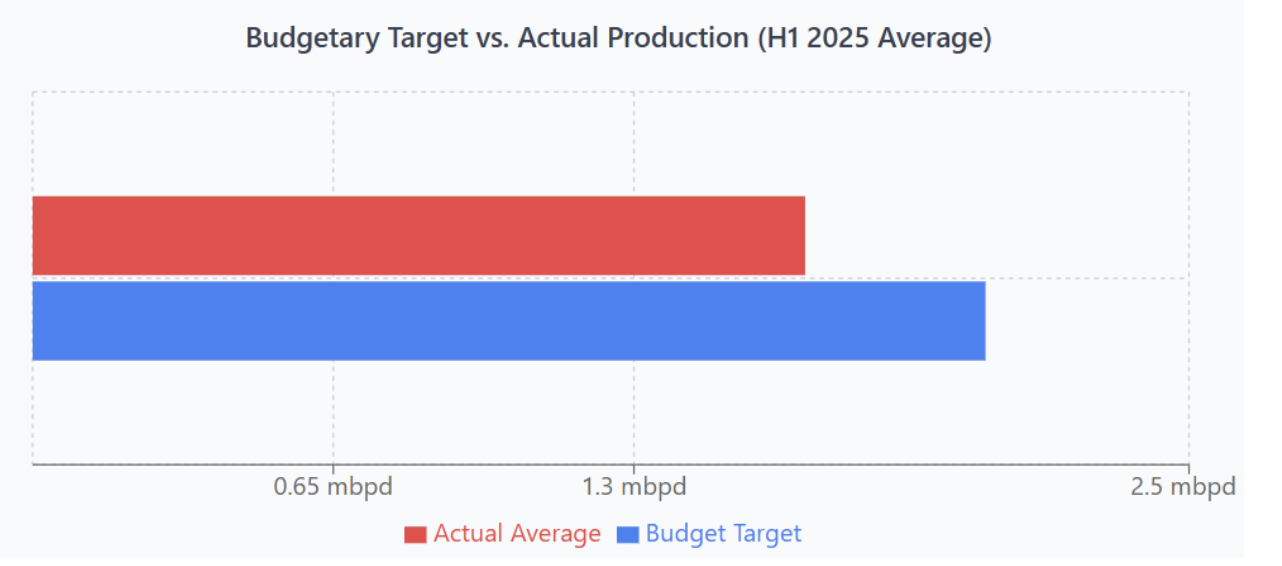

June 27, 2025 by johneb492254456 In the first half of 2025, Nigeria’s oil production remained underwhelming, continuing a multi-year struggle to meet output targets. Crude oil output, including condensates, hovered between 1.6 to 1.7 million barrels per day (mbpd), a figure significantly below the federal government’s budgetary benchmark. Specifically, production peaked modestly at approximately 1.74 mbpd in January, according to industry data, before declining to around 1.65 mbpd by May. Data released by the Nigerian National Petroleum Company (NNPC) shows that actual crude output in April was approximately 1.61 mbpd, underscoring the country’s chronic inability to meet its OPEC quota or internal fiscal assumptions. The 2025 national budget, based on projections of 2.06 mbpd in average daily production for H1, was overly optimistic. The medium-term outlook from the Ministry of Finance and the Nigerian Upstream Petroleum Regulatory Commission (NUPRC) even targets 2.5 mbpd in the near future, a benchmark that has increasingly seemed aspirational rather than attainable. In reality, the deficit between projected and realized production levels in H1 2025 was stark, ranging between 20% and 25%. This shortfall has had direct consequences for oil revenues, dollar inflows, and fiscal planning, as oil remains the dominant source of government income and foreign exchange. A persistent and structurally damaging factor behind Nigeria’s underperformance is the enduring challenge of oil theft and pipeline vandalism. According to investigative reports and statements from security agencies, the country is losing an estimated 200,000 barrels per day to illicit siphoning and sabotage along critical pipelines, particularly in the Niger Delta. These losses are not only draining government revenue but also discouraging investment and affecting the reliability of supply contracts with international buyers. In many cases, operators have been forced to shut down or defer production due to security concerns or export terminal disruptions caused by theft-induced downtime. Adding to the complexity is the role of Nigeria’s domestic refining resurgence, led by the Dangote Refinery. This massive 650,000 barrels per day facility, which began scaling operations in early 2025, has begun absorbing a significant share of locally produced crude. According to the NNPC, Dangote alone is expected to refine roughly 99.5 million barrels over the year, a figure that already began impacting H1 crude export volumes. The broader local refining system, combining Dangote and smaller modular refineries, now demands approximately 770,000 barrels per day, representing over one-third of Nigeria’s total daily output. While this has greatly reduced Nigeria’s dependence on costly fuel imports, it has simultaneously diverted export-bound crude, further affecting oil revenue generation from foreign markets. The combined effect of subdued production, theft-related losses, and increased domestic crude allocation has reduced the volume of Nigerian crude available for international export. Export performance in H1 2025 reflected this dynamic: according to NBS data aggregated by Nairametrics, Nigeria earned ₦12.96 trillion from crude oil sales in Q1 2025, a figure that represents roughly 63% of total exports for the period. However, this figure marks a 16% decline compared to Q1 2024, suggesting that despite more favorable pricing conditions in late Q2, overall export earnings from oil in early 2025 remained soft. Yet, not all export dynamics were negative. Nigeria’s non-crude petroleum exports, such as petrochemicals and LNG, posted noticeable gains, benefiting from improved capacity utilization and expanded trade ties, particularly with India, the United States, and several European countries. This diversification, though still marginal about crude exports, points toward a slow but meaningful shift in Nigeria’s export mix. In essence, Nigeria’s oil production and export trajectory in H1 2025 was shaped by an intricate combination of structural deficits, security challenges, infrastructural shifts, and ambitious fiscal assumptions. While the country did manage to maintain output within the 1.6–1.7 mbpd range, this level fell short of both domestic budget needs and external obligations. The implications of this underperformance have already started to manifest in oil revenue shortfalls and FX availability constraints, although later Q2 price spikes related to Middle East geopolitical tensions may help cushion the fiscal blow heading into Q3. In the first half of 2025, international oil markets moved through a distinctly two-phase pricing environment, marked initially by subdued pricing and later disrupted by geopolitical shocks. Nigeria’s benchmark crude, Bonny Light, which closely tracks global Brent prices, traded within a relatively moderate band of $70 to $75 per barrel for most of the half-year period. These figures were largely in line with the federal budget benchmark of $75 per barrel, providing some level of fiscal predictability in the earlier months of the year. However, by May, signs of oversupply were beginning to weigh on market sentiment. Brent crude prices fell to around $65 per barrel during that month, reflecting both muted global demand and expectations of increased output from key producers. This downward drift was supported by forecasts from the U.S. Energy Information Administration (EIA), which had projected that, barring major shocks, global oil markets would remain oversupplied in 2025, potentially dragging Brent prices down to an average of $61 per barrel by year-end. This bearish outlook was rooted in expectations of inventory build-ups, weaker-than-expected industrial demand in Europe and China, and the phased unwinding of OPEC+ production cuts. That trajectory, however, changed abruptly in June as geopolitical tensions