An Analysis of Why Africa’s Top Export Commodities Are Failing to Translate into Currency Stability

September 1, 2025 by johneb492254456 Africa sits atop a mountain of global treasures. Nigeria pumps millions of barrels of oil, Ghana supplies the world’s cocoa and gold, South Africa dominates platinum markets, and Zimbabwe is rising fast in lithium production. In theory, these riches should anchor robust currencies and shield economies from volatility. In reality, the opposite often happens: while global commodity prices surge, African currencies tumble. In 2024–2025, the paradox played out vividly. Oil prices rose sharply, cocoa futures hit multi-decade highs, and gold climbed above $2,000 per ounce. Yet the Nigerian naira lost more than half its value, Ghana’s cedi plunged, and Zimbabwe’s new gold-backed ZiG currency depreciated within months. The disconnect raises a sobering question: Why do Africa’s top export commodities fail to translate into currency stability? This article unpacks the structural factors behind the paradox. From the dominance of raw commodity exports and import dependency to fragile foreign-exchange reserves and fiscal mismanagement, the roots run deep. By exploring examples across Nigeria, Ghana, South Africa, and Zimbabwe, we reveal why commodity wealth often becomes a burden instead of a shield and what must change for Africa’s currencies to finally find stability. Africa is a major supplier of global commodities – from Nigeria’s oil to Ghana’s cocoa and gold, South Africa’s platinum and gold, to Zimbabwe’s lithium – yet these riches seldom anchor stable currencies. In 2024, world oil prices jumped and cocoa futures hit multi-year highs, but Nigeria’s naira and Ghana’s cedi continued to weaken. For example, Ghana saw gold prices rise 23% and cocoa 45% in 2024, yet its currency slid about 27% through late 2024 (before recovering slightly in 2025). Likewise, Nigeria’s naira fell roughly 70% against the US dollar in 2024 despite being one of the world’s top oil exporters (Nigeria produces about 2.7% of global oil supply). South Africa is the world’s leading platinum exporter (≈28.5% of global supply), but its rand remains vulnerable to global swings. This paradox – booming commodity prices yet unstable local money – stems from deep structural factors. Understanding this puzzle requires looking beneath commodity prices. African exports are overwhelmingly “raw”: oil, minerals, and cash crops with little value-added. These products are highly volatile – a 30–50% swing in oil or cocoa prices within months is not unusual. When prices surge, export revenues jump, but they can just as quickly evaporate with a downturn. Moreover, most African countries import large volumes of goods (staple foods, fuel, machinery) priced in dollars. In the latest shocks (COVID-19 and the Ukraine war), higher global energy and food prices have increased import bills, even as commodity exporters earned more for their exports. In practice, oil-rich Nigeria still imports refined fuel, and grain-importing Ghana has thin buffers. This import dependency means that windfalls outflows often offset windfalls from exports. In short, currencies have to weaken to pay for essential imports – a classic symptom of the “resource curse.” At the same time, African countries often enter booms with fragile fiscal and reserve buffers. In many cases, commodity windfalls were spent, not saved. A decade of cheap dollars and subsidies (for fuel, electricity, or food) left countries like Nigeria and Ghana with big deficits. When prices reversed or destabilized, their foreign-exchange reserves were insufficient to smooth the shock. As the IMF notes, many central banks tried to “prop up their currencies by supplying foreign exchange from reserves,” but with reserves “running low… there is little room to continue” intervening. Indeed, half of sub-Saharan countries ran current-account deficits above 5% of GDP in 2022, straining FX reserves and weakening exchange rates. Even moderate export gains were often outpaced by surging import and debt-servicing costs. Across the region, roughly 40% of public debt is external (mostly in USD), so any currency drop suddenly inflates government debt and deficits. These general pressures help explain the commodity/currency paradox. They also show why some countries avoid the trap. Nations with credible monetary anchors have seen far more stability: for example, Botswana’s pula (pegged to a currency basket) or the CFA franc (pegged to the euro) have remained steady. As MIT analysts point out, countries with fixed or managed pegs often see lower inflation and volatility than free-floaters in Africa. In contrast, countries running large deficits and floating regimes (Nigeria, Ghana, Zambia etc.) have seen repeated crashes. Below is a summary of key exporters illustrating this pattern: Several studies and reports emphasize these factors. For example, an IMF analysis notes that “large movements in commodity prices can cause trade imbalances, in turn causing foreign exchange flows to vary”. When revenues surge, deficits often rise too (because energy subsidies and debts remain high); when revenues fall, currencies crumble. As a Bloomberg report (via IMF data) puts it, during a commodity windfall, Ghana’s economy was still “vulnerable to exchange rate volatility,” prompting policy responses like gold-hedging. In summary, Africa’s export commodities remain a double-edged sword. High prices inject dollars but also amplify existing imbalances. Without strong reserves and low deficits, windfalls get eaten up by import bills and debt, leaving local currencies exposed. As analysts conclude, commodity riches alone are not enough for currency stability – durable reforms, diversification and careful reserve management are equally essential. Only when African nations translate raw exports into productive investment and savings will their exchange rates cease to mirror every price shock.

johneb492254456

Introduction

Africa’s Commodity Wealth and Currency Woes

Put another way, when a commodity boom sends dollars into the country, much of the revenue leaks right back out as costly imports. As MIT analysts note, “most sub-Saharan African countries… are net importers,” especially of staples (rice, wheat, maize). A weaker currency immediately raises the local price of these imports, driving inflation. That inflation erodes real incomes and deters investment, undermining confidence in the currency. The IMF finds that in Africa today “weaker currencies make the fight to curb inflation harder” because “more than two-thirds of imports are priced in US dollars”. In practice, local firms and consumers see prices jumping even if commodity dollars have come in, so the political pressure is to loosen or devalue the currency further. This creates a vicious cycle: depreciation leads to inflation and deficits, which then force further depreciation (as illustrated above).