in the Middle East escalated sharply. The intensification of the Iran–Israel conflict sent a ripple of uncertainty through global commodity markets. Investors and analysts responded swiftly to the increased risk of supply disruptions, particularly concerning the strategic Strait of Hormuz, a maritime chokepoint responsible for transporting a significant percentage of the world’s seaborne oil. As a result, Brent prices reversed course and surged to between $77 and $81 per barrel by the latter part of June, marking the highest levels seen since early January. Bonny Light, which typically commands a slight premium over Brent due to its low sulfur content and high gasoline yield, traded around $79 per barrel during the same period. This late-quarter price rally proved to be a significant fiscal windfall for Nigeria. With a large portion of federal revenues and foreign exchange earnings tied to crude oil exports, even modest increases in the price per barrel have a multiplicative impact on national revenue performance. The jump in prices during June not only helped offset earlier shortfalls triggered by lower production volumes but also improved Nigeria’s external earnings potential heading into the third quarter. Moreover, the sudden shift in pricing dynamics highlighted the volatility of Nigeria’s fiscal outlook, which remains highly sensitive to global energy geopolitics. In effect, H1 2025 can be characterized as a tale of two quarters, one of moderation and caution, followed by a sharp revaluation in oil markets that caught many observers by surprise. While the gains in June helped Nigeria edge closer to its budgetary assumptions, they also served as a stark reminder that global oil prices remain vulnerable to geopolitical flashpoints and that any fiscal strategy tied to hydrocarbons must be inherently adaptive and risk-aware. The naira has traded in a relatively tight range (₦1,400–1,600 per $) since early 2025, reflecting greater FX stability. The unified interbank (I&E) rate has been roughly ₦1,500–1,520 in mid-2025, while the parallel (“black”) market hovers ~₦1,590. According to analysts, the parallel market is now only ~5% above the official rate, indicating limited arbitrage. Higher oil receipts and remittance inflows are expected to keep the naira supported; one analyst notes that the recent oil‑price bump “could improve FX reserves by 15% and stabilize the naira”. The CBN has offered FX through weekly wholesale auctions and raised deposit and lending rates to defend the currency (MPR ~24.5%), while liquidity in foreign exchange markets appears ample. Overall, H1 saw a gradual strengthening (or at least stability) of the naira driven by better FX inflows, with little need for drastic central‑bank interventions so far. Nigeria recorded a trade surplus in Q1 2025 (≈₦5.17 trillion) largely because imports fell faster than exports. The collapse in fuel imports (thanks to Dangote’s output) was a key factor. On the capital side, foreign portfolio flows have remained muted – global rate hikes and regional volatility keep many international investors on the sidelines. However, diaspora remittances (always one of the highest in Africa) continued to support FX supply through official channels. Externally, Nigeria’s reserve buffers are ample: end‑January 2025 reserves were $38.88 billion (≈8.8 months of goods imports). This is down slightly from December 2024 ($40.19 b) but still well above minimum thresholds. With trade surplus and higher oil earnings, reserves are likely to drift higher in H1. In short, Nigeria’s external position in H1 was healthy – sizable reserves, trade surplus, and steady remittances – even as capital inflows remained lackluster. The Middle East conflict (mid‑June 2025 onward) sent shockwaves through oil markets. After U.S. and Israeli strikes on Iran, Brent briefly reached ~$81.4/barrel (a five-month peak) on June 23. Prices jumped ~$12–14 from May to mid‑June (Brent ~$65→$77), largely due to fears that Iran might close the Strait of Hormuz. Nigeria’s crude benefited: Bonny Light traded ~4% above Brent (≈$79). At Nigeria’s H1 output (~45 million barrels/month), the price rise translates into roughly +$630 million extra oil income in June. In percentage terms, analysts suggest this windfall could boost FX reserves by ~15%. In other words, the conflict has materially improved Nigeria’s oil receipts and bolstered FX. However, there are important trade-offs. Higher international oil prices have lifted domestic fuel prices: petrol briefly reached N915–N925/liter in Lagos (versus ~N885 prior), stoking inflationary pressure. Experts warn of “dual risks” – imported inflation and potential capital flight to safe assets – that could tighten liquidity in FX markets. In sum, the conflict-driven oil spike is a net positive for Nigeria’s revenues and reserves, but it also heightens inflation and may induce cautious capital reallocations abroad. Several forces will shape the near-term outlook: the course of the Iran–Israel war, OPEC+ policy, global demand trends, and Nigeria’s own reforms. Key scenarios include: In summary, H1 2025 saw subdued output and a mixed revenue picture, but a sudden price shock improved prospects. For Q3, much depends on the Middle East conflict and OPEC+ actions. A sustained oil rally would benefit government coffers and the naira, whereas a reversal (via conflict easing or oversupply) would revive budgetary and FX pressures. Policymakers should prepare for either path by shoring up fiscal buffers when possible and ensuring liquidity. Overall, Nigeria’s ample reserves (∼9 months cover) provide some cushion, but the nation’s fortunes will ride on how these global and domestic factors unfold in the coming quarter.

johneb492254456

H1 2025 Oil Production & Exports

H1 2025 Oil Prices

USD/NGN and FX Liquidity

Capital Flows & Reserves

Impact of Iran–Israel Conflict

Q3 2025 Outlook (Scenarios)

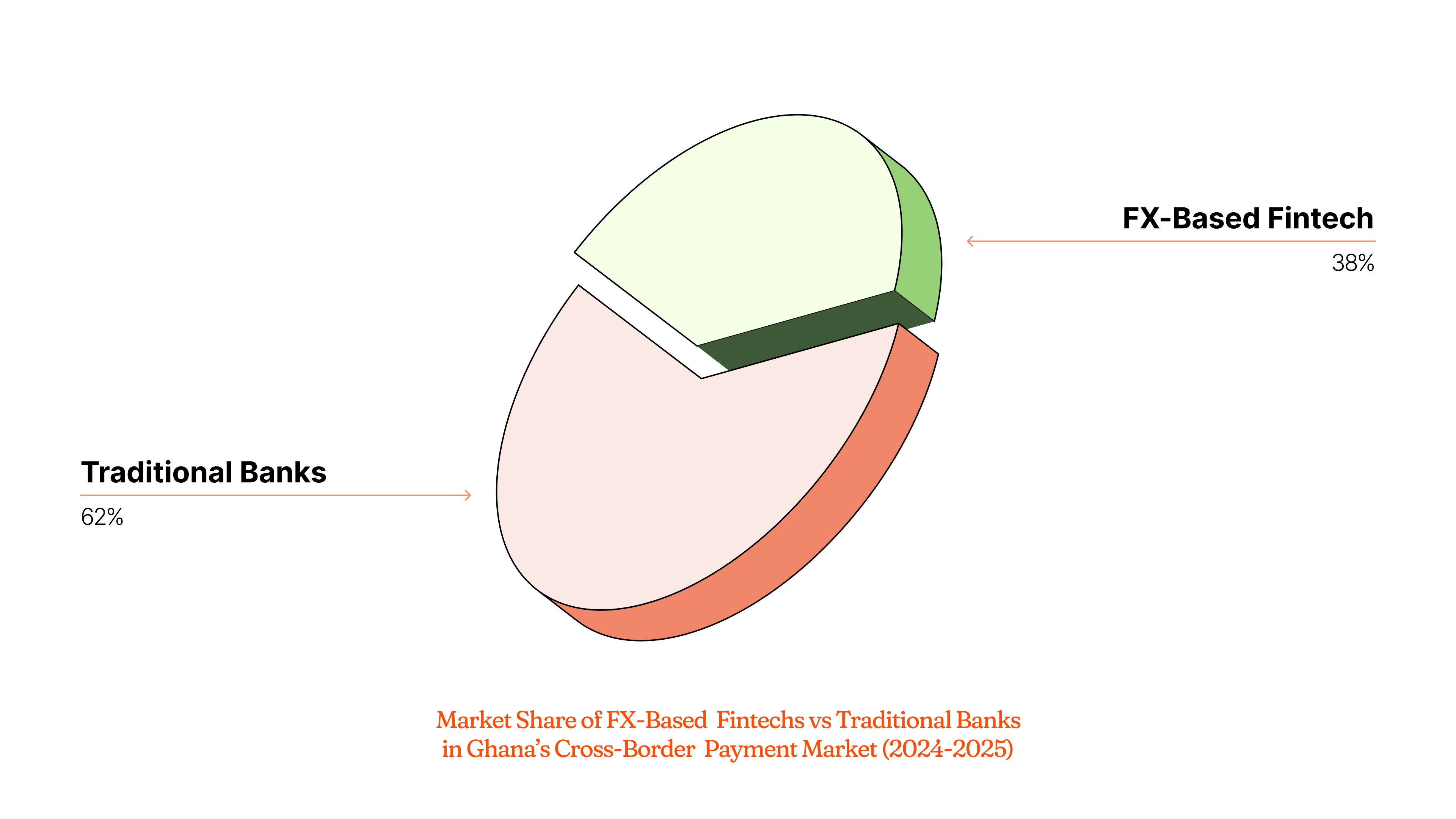

Why the Cedi's Surge Could Change Ghana’s Fintech Playbook

June 24, 2025 by johneb492254456 Ghana’s Cedi has staged an extraordinary recovery in 2025, appreciating by 42% against the US dollar since January, trading at approximately GHS 10.20/USD by late May. This surge, a stark contrast to its 45.1% depreciation in 2022, is driven by a combination of robust macroeconomic policies and favorable global conditions. Key catalysts include a gold windfall, with prices hitting 28 record highs by April, contributing 60% of Ghana’s export receipts in Q1 2025. The IMF’s $3 billion Extended Credit Facility, coupled with stringent monetary policies like a 500-basis-point rate hike to 30%, has bolstered investor confidence. Moreso, the Bank of Ghana’s gold-backed “Goldbod” initiative, mandating 20% of gold exports be purchased in Cedis, has strengthened foreign exchange reserves, now covering over four months of imports. The Cedi’s strength directly influences Ghana’s mobile money ecosystem, a cornerstone of its fintech sector, which serves over 50% of the population and processed transactions worth $150 billion in 2024. A stronger Cedi reduces the cost of imported technology infrastructure, such as servers and payment systems, enabling platforms like MTN Mobile Money and Vodafone Cash to lower operational costs. This cost reduction could translate into lower transaction fees, making digital payments more accessible and driving financial inclusion, particularly in rural areas where 4 million citizens are targeted for connectivity by 2026. However, the appreciating Cedi increases the relative cost of remittances for diaspora senders, potentially reducing inflow volumes, which accounted for 3.2% of GDP in 2024. Fintechs must adapt by offering competitive exchange rates or value-added services like micro-savings or insurance to retain users. Foreign exchange-based fintechs, such as Chipper Cash and Flutterwave, face a dual-edged sword with the Cedi’s surge. On one hand, a stronger Cedi lowers the cost of cross-border transactions for Ghanaian users, making FX fintechs more competitive against traditional banks. For instance, importing goods or services priced in USD becomes cheaper, encouraging businesses to adopt fintech solutions for international payments. On the other hand, the appreciating Cedi reduces profit margins for fintechs that thrive on currency volatility, as weaker exchange rate fluctuations limit arbitrage opportunities. To counter this, FX fintechs can leverage Ghana’s improved credit rating (S&P Global’s CCC+ in May 2025) to attract international partnerships, offering hedging tools or multi-currency wallets to mitigate risks for businesses. The Cedi’s surge enhances Ghana’s appeal to international investors, particularly in fintech, where the International Finance Corporation (IFC) committed $422 million in FY24. A stable and appreciating currency signals reduced risk, encouraging foreign direct investment (FDI) in sectors like digital payments and blockchain. The Ghana Stock Exchange’s strong performance, with increased market capitalization in IT and finance sectors, reflects this confidence. For investors, Cedi-denominated assets, such as government bonds, offer attractive yields, further supported by fiscal discipline and IMF-backed reforms. The Cedi’s appreciation necessitates a recalibration of pricing and scaling strategies for fintechs. Lower import costs enable platforms to reduce service fees, potentially increasing user adoption but squeezing margins. To scale, fintechs should invest in localized solutions, such as integrating with Ghana’s centralized public-sector payment platform, Ghana.gov.gh, to tap into government-driven digitalization. Exporters, facing higher costs due to a stronger Cedi, may demand fintechs offer hedging or trade finance tools to maintain competitiveness. Moreso, the appreciating Cedi enhances the purchasing power of Ghanaian consumers, creating opportunities for fintechs to introduce premium services like investment apps or digital lending tailored to MSMEs. The Cedi’s 42% surge in 2025 marks a pivotal moment for Ghana’s fintech sector, offering opportunities to lower costs, attract investment, and drive innovation. Mobile money platforms can leverage reduced operational costs to enhance financial inclusion, while FX-based fintechs must innovate to maintain profitability in a low-volatility environment. International investors, buoyed by Ghana’s improved fiscal health, are likely to increase FDI, but sustained growth requires addressing risks like commodity price fluctuations and import reliance. Policymakers should prioritize export diversification and fiscal discipline to ensure the Cedi’s stability, while fintechs must align with Ghana’s digital agenda to scale effectively. The outlook is cautiously optimistic, with GITFiC projecting a 28.94% annual Cedi appreciation in 2025, provided reforms continue. Ghana’s fintech playbook is being rewritten—those who adapt will shape its future.