Put another way, when a commodity boom sends dollars into the country, much of the revenue leaks right back out as costly imports. As MIT analysts note, “most sub-Saharan African countries… are net importers,” especially of staples (rice, wheat, maize). A weaker currency immediately raises the local price of these imports, driving inflation. That inflation erodes real incomes and deters investment, undermining confidence in the currency. The IMF finds that in Africa today “weaker currencies make the fight to curb inflation harder” because “more than two-thirds of imports are priced in US dollars”. In practice, local firms and consumers see prices jumping even if commodity dollars have come in, so the political pressure is to loosen or devalue the currency further. This creates a vicious cycle: depreciation leads to inflation and deficits, which then force further depreciation (as illustrated above).

Country

Top Export(s)

Share of Exports (approx.)

Exchange Rate Trend (2020–25)

Nigeria

Crude Oil

≈80–90% of exports

Naira collapsed ~150–200% between 2020–24 (from ~₦360 to >₦1,600/USD). It briefly stabilized in 2025 as reforms (ending fuel subsidies, unifying FX) took hold

Ghana

Gold, Cocoa, Oil

Gold (~30–35%), cocoa & oil are significant

Cedi fell ~27% in 2024 amid political and debt crises, despite gold and cocoa price booms. A mini-resurgence came in 2025 after a stabilizing IMF program and gold-backed measures

South Africa

Platinum, Gold, Diamonds

Platinum ≈30% of the global market

Rand is volatile on global risk, but high metals prices and interest rates helped it recover in 2024–25. SA’s broader export base (manufacturing & minerals) gives it more cushion than mono-exporters.

Zimbabwe

Lithium, Gold, Diamonds

Vast lithium reserves (≃8% of world)

After years of hyperinflation, Zimbabwe introduced a new gold-backed currency (ZiG) in 2024, which still suffered a major devaluation by late 2024. Despite mining booms, chronic policy risks keep exchange rates under severe pressure.

China Built Africa’s Railways. Now It’s Rewriting Its Trade Maps

August 27, 2025 by johneb492254456 China’s extensive involvement in Africa’s infrastructure, particularly through railways and related projects under the Belt and Road Initiative, represents a calculated effort to reshape the continent’s economic landscape and direct trade patterns toward Beijing. This presentation, as part of the StayWired series, explores how these developments go beyond mere construction to create lasting dependencies that favor Chinese interests, drawing on insights from financial news, think tanks, and official reports to provide a grounded analysis for the general public. By examining historical shifts, key projects, trade transformations, and broader implications, we uncover the ways in which Africa’s connectivity is being realigned in a rapidly evolving global context. Africa’s trade networks have long been influenced by external powers, beginning with colonial-era pathways that funneled resources primarily to European markets through coastal ports and limited inland connections. In the post-independence period, these systems remained fragmented due to underinvestment and political instability, resulting in inefficient logistics that hindered intra-continental commerce and global integration. Today, China’s interventions are forging a new paradigm by establishing integrated corridors that prioritize efficiency and alignment with Beijing’s supply chains, effectively overwriting outdated maps to create hubs that enhance resource extraction and market access for Chinese goods. This transition is evident in the way modern infrastructure now links mineral-rich interiors directly to export-oriented ports, fostering a network that could dominate Africa’s economic future. Through the Belt and Road Initiative, China has financed and constructed numerous railway projects across Africa, aiming to boost connectivity and economic activity. For instance, the rehabilitation of the Tanzania-Zambia Railway, originally built in the 1970s and spanning over 1,860 kilometers, has been revitalized with recent agreements signed in 2024 to improve cargo transport for commodities like copper from Zambia to Tanzanian ports, addressing decades of deterioration that limited its capacity to just a fraction of its potential. Similarly, Angola’s Lobito-Luau Railway, rehabilitated in 2015 at a cost of $1.2 billion and stretching 1,344 kilometers, connects key mining regions to Atlantic ports, facilitating faster export of minerals and reducing reliance on road transport. In Zimbabwe, a $533 million deal in 2024 with Chinese firms targets the upgrade of colonial-era tracks to support coal exports, while ambitious plans for a 3,400-kilometer mega-rail linking Sudan to Chad across the Sahara promise to transform freight movement among multiple landlocked nations. These efforts, often funded by Chinese loans and executed by state-linked companies, exemplify how Beijing is embedding its influence into Africa’s physical and economic framework. By integrating railways with ports and logistics hubs, China is systematically altering Africa’s economic geography to create streamlined pathways that direct trade flows toward its own markets and financing ecosystems. This redesign manifests in enhanced supply chains where African raw materials, such as minerals and agricultural products, are more efficiently routed to Chinese buyers, while imports of manufactured goods from China become more accessible via these corridors. Reports indicate that such infrastructure has contributed to a surge in bilateral trade, with China’s commerce with Belt and Road countries reaching $1.34 trillion in 2019, growing 7.4 percent faster than with non-participating nations, largely driven by exports of construction materials and machinery. The economic ramifications of China’s railway push extend to creating dependencies that streamline African exports toward Beijing, as evidenced by China’s status as the continent’s largest trading partner, with bilateral trade expanding fourfold in recent decades according to think tank analyses. This alignment is supported by data showing that Chinese investments in infrastructure have driven exports of equipment and standards, such as in hydropower-linked projects that boosted machinery shipments worth hundreds of millions, fostering a cycle where African economies become intertwined with Chinese supply networks. Consequently, countries benefit from improved connectivity that reduces transport times and costs, yet they also face heightened reliance on Chinese markets for their commodities, with trade imbalances favoring Beijing’s imports over balanced exchanges. Insights from official reports reveal that this has accelerated economic growth in some regions but raised concerns over debt sustainability, as loans for these projects often tie repayments to resource concessions. Reflecting on these developments, China’s railway initiatives offer valuable lessons in rapid infrastructure deployment but also reveal challenges like opaque lending practices and environmental concerns that could undermine long-term sustainability. Moving forward, African nations may seek diversified partnerships to balance dependencies, while global stakeholders like the United States respond with alternatives such as the Partnership for Global Infrastructure and Investment to counter Beijing’s influence. Data from recent forums suggest that while trade ties continue to deepen, with China pledging further investments in 2024, the evolving landscape demands vigilant oversight to ensure equitable benefits. Ultimately, this rewriting of trade maps could propel Africa’s integration into the global economy, provided it navigates the risks of over-reliance on a single partner. Here, insert a pie chart breaking down Africa’s debt holders by creditor type, based on IMF and World Bank figures, to emphasize China’s prominent role.

johneb492254456

Politically, nations entangled in Chinese-financed railways often find themselves indebted, leading to reliance on Beijing’s ongoing support for maintenance and expansions, which can influence domestic policies and international alignments. Geopolitically, this infrastructure dominance risks marginalizing other players, as China’s control over key arteries could sideline initiatives from the European Union or India, while enhancing Beijing’s strategic footing in resource-rich areas. For example, debt distress in several African countries, with seven deemed at risk by the World Bank in 2020 due to Chinese loans, underscores how financial obligations can translate into political leverage, prompting renegotiations that favor Beijing.