johneb492254456

Your Next Competitor Might Not Be a Country — It Might Be an API

June 14, 2025 by johneb492254456 In a world where borders once defined competition, digital platforms powered by APIs are rewriting the rules, dissolving geographic barriers faster than any trade deal. From e-commerce to finance, APIs enable seamless, scalable, and instant global reach, pitting startups against giants and algorithms against nations. This week’s StayWired discussion explores how APIs are reshaping markets, empowering borderless businesses, and redefining who or what your next competitor might be, with a deep dive into their impact on global commerce. APIs, or Application Programming Interfaces, are the invisible engines of the digital economy, allowing systems to connect and share data effortlessly. In 2024, the global API management market hit $5.5 billion, growing 25% year-over-year, per Gartner, as businesses from London to Lagos leverage APIs to expand. Stripe’s payment API, for instance, powers 1.5 million businesses across 195 countries, enabling a Kenyan retailer to process payments as easily as a U.S. giant, according to Stripe’s 2024 report. This democratization erodes the advantage of proximity, making competition a matter of code, not borders. Digital platforms built on APIs are outpacing traditional trade agreements in opening markets. While the USMCA took years to negotiate, platforms like Shopify, using APIs to integrate logistics and payments, helped 2 million merchants generate $600 billion in global sales in 2024, per Shopify’s annual data. Small businesses in Vietnam now sell to U.S. consumers without navigating customs red tape, as APIs handle taxes and shipping in real-time. The World Trade Organization notes that digital trade grew 30% faster than physical trade from 2020 to 2024, fueled by API-driven ecosystems. The competitive edge of APIs lies in their ability to scale and innovate rapidly. Amazon’s AWS APIs, for example, enable developers to build apps globally with minimal infrastructure, supporting 190 countries and generating $100 billion in revenue in 2024, per Amazon’s earnings. In contrast, traditional firms tied to physical supply chains face delays and costs—McKinsey estimates that API-integrated firms cut go-to-market times by 40%. In India, UPI’s API ecosystem processed $2.4 trillion in transactions in 2024, per NPCI, letting fintechs like PhonePe compete with global banks without branches. Industries are transforming under API-driven competition. In retail, platforms like Shein use APIs to optimize supply chains, cutting delivery times by 50% and capturing 20% of the U.S. fast-fashion market in 2024, per Statista. In finance, Plaid’s APIs connect 7,000 apps to bank accounts, enabling fintechs to challenge traditional lenders, with $1.2 trillion in linked assets, per Plaid’s 2024 data. Even healthcare sees disruption—Google’s Health API powers 500,000 telehealth sessions monthly, per Google Cloud, bypassing regional providers. No sector is immune when APIs erase geographic constraints. Your next competitor might not be a country but an API, enabling a startup in Singapore to outmaneuver a corporation in Chicago. APIs have fueled a $5.5 billion market, slashed market entry barriers, and driven digital trade to outpace physical goods. Yet, cybersecurity, privacy, and access gaps demand vigilance. The future belongs to those who harness APIs to innovate, not just compete. Insight: A 2025 BCG report predicts API-driven firms will capture 30% of global trade value by 2030, signaling a world where code, not borders, defines winners.

johneb492254456

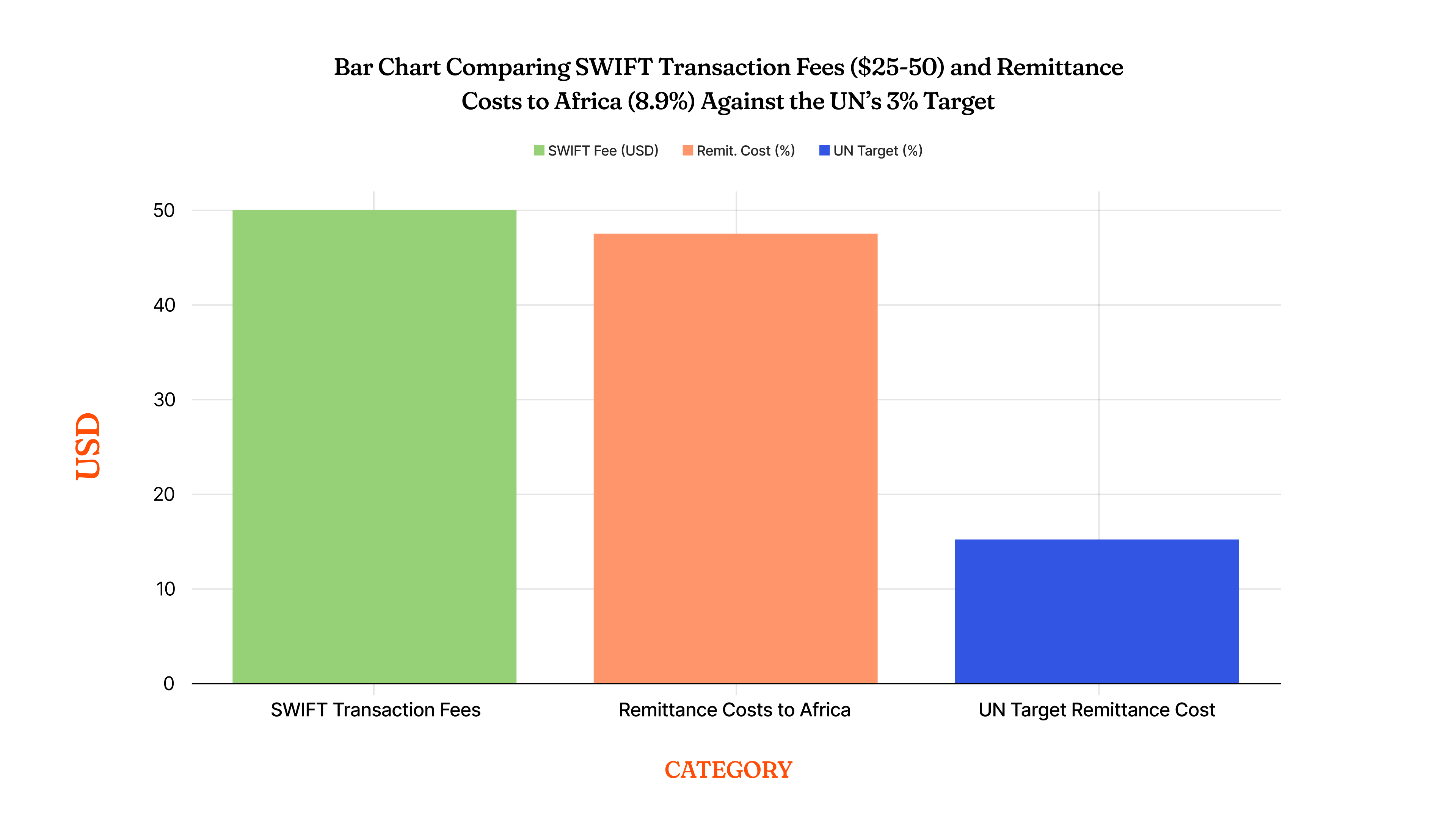

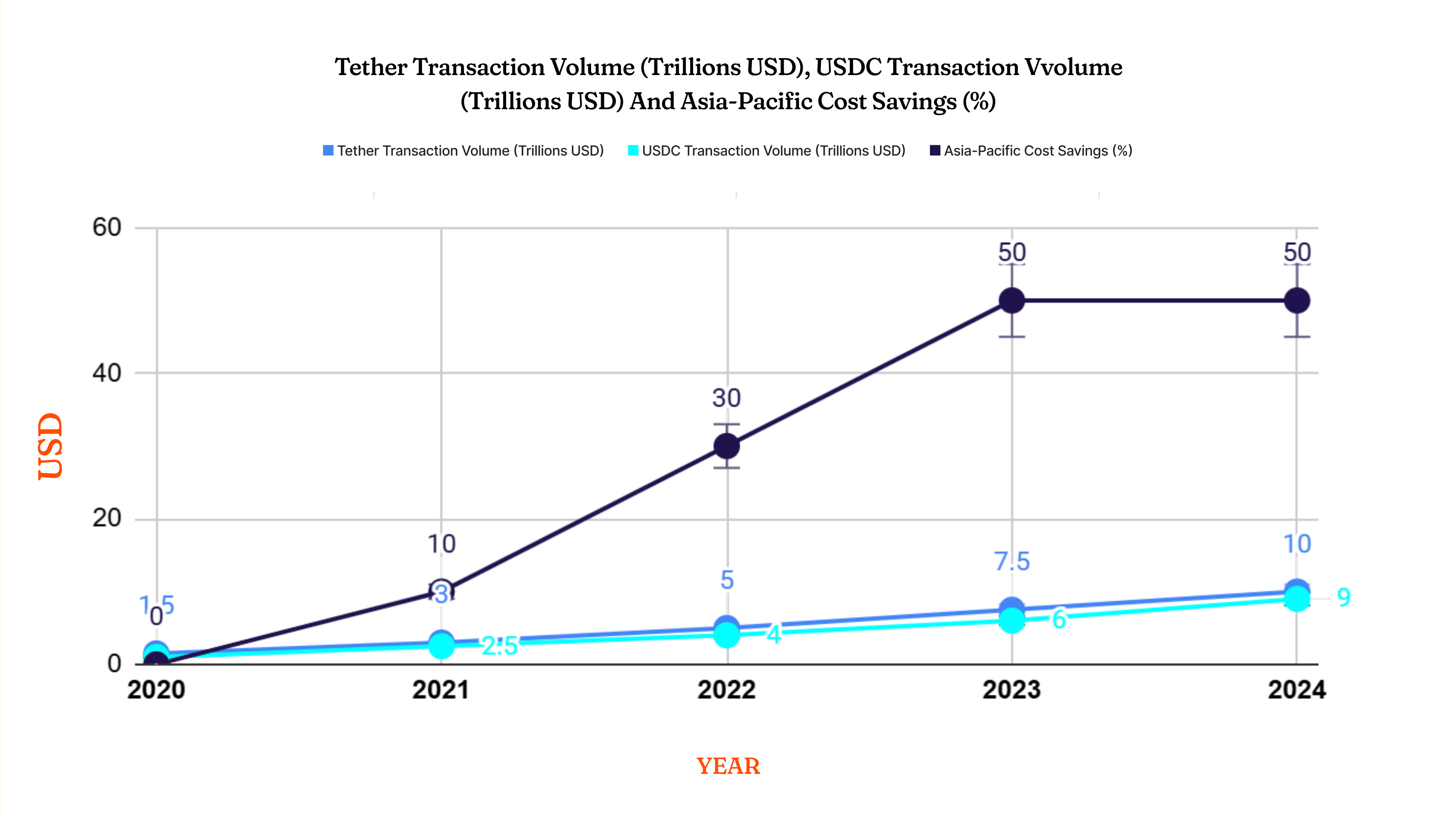

From SWIFT to Stablecoins: Are Banks Still Relevant in Cross-Border Trade?

June 10, 2025 by johneb492254456 Cross-border trade is undergoing a seismic shift as blockchain-powered solutions like stablecoins promise instant, borderless transfers, challenging the traditional role of correspondent banks. For decades, the SWIFT network has been the backbone of international payments, but high costs, slow processing, and inefficiencies have opened the door to innovation. This week’s StayWired discussion explores whether banks remain vital in global commerce or if decentralized technologies are poised to render them obsolete, diving into costs, speed, and the evolving financial landscape. The SWIFT system, launched in 1973, connects over 11,000 financial institutions across 200 countries, handling $150 trillion in annual cross-border payments, according to SWIFT’s 2024 report. However, transactions often take 1-5 days, with fees averaging $25-$50 per transfer, per the World Bank’s 2023 data. Correspondent banks, acting as intermediaries, add layers of cost and delay, with smaller businesses in emerging markets hit hardest. A 2024 IMF study notes that remittance costs to Africa average 8.9%, far above the UN’s 3% target, exposing SWIFT’s limitations in a fast-moving world. Enter stablecoins, digital currencies pegged to assets like the U.S. dollar, offering a compelling alternative. Tether (USDT) and USD Coin (USDC) processed $10 trillion in transactions in 2024, per CoinGecko, with near-instant settlements at fees often below $1. Blockchain’s transparency cuts out middlemen, enabling peer-to-peer transfers across borders. A 2023 Ripple survey found that 70% of Asia-Pacific firms using stablecoins for trade payments saw cost reductions of 50% or more, hinting at a revolution for exporters in places like Singapore and Thailand. Banks, however, aren’t standing still. Major players like JPMorgan have launched JPM Coin, facilitating instant cross-border settlements, with $1 billion in daily transactions by 2024, per the bank’s annual report. The Bank for International Settlements’ 2024 mBridge project, a blockchain platform linking central banks, processed $22 million in test trades across four countries, showing banks can adapt. They also offer trust to FDIC insurance and regulatory oversight give comfort that stablecoins, often issued by private firms, can’t match, especially after 2022’s TerraUSD collapse wiped out $40 billion, per Chainalysis. Speed and cost favor stablecoins, but risks loom large. The Financial Stability Board’s 2024 report warns of stablecoin volatility if reserves aren’t fully backed, with 10% of audited coins showing discrepancies. Regulatory gaps persist; only 25% of jurisdictions have comprehensive crypto laws, per the OECD, leaving cross-border trade exposed to fraud and money laundering. Banks, by contrast, comply with strict AML and KYC rules, with the Basel Committee noting a 98% compliance rate among global banks in 2023, a safeguard blockchain struggles to replicate. Emerging markets highlight the stakes. In Latin America, where 60% of cross-border trade relies on U.S. dollar payments, stablecoins cut costs for small firms, with a 2024 Inter-American Development Bank study showing a 40% drop in transfer fees for Brazilian exporters. Yet, banks remain critical for credit—trade finance, like letters of credit, backed $5.2 trillion in global trade in 2023, per the ICC, a service stablecoins can’t yet scale. Without bank intermediation, smaller players risk exclusion from complex deals, especially in Africa and Asia. Are banks still relevant? Stablecoins win on speed and cost, slashing fees and delays for cross-border trade, with volumes soaring past $10 trillion in 2024. But banks bring stability, credit, and regulatory trust—vital for large-scale commerce and risk-averse players. The future likely blends both: banks adopting blockchain to stay competitive, while stablecoins mature under tighter rules. Insight: A 2025 McKinsey report predicts hybrid systems could handle 20% of global trade payments by 2030, suggesting banks and stablecoins will coexist, reshaping commerce together.