Politically, nations entangled in Chinese-financed railways often find themselves indebted, leading to reliance on Beijing’s ongoing support for maintenance and expansions, which can influence domestic policies and international alignments. Geopolitically, this infrastructure dominance risks marginalizing other players, as China’s control over key arteries could sideline initiatives from the European Union or India, while enhancing Beijing’s strategic footing in resource-rich areas. For example, debt distress in several African countries, with seven deemed at risk by the World Bank in 2020 due to Chinese loans, underscores how financial obligations can translate into political leverage, prompting renegotiations that favor Beijing.

Meet the Unofficial Central Bank of WhatsApp: West Africa’s Newest FX Market Maker

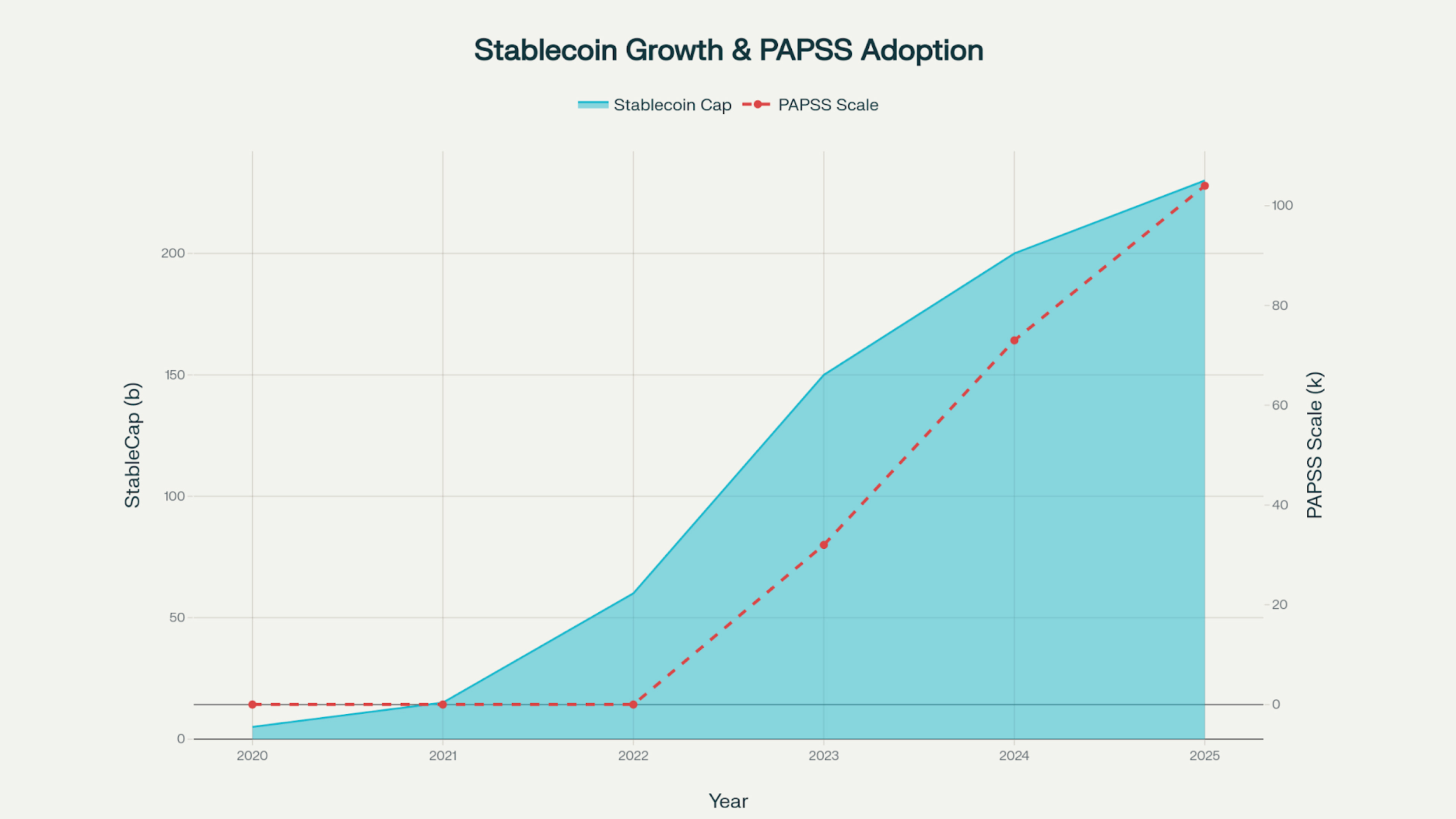

August 20, 2025 by johneb492254456 In recent years, informal peer-to-peer (P2P) foreign exchange networks operating via WhatsApp, Telegram, and Binance P2P have increasingly supplanted official banking channels in African retail and SME-level currency trades. Dense, trust-based local networks now often handle more USDT liquidity daily than traditional central bank mechanisms. These networks set prices, manage access, and respond swiftly to shocks playing the role of a market maker much like a central bank, but entirely outside official channels. Across cities like Lagos, Nairobi, and Accra, top-tier WhatsApp-based vendors now coordinate trades worth millions of dollars in USDT for local currencies weekly. They determine spreads, ration dollar liquidity, and can shift exchange rates within hours of policy announcements or economic shocks. Meanwhile, across Sub-Saharan Africa, cryptocurrency adoption surged over 45 % year-on-year between 2022–2023 and 2023–2024, with Nigeria alone accounting for approximately 40 % of regional stablecoin inflows underscoring how critical these informal networks have become. WhatsApp thrives because of its near-ubiquitous smartphone penetration in Nigeria and wider West Africa. Users trust these FX vendors due to personal referrals, community reputation, and reliability even when formal KYC or regulatory oversight is absent. Trust, not formal credentials, drives adoption. Central banks routinely deploy billions of dollars to defend their national currencies. Yet, a single well-connected WhatsApp vendor, leveraging a network of thousands of contacts, can effectively shift “street” exchange rates more swiftly than official channels. As regulated FX markets shrink, these informal networks scale globally, eroding policy efficacy and challenging monetary sovereignty. As significant FX volume shifts into decentralized, informal liquidity hubs, central banks risk losing control over key monetary tools such as exchange rate and open market operations. Consequently, inflation targeting and currency stability become harder to enforce. For SMEs, however, these P2P “WhatsApp central banks” are often the only accessible providers of dollar liquidity, highlighting the dual nature of this phenomenon. Addressing the structural gaps in FX access, the Pan-African Payments and Settlement System (PAPSS) is gearing up to launch the “Africa Currency Marketplace” in 2025. Supported by 15 central banks, the platform will enable direct currency swaps across borders allowing users in Nigeria to match naira to someone needing birr in Ethiopia, for instance without recourse to the US dollar. Meanwhile, stablecoins like USDT and USDC are gaining traction, offering Africans a stable hedge against inflation and FX shortages. This innovation provides real-world utility beyond crypto trading serving as value storage, hedging tools, and cross-border transaction mediums. Informal FX networks facilitated via WhatsApp and stablecoins are rapidly displacing official market-making channels, especially in regions with shallow local currency liquidity. While these decentralized hubs empower SMEs and bridge systemic gaps, they undercut the effectiveness of monetary policy. Formal infrastructure solutions like PAPSS’s Africa Currency Marketplace, and regulated stablecoin systems, present a path toward scaling efficiency while potentially preserving policy control. Understanding this evolving landscape is vital for citizens, policymakers, and businesses alike.

johneb492254456

An Analysis of Why Gold Is Becoming a Defensive Currency for African Central Banks