johneb492254456

A WeWire Report: Behind the Ghana Cedi’s 2025 Rally - Key Drivers and Outlook

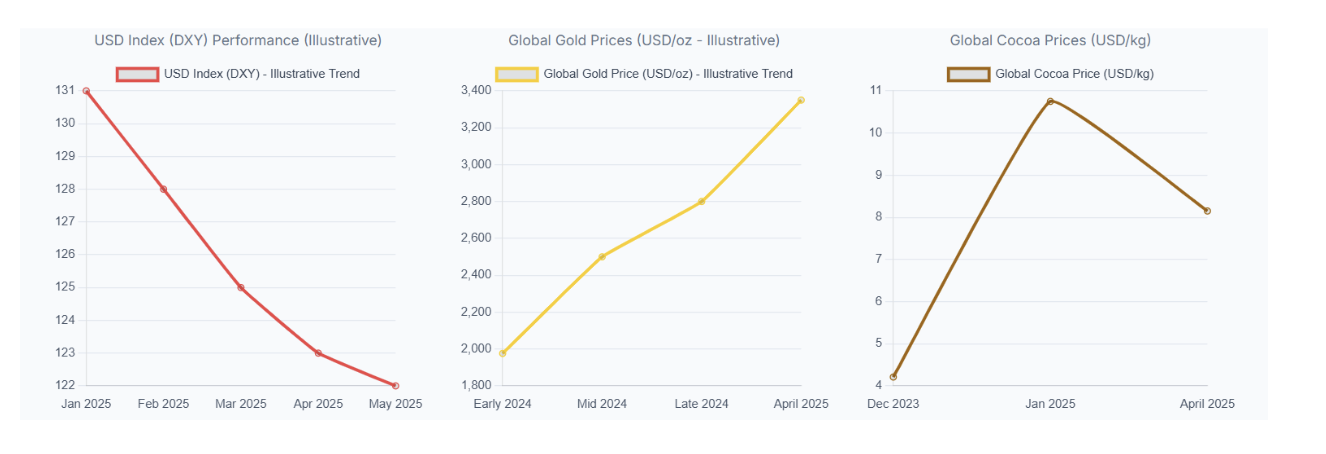

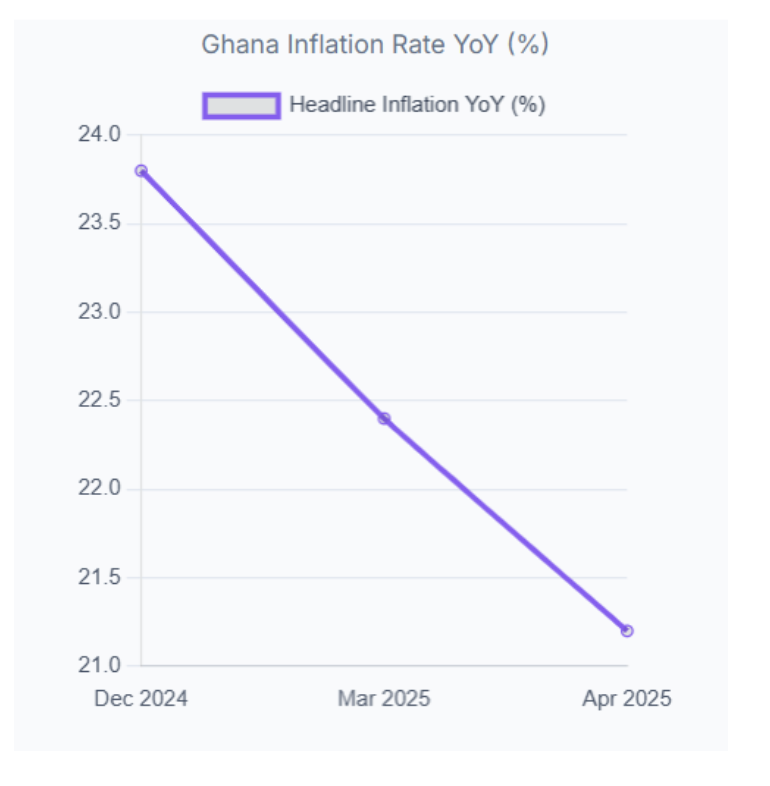

June 5, 2025 by johneb492254456 The Ghana Cedi has demonstrated a remarkable turnaround over the past six weeks, appreciating sharply against the U.S. dollar on the official market. This significant strengthening is exemplified by the interbank cedi briefly breaking GHS 10.25 per USD by late May 2025, a notable improvement from approximately GHS 13.15 per USD just a week prior. This represents a substantial reversal from the currency’s performance in 2024, when it depreciated by 28% against the US dollar, and its plunge past ₵15 per USD in late 2023 and early 2024 amidst severe economic strain. By May 21, 2025, the cedi had appreciated by 24.1 percent against the US dollar year-to-date. This WeWire report delves into the multifaceted reasons behind the cedi’s strengthening, examining the key macroeconomic drivers, the supportive policy measures implemented by Ghana’s authorities, and the broader economic trajectory. It will also critically assess the sustainability of this trend, drawing on recent data and expert perspectives to provide a forward-looking outlook. The dramatic reversal from severe depreciation to strong appreciation, especially after a period of sovereign debt challenges, signals a profound shift in how both domestic and international markets perceive Ghana’s economic health and the effectiveness of its policy responses. It suggests that economic agents are now more confident in the country’s recovery path and policy direction, indicating a robust underlying shift in economic perception. The recent resurgence of the Ghana Cedi is primarily underpinned by a significant improvement in the nation’s external accounts, driven by robust performance in its key export sectors and sustained foreign currency inflows. Ghana, a prominent gold producer in Africa, has experienced a historic surge in gold exports. Gold shipments reached approximately US$11.6 billion in 2024, marking a substantial 53% jump from 2023 and accounting for roughly 57% of total exports according to the Bank of Ghana Report. This robust performance continued into 2025, with gold exports surging to US$2.7 billion in the first four months of 2025 (January to April), a significant increase from $670.5 million in the same period of 2023 and $862.4 million in 2024. Specifically, the first quarter of 2025 alone saw gold export earnings of around US$1.83 billion. This boom is attributable to both buoyant production, with small-scale mining contributing over 40% of the estimated 151 tonnes in 2024 (versus ~120t in 2023), and record global gold prices, which broke US$3,300 per ounce in April 2025. Research from JPMorgan indicates that the gold sector alone contributed a substantial 60% of Ghana’s export receipts in Q1 2025. Ghana’s cocoa sector has also made significant contributions to the country’s foreign exchange inflows. Cocoa export revenues for the first four months of 2025 reached an impressive $1.84 billion, more than triple the $579 million recorded during the same period in 2024. This four-month total remarkably exceeds Ghana’s entire cocoa earnings for the first eleven months of 2024. The surge is multifaceted, driven by improved farmgate prices reducing smuggling, a clampdown on illegal mining (galamsey) preserving cocoa farms, and a notable shift in Ghana’s sales strategy. Ghana historically traded cocoa via the futures market, pricing beans based on previous years’ averages, which meant it missed out on global cocoa price surges in 2024. However, in 2025, due to difficulties in securing traditional syndicated loans for forward buying, Ghana has become more active in the spot market, enabling it to capitalize on the current high global cocoa prices. This forced shift allowed Ghana to sell cocoa at current, significantly higher spot prices, directly leading to a tripling of export earnings. This demonstrates a flexible, market-responsive approach to revenue generation under duress, though it also exposes Ghana to greater immediate downside risk if global cocoa prices were to fall sharply. Cocoa production for the 2024/2025 market year is projected to climb to 700,000 metric tons (MT), a 32% increase over the previous year’s estimate. These combined surges in gold and cocoa export receipts have led to a substantial increase in Ghana’s foreign currency earnings, directly boosting the supply of dollars in the domestic market and easing pressure on the Cedi. The following table provides a quantitative comparison of Ghana’s key export earnings: The appreciation of the Ghana Cedi is not solely due to internal production increases but is significantly amplified by a complex global interplay, particularly concerning the U.S. dollar and gold prices. Historically, there has been an inverse relationship between gold prices and the U.S. dollar’s strength: when the dollar strengthens, gold typically weakens because it becomes more expensive for holders of other currencies, and dollar-denominated assets offer more attractive yields. However, late 2023 and early 2024 witnessed an unusual phenomenon where both gold and the dollar demonstrated significant strength simultaneously. This was influenced by factors such as geopolitical tensions, increased central bank gold purchases (as a diversification away from dollar-denominated assets), and persistent inflation concerns. A key driver for gold’s appeal was the market’s anticipation of the Federal Reserve signaling interest rate cuts while inflation remained above target. This scenario leads to lower real interest rates, reducing the opportunity cost of holding non-yielding assets like gold. Crucially for Ghana, the US Dollar Index (DXY) has fallen by approximately 7% since the beginning of 2025. This weakening of the USD in early 2025 directly contributed to the surge in global gold prices, which surpassed US$3,300 per ounce in April 2025. This global dynamic has significantly amplified Ghana’s gold export revenues, providing a substantial foreign exchange windfall. Ghana is thus a direct beneficiary of these global macroeconomic and geopolitical trends. While its increased gold production is a domestic factor, a substantial portion of the export windfall (and thus the Cedi’s strength) is externally driven. This implies that the Cedi’s stability is partially contingent on these global factors remaining favorable, making it susceptible to shifts in international monetary policy, inflation outlooks, and geopolitical risk sentiment. The following charts illustrate the performance of the US Dollar Index and global gold prices: Chart: US Dollar Index (DXY) Performance (Q1 2025 – May 2025) Balance of Payments & Reserves Ghana’s improved external accounts are evident in a record provisional current account surplus of US$2.1 