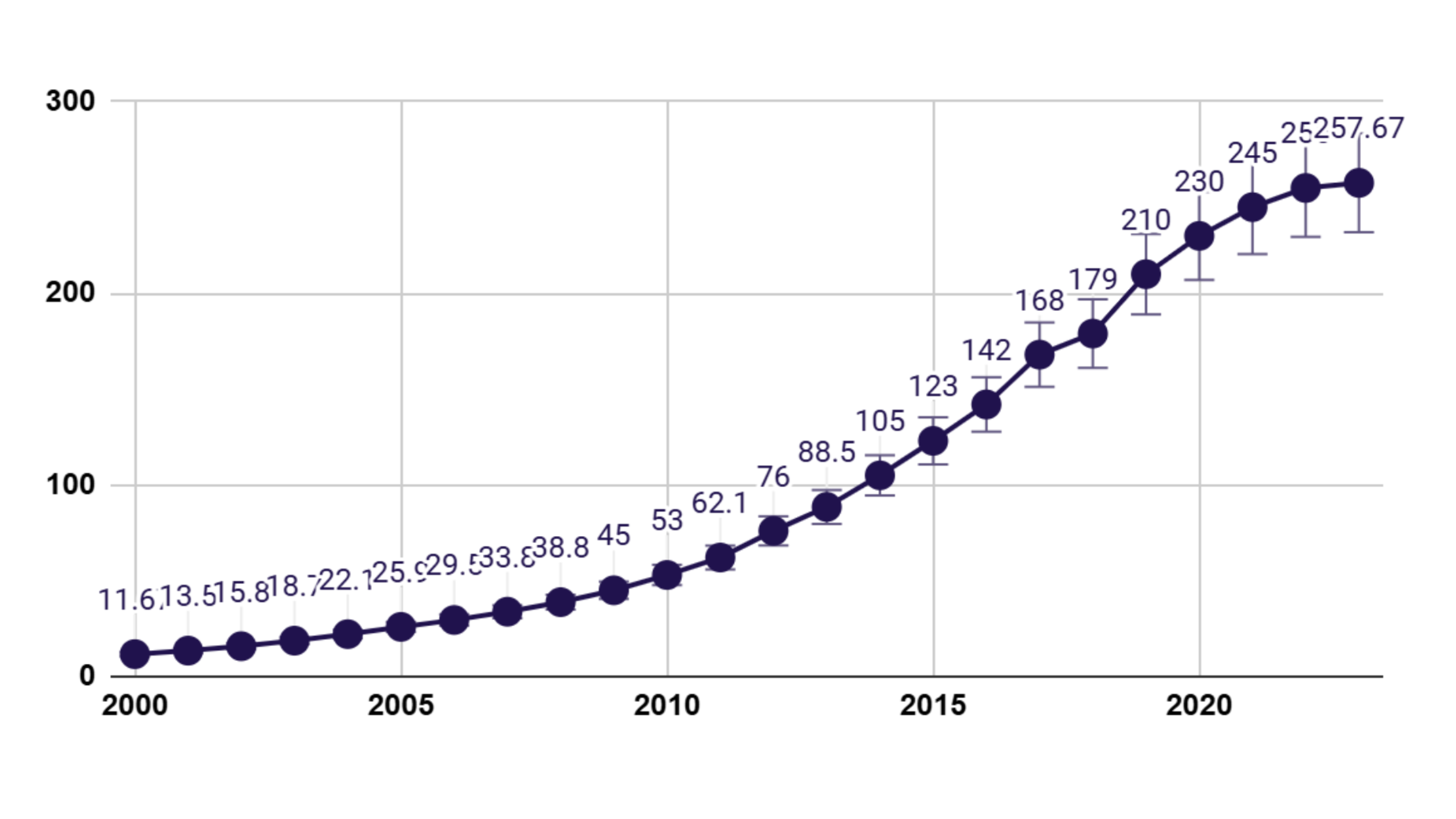

August 18, 2025 by johneb492254456 Global economic uncertainty has spiked in 2025, driven by renewed U.S. trade wars, interest-rate divergences, and geopolitical tensions. U.S. President Trump’s threat of steep tariffs on Europe and elsewhere – effectively “weaponizing” the dollar has unsettled markets. In mid-March 2025, for example, gold surged to historic highs as investors fled into safe havens amid news of Trump’s tariffs, giving a temporary boost to commodity-linked currencies like South Africa’s rand. Across emerging markets, Federal Reserve policies and fiscal strains have widened growth and rate gaps, putting extra pressure on fragile local currencies. In this context, where the dollar’s dominance and U.S. policy are viewed with growing distrust, many African central banks are rebuilding gold reserves as a hedge against foreign-exchange shocks. Gold’s appeal lies in its unique reserve attributes: it is a stable, liquid store of value with no counterparty risk. As one analysis puts it, “gold remains a critical asset for central banks globally due to its stability, liquidity, and consistent returns”. World Gold Council (WGC) surveys find that 95% of monetary authorities expect gold holdings to rise in the next year. Central banks bought record amounts of gold in 2023–2024 (over 1,000 tonnes each year), nearly doubling the decade’s average. In 2024, central banks worldwide held about 36,000 tonnes of gold – close to a six-decade high – as 66% of them increased bullion to diversify and roughly 20% did so as a geopolitical hedge. Emerging-market banks in particular have been most aggressive. For example, in May 2025, the World Gold Council reported big purchases by Kazakhstan (+7t) and Turkey (+6t), as well as gains by Poland and even Ghana (+1t). Surveyed officials explicitly cite “trade protectionism” and “currency shocks” as reasons to add gold. These global trends echo loudly in Africa. Analysts note that gold reserves “act as a safeguard against currency volatility” and signal credibility to investors. In economies prone to sudden FX swings, central banks see bullion as insurance. According to African Leadership Magazine, “Africa’s central banks increasingly turn to gold to secure economic resilience, enhance monetary sovereignty, and build investor confidence” in today’s unstable climate. Gold’s long-term value retention makes it a powerful “financial anchor” for nations wary of any single foreign-currency peg. A World Gold Council survey underscores this shift: 76% of central bankers now project that gold will make up a larger share of reserves over five years, while 73% expect the dollar’s share to shrink. In short, policymakers worldwide – and especially in the Global South – are interpreting U.S. policy moves as a wake-up call to reduce over-dependence on the greenback. Africa’s largest gold reserves tend to be in North African countries (Algeria, Libya, Egypt), but sub-Saharan nations are accelerating their accumulation. Business Insider Africa reports that Algeria holds ~174 t, Libya ~147 t, and Egypt ~128 t as of Q1 2025. Ghana – Africa’s top gold producer – leads in Sub-Saharan holdings with ~31.0 t. In recent years, Ghana’s central bank has embarked on an aggressive “Gold for Reserves” policy, boosting official stock from under 9 t in mid-2023 to ~33 t by June 2025. Mauritania, Kenya, and others have added more modest amounts to diversify away from foreign currency. The message is clear: even resource-rich exporters (like Ghana) are hoarding bullion not just for revenue, but as reserve backing to insulate their cedi. Smaller economies – facing narrow export bases – likewise treat gold as a buffer rather than a mere windfall. According to Business Insider Africa, many African central banks now see gold as part of sovereign risk management. Gold reserves “strengthen monetary sovereignty and reduce reliance on foreign currencies,” enhancing credibility in international markets. This thinking dovetails with global patterns: emerging markets, collectively, plan to increase gold holdings faster than advanced economies. One WGC survey found nearly half of Global South central banks intend to grow gold reserves in the coming year, versus only one-fifth of advanced economies. These banks point to trade wars and sanctions as prime motivators – doubts about the dollar’s safe-haven status have prompted them to “shift their reserves towards gold at a much faster rate than advanced economies”. Nigeria’s naira has been among Africa’s weakest currencies, driven down by inflation, import dependence, and FX shortages. At times, the naira has plummeted over 20% in a month, and even aggressive rate hikes by the Central Bank of Nigeria (CBN) have struggled to halt declines. Such volatility has led legislators to push new policy frameworks: in July 2024, a Nigerian senator proposed a Gold Reserve Bill to formalize gold’s role in monetary policy. The draft legislation would make the CBN the “off-taker” of all domestic gold and target a minimum of 30% of reserves in bullion. Its stated aim is to use gold “as a financial anchor, providing a secure foundation for currency value and overall economic health”, thus “mitigating inflation and deflation risks” and stabilizing the naira. Though still under consideration, this bill underscores how Nigeria’s policymakers are eyeing gold as a tool to shore up credibility. Meanwhile, on the ground, the CBN is quietly expanding its bullion holdings. In its 2024 audited accounts, the bank disclosed that gold reserves jumped in value from ₦1.28 trillion to ₦2.77 trillion (about $6.2 billion) between end-2023 and end-2024. (The quantity of gold held – ~687,400 troy ounces – was unchanged; the entire increase came from higher prices.) Importantly, gold’s share of Nigeria’s total reserves rose from ~4.3% to ~5.1% in one year. As one analysis noted, this “signals a deliberate diversification away from traditional currency reserves, providing a hedge against dollar volatility and global financial risks”. In other words, Abuja sees gold as one way to buttress its reserves when the U.S. dollar is unpredictable. Traders and businesses in Nigeria have long felt the pinch of dollar shortages and rate swings. One foreign exchange researcher observed that even savvy importers have given up on dodgy naira/dollar markets – some transact in Chinese yuan or cryptocurrencies – just to avoid the naira’s roller coaster. This de-dollarization from below – ordinary companies and entrepreneurs finding alternatives to the USD – reflects the scale of mistrust in the formal FX system. In this environment, policymakers argue that beefing up gold stockpiles will help “backstop” the naira and keep inflation expectations in check. Ghana presents a case of a country turning its natural advantage into monetary insurance. After defaulting on its debt in 2023, Ghana entered an IMF program and urgently needed foreign exchange. Gold exports – already Africa’s largest – became a lifeline. By mid-2025, Ghana’s gold exports had surged over 75% year-on-year, creating a large trade surplus that bolstered reserves to about $11.1 billion (enough for 4.8 months of imports). The cedi appreciated roughly 40% in 2025, making it one of the world’s best-performing currencies that year. Bank of Ghana Governor Johnson Asiama has explicitly linked gold to stability. Since May 2023, the BoG has purchased local gold on the market (via the Gold Board) and added it to reserves. Its total gold stock shot from 8.78 t in 2023 to 32.99 t by June 2025. In June alone, it bought 0.83 t – the largest monthly increase of 2025. Asiama explains that formalizing small-scale gold exports into reserve accumulation “directly translates to reserve growth and monetary stability”. In BoG’s words, gold serves as a “safe-haven asset and a hedge against currency depreciation” amid global turmoil – precisely what dollar and euro reserves cannot guarantee in volatile times. Analysts see Ghana’s moves as aimed at insulation. By bulking up gold, the central bank avoids having all its eggs in one basket. The June 2025 jump to 33 tons of gold “signals to investors, multilateral lenders, and credit rating agencies that Ghana remains committed to building a resilient macroeconomic framework,” one report noted. It also keeps value in the domestic mining sector: buying Ghanaian-mined gold means less pressure on FX markets to pay for imports. To lock in gains, Ghana is even exploring hedging future gold prices to protect its reserve build-up. All told, Ghana exemplifies how a developing country can leverage its gold output as a buffer and a signal of prudent management. South Africa has long been a major gold miner, though its central bank holds relatively modest bullion reserves by African standards. Still, the South African rand – often called a “commodity-backed currency” – naturally reacts to gold’s fortunes. In March 2025, for example, gold’s rapid rally (to ~$3,500/oz) helped lift the rand about 0.7% against the dollar, even while domestic political uncertainty was dampening confidence. One market analyst observed that the rand’s strength that week was “more to do with the record gold price and strong commodity prices” than any local factor. In other words, even an asset like the rand benefits indirectly from safe-haven flows into gold and mining stocks. Behind the scenes, rising gold prices also inflate the value of South Africa’s reserves. By April 2025, the SARB reported that higher bullion prices had effectively added about R19.4 billion (~$1 billion) to its reserves in just one month. The Bank’s statement made clear that this was “mainly driven by a […] higher gold price” (up 9% in March). Overall, South Africa’s gold reserves grew in value by some $2 billion in 2025 amid “mounting US policy uncertainty”. Thus, even without active new purchases, South Africa is accruing benefits simply by being a gold exporter. Policymakers treat the windfall conservatively, but it does give some extra breathing room as global trade tensions roil markets. It is notable, however, that unlike Ghana or Nigeria, the SARB has not signaled an aggressive new gold-accumulation campaign. South Africa’s strategy remains focused on traditional foreign-exchange management, even as it watches prices. But the recent episode underlines a broader point: in a world of “weaponized” dollars, even commodity economies find that higher gold prices can shore up their currency and reserves. Beyond individual countries, the turn toward gold reflects a deeper shift. Surveys show roughly half of central banks in the “Global South” (emerging markets and developing economies) plan to expand gold reserves in the next year. In contrast, only about 21% of advanced economies intend to do so. Respondents cite geopolitical instability and rising trade protectionism – in part due to U.S. tariffs – as chief reasons. Indeed, one anonymous official told the WGC that recent U.S. tariff policies may “reduce interest in USD and USD-denominated assets as a reserve currency”. They foresee a gradual but steady “de-dollarization” even if the dollar’s institutional advantages remain strong. Many analysts argue that Africa’s gold drive is ultimately a symptom of mistrust in the existing dollar-based system. When traders in Nigeria or Ghana find it hard to get dollars at reasonable rates, or fear sanctions risk, the appeal of alternatives grows. The gold trend dovetails with other “de-dollarization” efforts: currency swaps with China, talk of new trade currencies, even experiments with digital tokens (Zimbabwe’s gold-backed token, for example). But gold is the oldest form of diversification: it requires no new technology or alliance. As one report put it, central banks are sharpening “active reserve management,” with 44% now handling gold separately from other assets. In sum, Africa’s central banks are turning to gold as both insurance and signaling. Insurance because gold can cushion shocks – a 20% jump in bullion value can instantly relieve pressures that might otherwise crash a currency. Signaling because each tonne of gold amassed tells markets that a country is breaking from the dollar-only playbook. It suggests an acknowledgement that past fixes – IMF bailouts, dollar borrowing – may not be enough for the next crisis. By contrast, gold requires no one’s good graces and cannot be unfriended or sanctioned.