billion in the first quarter of 2025. This surplus was primarily “driven mainly by higher prices and increased production volumes of gold and cocoa, and strong remittance inflows”. The strong current account performance, even with net outflows in the capital and financial account, resulted in an overall Balance of Payments surplus of US$1.1 billion. This robust external performance has translated into significant reserve accumulation. Gross International Reserves (GIR) climbed from approximately US$6.0 billion in early 2024 to nearly US$10.7 billion by April 2025. This level is equivalent to 4.7 months of import cover, a substantial improvement from about 2.7 months in early 2024. The Bank of Ghana explicitly states that this reserve accumulation is “largely from domestic sources”, implying that the Cedi’s strength is genuinely market-driven and not a result of depleting reserves to prop up the currency. The significant increase in Ghana’s import cover provides a crucial buffer against external shocks, signaling enhanced economic resilience and effectively reducing speculative pressure on the Cedi by reassuring markets of ample foreign exchange liquidity. A robust reserve position instills confidence among investors and market participants, signaling that the central bank possesses sufficient foreign exchange resources to manage potential demand-supply imbalances in the currency market, thereby discouraging speculative attacks against the Cedi. This reduces the perceived risk of currency depreciation and contributes directly to the Cedi’s stability and appreciation. The following chart illustrates the trend in Ghana’s Gross International Reserves and import cover: Beyond favorable macroeconomic trends, Ghana’s authorities have implemented a series of decisive policy measures that have been instrumental in supporting the Cedi’s appreciation and ensuring macroeconomic stability. The Bank of Ghana (BoG) has consistently maintained a hawkish monetary policy stance. The Monetary Policy Rate (MPR) was held at 28.0% in May 2025 by a unanimous decision, following a 100 basis points hike to 28% on March 28th, 2025, after three consecutive meetings with no changes. This tight policy stance, coupled with stepped-up liquidity sterilization efforts, has been explicitly credited by BoG Governor Johnson Asiama for the Cedi’s recent rebound and for its role in bringing down inflation. Headline inflation has declined consecutively for four months, reaching 21.2% in April 2025, a significant drop from 23.8% in December 2024. Both food inflation (25.0% in April) and non-food inflation (17.9% in April) have eased. The Ghana Reference Rate, which serves as the base lending rate, has eased substantially to 23.9% in April 2025 from 29.3% in December 2024, signaling improvements in credit conditions and potentially boosting real sector activities. Despite these positive developments, the BoG acknowledges that the current inflation level remains high relative to its medium-term target of 6%-10%, necessitating a continued tight stance to reinforce the disinflation process. Inflation is now expected to ease faster towards the medium-term target, potentially by Q1 2026, barring unanticipated shocks. The Bank of Ghana’s decision to maintain a high Monetary Policy Rate (MPR) at 28.0% despite a consecutive decline in headline inflation demonstrates a robust commitment to anchoring disinflation and reinforcing exchange rate stability, prioritizing long-term price stability over immediate growth stimulation. This continued hawkish stance, even as inflation shows signs of easing, indicates a strong resolve to fully achieve its inflation target and solidify the Cedi’s gains. This signals to the market that the central bank is not prematurely easing policy and is committed to breaking inflationary inertia, even if it means potentially moderating short-term economic growth. This proactive approach enhances the BoG’s credibility and reinforces market confidence in the Cedi’s stability. The following chart illustrates the trend in Ghana’s inflation rate: Chart: Ghana Inflation Rate (YoY) (Historical Trend) The government’s budget performance has shown improvement, with fiscal policy implementation broadly aligned with the 2025 Budget. Provisional data for Q1 2025 indicated a primary surplus on a commitment basis, a significant step towards fiscal consolidation. Revenue shortfalls were effectively offset by spending cuts and expenditure rationalization, contributing to closing the deficit and signaling fiscal discipline to financial markets. The Cedi’s appreciation has had a profound positive effect on Ghana’s fiscal health. President John Mahama announced that the Cedi’s strength had already reduced Ghana’s foreign-currency debt by nearly ₵150 billion over the past five months. This has created much-needed fiscal breathing room, potentially allowing Ghana to achieve its target of a 55–58% debt-to-GDP ratio by year-end, well ahead of the original 2028 deadline. Public debt, using the revised GDP series, fell from approximately 69% of GDP in early 2024 to roughly 55% by early 2025. The Cedi’s appreciation is creating a powerful virtuous cycle for Ghana’s fiscal health by significantly reducing the local currency cost of its substantial external debt, thereby freeing up critical fiscal space that can be strategically redirected towards growth-enhancing projects. The newly created fiscal space allows the government to reallocate funds (potentially up to 15% of previous debt-service outlays) towards crucial capital projects such as infrastructure, healthcare, and education. This redirection of resources can stimulate real economic growth, create jobs, and improve public services, thereby further strengthening the Cedi’s long-term fundamentals and fostering a positive feedback loop between currency stability and economic development. The government has renewed its commitment to the IMF’s Extended Credit Facility (ECF) program, which is crucial for continued support and external confidence. The Bank of Ghana has actively enforced foreign exchange rules, monitoring interbank and bureaux-de-change operations. Initiatives like the relaunched Gold Purchase Programme and a new gold-backed bond aim to ensure export proceeds enter the official market. Importantly, reserves have grown, implying the Cedi’s strength is market-driven, not due to reserve depletion (though BoG did support the FX market with US$264.4M in March 2025 to preserve stability). The sustainability of the Cedi’s recent gains is a subject of ongoing analysis, with arguments for both persistence and potential headwinds. Fundamental economic improvements strongly suggest that the Cedi’s positive trend may persist. The underlying enhancements in Ghana’s external accounts, driven by record gold and cocoa exports and robust remittance inflows, continue to facilitate the accumulation of international