johneb492254456

Introduction

African Gold Reserves on the Rise

Nigeria: Fortifying the Naira

Ghana: Using Gold to Anchor Recovery

South Africa: Gold Prices Bolster the Rand and Reserves

The Global South and the De-Dollarization Trend

An Analysis of Africa’s Push to Replace Imports with Local Production and What’s Holding It Back

August 18, 2025 by johneb492254456 Introduction Across Africa, the rallying cry for economic sovereignty has grown louder over the past five years. Governments from Lagos to Nairobi have launched ambitious “Made-in-Africa” campaigns designed to curb the continent’s deep reliance on imports, stabilize local currencies, and create jobs through domestic production. The vision is bold: produce more, import less, and build competitive industries that can meet both local and export demand. This movement gained urgency during the COVID-19 pandemic and subsequent global supply chain disruptions, which exposed Africa’s vulnerability to external shocks. Between 2020 and 2025, nations such as Nigeria, Kenya, and South Africa intensified their push for industrialization and self-reliance, targeting sectors ranging from agriculture and textiles to cement and automotive manufacturing. Policy tools have included import bans, high tariffs, local content requirements, and state-backed industrial funds. Yet, despite strong political will, progress remains uneven. While Nigeria boasts over 100 modern rice mills and South Africa runs industrial localization programs, the continent continues to import a significant share of its food, textiles, machinery, and consumer goods. The reasons are systemic: unreliable energy supply, outdated manufacturing technology, fragmented supply chains, limited access to affordable capital, and inconsistent policy enforcement. In some cases, policies intended to protect local producers, such as duty waivers or import restrictions, have been undermined by smuggling and global price pressures. This report analyzes Africa’s evolving import-substitution drive between 2020 and 2025, focusing on Nigeria, Kenya, and South Africa. It examines key policy initiatives, sector-specific case studies, and the structural barriers preventing meaningful industrial transformation. The goal is to provide a data-driven understanding of why the continent’s aspiration to become a production powerhouse has not yet translated into reality and what it will take to change that trajectory. African governments have launched high-profile “Made-in-Africa” initiatives aiming to shrink import bills and strengthen local industries. The rationale is clear: boost jobs, curb foreign currency outflows, and stabilize currencies. In practice, however, progress has been mixed. The continent’s manufacturing value added (MVA) has stagnated around 12–13% of GDP in recent years – well below the levels of emerging economies – and only a handful of countries (Nigeria, Egypt, South Africa, Algeria, and Morocco) had MVA above $10 billion in 2023. A recent study estimates that even a modest rise in Africa’s manufacturing share (e.g., +2 percentage points) could boost per-capita GDP by roughly $190 (PPP) by 2043, underscoring the potential payoff of successful industrial policy. But across Africa, key constraints loom large: bottlenecks in supply chains and infrastructure, erratic policies, and expensive power and capital keep local firms from competing effectively. In short, while leaders speak of “produce more, import less,” turning that into reality requires tackling deep-rooted weaknesses. Meanwhile, on the ground, the CBN is quietly expanding its bullion holdings. In its 2024 audited accounts, the bank disclosed that gold reserves jumped in value from ₦1.28 trillion to ₦2.77 trillion (about $6.2 billion) between end-2023 and end-2024. (The quantity of gold held – ~687,400 troy ounces – was unchanged; the entire increase came from higher prices.) Importantly, gold’s share of Nigeria’s total reserves rose from ~4.3% to ~5.1% in one year. As one analysis noted, this “signals a deliberate diversification away from traditional currency reserves, providing a hedge against dollar volatility and global financial risks”. In other words, Abuja sees gold as one way to buttress its reserves when the U.S. dollar is unpredictable. Nigeria’s push goes beyond rice. In 2025, the Tinubu administration unveiled a “Nigeria First” industrialization policy mandating that all federal agencies prioritize locally made goods. New procurement rules will favor Nigerian products, and incentives (like preferential credit) are planned to spur domestic production. Historically, such measures have had some success. For instance, Nigeria’s long-standing restriction on cement imports helped domestic producers increase their output from just 2 million tonnes in 2002 to over 40 million tonnes by 2020. However, those same protections also left cement makers without access to cheap imported inputs, driving up costs and creating opportunities for smuggling. Indeed, a 2015–2023 “41 items” list from the Central Bank barred foreign-exchange access for goods (cement, textiles, foods, etc.) supposed to be made locally, only lifted in October 2023. When bans were lifted, manufacturers faced sudden competition, and when bans tightened, they faced input shortages. In practice, analysts note that policy inconsistency and weak enforcement often negate the intended benefits of import bans. One economist observes that while tariffs protect certain jobs, consumers and many local businesses lose out from higher prices and limited choice. Beyond trade rules, Nigeria’s factories grapple with steep production costs. Most critically, power supply remains far below demand. The country needs over 30,000 MW but only generates about 4,000 MW on average. Manufacturers respond by running generators (at three to four times the cost of grid power). The Manufacturers’ Association warns these electricity bills are “slashing” profit margins, causing unsold inventory and even factory closures. In short, Nigeria’s import-substitution drive is hobbled by familiar barriers: unreliable power, expensive energy, and fragmented supply chains. Without reliable infrastructure and steady policies, the ambitious “produce more” goal risks falling short. Kenya has also tried to reignite local manufacturing – especially textiles – but progress has been elusive. Under the African Growth and Opportunity Act (AGOA) Kenya once exported garments widely. Today, however, it is Africa’s top importer of second-hand clothes. In 2023, Kenya paid about KSh 38.5 billion (≈$298 million) for used apparel, a 12.5% jump from 2022. That volume even exceeds Nigeria’s, despite Nigeria having over four times Kenya’s population. As the Business Insider report notes, this “mitumba” surge is meeting Kenya’s demand for cheap clothing but mocks the country’s revival plans. Manufacturers lament an “unfair” playing field: the Kenya Association of Manufacturers (KAM) points out that domestic firms face intense competition from low-cost imports (new and used). In mid-2024, for example, the Kenyan Parliament quietly abolished two import levies on used clothing, effectively making mitumba even cheaper – a move local producers openly opposed. By contrast, neighbors such as Uganda, Rwanda, and Ethiopia have tightened or taxed used-clothing imports to protect local mills. Kenya’s experience shows that without import controls or incentives, consumers will favor far less expensive textiles, regardless of government slogans. Aside from apparel, Kenyan manufacturers face broad cost pressures. A late-2024 KAM survey found that nearly half of firms expect input prices (raw materials, fuel, power, taxes) to rise in 2025. Key grievances include rising energy and fuel prices, heavy excise duties on locally made goods, and erratic policy changes. Many manufacturers say they are in a “wait-and-see” mode until regulatory uncertainty clears. Cheaper imports from China and neighboring countries continue to erode market share. Some Kenyans see opportunity in import substitution: textiles, footwear, and agro-processing are cited as sectors that could replace imports. But real gains hinge on fixing underlying issues: Kenya needs more reliable power, streamlined transport networks, and access to credit before its factories can scale up. In the words of one industry leader, the country “has not been intentional” enough about growing manufacturing, and must address these barriers for any “Made in Kenya” strategy to work. South Africa’s economy is far more industrialized, and its government has long promoted localization policies. Like Nigeria and Kenya, Pretoria also faces high energy costs and infrastructure issues. Chronic power outages (load-shedding) and expensive electricity make factories less competitive. Over the past year, the South African government has rolled out support programs: it created an export-promotion desk, extended financial aid to exporters, and established a Local Production Support Fund to finance import-substitution projects. These measures are explicitly meant to bolster the industrial base in the face of global shocks (e.g., new U.S. auto tariffs). However, observers warn that policy alone won’t help unless the fundamentals are fixed. The auto sector provides a stark illustration. South Africa exports hundreds of thousands of vehicles, but 64% of cars sold domestically are imported, and local content (the share of locally made parts) remains only ~39% – well below the 60% target. In 2023, this imbalance helped trigger 12 factory closures and 4,000 job cuts in automotive supply chains. New U.S. tariffs (30% on SA cars and parts) threaten to exacerbate this by restricting a $1.6 billion export market. The trade minister has responded by expanding incentives (even for electric-vehicle parts) and seeking to boost local procurement to “unlock” domestic demand. Still, analysts stress that without fixing energy and skills gaps, just localizing procurement won’t revive the industry. In short, South Africa has strong institutions and policies in place, but persistent power blackouts, financing constraints, and global competition continue to impede “Buy Local” ambitions. Across Africa, the picture is clear: the ambition to substitute imports is widespread, but obstacles are systemic. Major challenges cited by experts include: These issues are mutually reinforcing: without abundant, affordable power and strong infrastructure, even well-intentioned policies can’t boost output. As one regional analysis notes, localizing industry must go hand-in-hand with fixing the underlying weaknesses in productivity. The scale of the prize is large – modeling suggests that industrializing Africa even slightly faster could create millions of jobs and lift tens of millions out of poverty by 2040 – but only if these structural gaps are closed. In summary, Nigeria, Kenya, and South Africa have all made bold rhetoric and selective policy moves (bans, procurement rules, funds) to encourage local production. But in 2025, the results are uneven. Where underlying conditions (investment, power, policy stability) are poor, import dependence remains high. As one expert put it, without reliable infrastructure and consistent support, import-substitution becomes “a siren song” rather than a sustainable path to industrialization. For Africa to truly move from importing to producing, governments will need to match their political will with reforms that tackle the root causes – ensuring that local “Made-in-Africa” goods can be price-competitive, high-quality, and reliably delivered.