reserves. This has led to a substantial increase in import cover, providing a crucial buffer against external shocks. Policy consistency further supports this outlook. Both fiscal and monetary policies remain tight and disciplined. The Bank of Ghana maintains its hawkish stance, and its latest forecast points to inflation returning faster to target (by Q1 2026) if these policies hold. The government’s renewed commitment to fiscal consolidation under the IMF program is also a positive sign, providing a framework for continued stability and external support. Investor confidence appears to be growing following last year’s crisis. S&P Global Ratings recently raised Ghana’s foreign currency sovereign credit ratings to ‘CCC+/C’ from ‘SD/SD’ in May 2025, with a stable outlook, citing improving external metrics and resilient economic growth. The IMF has also reached staff-level agreements on reviews of its Extended Credit Facility, signaling continued international backing. Furthermore, Ghana could see an additional surge in remittances if the proposed U.S. 5% remittance tax prompts Ghanaian migrants to send funds home before it takes effect, providing a temporary boost to inflows. Despite the positive momentum, several risks and headwinds could challenge the Cedi’s rally. Economists, such as Lord Mensah, caution that the recent Cedi strength “is not going to run forever” without sustained growth in Ghana’s “real sectors” (e.g., agriculture, manufacturing, and diversified services). A significant portion of the appreciation so far reflects financial inflows and past policy tightening, rather than broad-based productive expansion. This observation highlights that while Ghana’s immediate currency strength is largely driven by robust financial inflows (commodity exports, remittances) and tight policy, its long-term sustainability is critically dependent on translating these financial gains into tangible, diversified real sector growth. Without this, the Cedi’s rally risks becoming a reprieve, potentially exposing Ghana to “Dutch Disease” effects, where a booming commodity sector makes other export sectors less competitive due to a strong currency, hindering long-term economic diversification and creating vulnerability to commodity price downturns. Commodity price volatility also poses a risk. While currently favorable, global prices for gold and cocoa are subject to fluctuations. If these prices fall significantly, or if Ghana’s oil output faces maintenance shutdowns in Q3, the Cedi could weaken. Cocoa prices, for instance, have already retreated slightly in May 2025 after peaking earlier in the year. Fiscal spending pressures remain a concern. Although the 2025 budget aims for strict expenditure control and a primary surplus, expenditure pressure is likely to persist due to factors such as high inflation, potential public discontent with public financial management, and the inherent risks this poses to economic growth. Historically, Ghana’s expenditure has grown substantially (28% annually over the past 25 years). There are also indications that many firms priced goods in Cedi at earlier, higher exchange rates, meaning consumer prices may not yet fully reflect the stronger currency. While inflation is declining, it remains elevated at 21.2% in April 2025, still significantly above the Bank of Ghana’s target range. Furthermore, while the banking sector has shown resilience, asset quality remains a concern, with the non-performing loan (NPL) ratio climbing to 21.8% by year-end 2024 from 20.6% a year prior. Recapitalization measures are still required for some banks to ensure continued resilience. External headwinds also persist. Global economic developments continue to present challenges, including low growth prospects, unsynchronized disinflation outcomes, and restrictive global financial conditions, partly driven by trade policy shifts in the United States. The World Bank also cautions about downside risks such as a sharper-than-expected slowdown in China, escalating geopolitical tensions (particularly in the Middle East), and prolonged elevated global interest rates. The Ghana Cedi is likely to remain relatively strong and stable in the near term, specifically over the next month to the next quarter. The momentum from continued high global commodity prices (especially gold, buoyed by global uncertainties and ongoing central bank demand for diversification), sustained robust remittance inflows, and the Bank of Ghana’s unwavering commitment to its tight monetary policy stance will provide significant and credible support. The ongoing adherence to the IMF program and the recent sovereign credit rating upgrade by S&P Global Ratings will further bolster investor confidence. The central bank’s ample reserve buffers (US$10.7 billion, equivalent to 4.7 months of import cover) provide a strong and credible defense against any immediate speculative pressures or short-term external shocks. While the broad appreciating trend is expected to persist, minor fluctuations are possible. These could arise from short-term shifts in global commodity prices (e.g., the recent retreat in cocoa prices 1), or any perceived softening in the government’s fiscal discipline. However, given the current policy resolve and the fundamental improvements in the external sector, these are unlikely to trigger a sharp or sustained reversal in the immediate horizon. The trajectory of global gold and cocoa prices, the actual implementation and market reaction to the proposed U.S. remittance tax, and the Ghanaian government’s continued strict adherence to its fiscal consolidation plan will be crucial determinants of the Cedi’s path. The pace of inflation decline and the Bank of Ghana’s corresponding policy responses will also be closely watched. As highlighted by economists, the longer-term sustainability of the Cedi’s strength beyond the next quarter will increasingly depend on Ghana’s ability to translate these substantial financial inflows into diversified real economic growth, moving beyond an over-reliance on commodity windfalls. The current rally presents a valuable window of opportunity for targeted investments in non-commodity sectors to ensure a more resilient and sustainable foundation for the Cedi’s value in the long run.

johneb492254456

Macroeconomic Drivers of the Cedi’s Strength

Exports & Commodity Inflows

Export Commodity

Period (Jan-Apr 2023)

Period (Jan-Apr 2024)

Period (Jan-Apr 2025)

Q1 2025 (Jan-Mar)

Gold Exports

US$670.5 million

US$862.4 million

US$2.7 billion

US$1.83 billion

Cocoa Exports

N/A

US$579 million

US$1.84 billion

N/A

Global Context: The US Dollar and Gold Prices

Policy and Central Bank Actions

Policy and Central Bank ActionsTight Monetary Policy (Ghana)

Fiscal Discipline

Central Bank Interventions

Will the Cedi’s Rally Continue?

Arguments for Persistence

Risks and Headwinds

Forecast/Conclusion