johneb492254456

Africa’s Import-Substitution Drive: Ambition vs. Reality

Nigeria: Aggressive Policies vs. Practical Hurdles

Kenya: Textile Revival Meets Fierce Import Competition

South Africa: Localization Ambitions Amid Crises

Continental Challenges and Outlook

What Happens When Your Supplier’s Bank Fails 7,000km Away?

August 13, 2025 by johneb492254456 In an era where global trade relies on intricate networks spanning continents, a bank failure thousands of kilometers away can cripple suppliers by freezing their access to credit and liquidity, leading to halted production and delayed shipments that ultimately affect businesses and consumers far downstream. This StayWired presentation explores these vulnerabilities through data from authoritative sources like the International Monetary Fund and the World Bank, illustrating how such financial shocks amplify economic downturns via a bank distress amplifier that exacerbates costly failures and raises solvency uncertainties across interconnected economies. For instance, during the 2007-2009 financial crisis, 168 banks failed in the United States alone, triggering widespread disruptions that echoed through global supply chains and reduced trade volumes in exposed regions. When a supplier’s bank fails overseas, it typically begins with the institution’s inability to meet its financial obligations, often triggered by rapid deposit withdrawals, asset devaluations, or regulatory shortcomings, as seen in the 2023 collapses that prompted the IMF to warn of heightened stability risks amid tighter monetary policies. Such events freeze accounts and restrict credit access, leaving the supplier unable to process payments or secure loans for ongoing operations, which in turn disrupts their ability to fulfill orders promptly. According to a Bloomberg report, these failures serve as stark reminders of vulnerabilities in the financial system, where even isolated incidents can exacerbate inflation pressures through interrupted supply flows, as small businesses providing niche inputs face sudden liquidity shortages that cascade outward. Examining the 2023 Silicon Valley Bank collapse provides a clear example, where its failure disrupted tech suppliers worldwide, causing cash flow crises that delayed component deliveries and forced companies to renegotiate contracts amid uncertainty, as detailed in analyses from financial platforms like RapidRatings. Similarly, the long-run effects of 19th-century London bank failures, as studied in economic papers, reshaped international trade for decades, with exposed regions never fully recovering lost export growth relative to unaffected areas, underscoring how distant financial shocks embed structural changes in global commerce. Bloomberg reports on the IMF’s assessments of these incidents reveal that they ignite stability concerns, particularly when combined with factors like interest rate hikes, leading to widespread supply bottlenecks as seen during the 2008 crisis when trade volumes plummeted To shield against the fallout from a distant supplier’s bank failure, businesses can diversify their supplier base across multiple regions and financial institutions, regularly monitor banking health through reports from entities like the IMF, and incorporate contingency clauses in contracts that allow for swift pivots to alternatives. Insights from Bloomberg suggest hedging against inflation spikes via forward contracts or insurance products that cover disruption losses, while maintaining emergency funds to bridge short-term gaps in supply flows. The World Bank’s guidance on economic prospects advocates for enhanced global regulatory cooperation to address vulnerabilities exposed by failures, encouraging companies to leverage trade finance tools that secure payments independently of local banks. Additionally, adopting digital tracking systems for supply chains can provide early warnings of financial distress in supplier networks, as recommended in IMF stability reports. Ultimately, a bank failure 7,000 kilometers away underscores the fragility of global interdependence, where one institution’s collapse can trigger widespread supply disruptions, but armed with knowledge from IMF warnings and Bloomberg analyses, businesses can build resilience to weather these storms. Key takeaways include recognizing the 8.5 percent export hit from such events and prioritizing diversification to sustain operations, as evidenced by historical and recent data showing long-lasting trade reshaping. Moving forward, ongoing reforms in financial oversight, as urged by the World Bank, promise to dampen these risks, empowering the general public and entrepreneurs to engage in international trade with greater confidence.

johneb492254456

The supplier, often a small or medium-sized enterprise in a distant country, experiences an abrupt halt in financial operations when their bank fails, as frozen assets prevent them from paying employees, purchasing raw materials, or servicing debts, leading to operational paralysis that can last days or weeks while regulators intervene. A study published in the Quarterly Journal of Economics reveals that regions exposed to such bank failures see immediate export drops, with affected entities struggling to maintain production due to credit crunches that limit inventory replenishment. Bloomberg analyses further indicate that these disruptions can boost inflation by forcing suppliers to seek costlier alternative financing, if available, thereby raising prices passed along the chain. The IMF’s Global Financial Stability Report underscores this by noting that cyber-related or market-driven bank failures amplify these issues, creating a domino effect where suppliers’ inability to meet commitments erodes trust in international partnerships.

The supplier, often a small or medium-sized enterprise in a distant country, experiences an abrupt halt in financial operations when their bank fails, as frozen assets prevent them from paying employees, purchasing raw materials, or servicing debts, leading to operational paralysis that can last days or weeks while regulators intervene. A study published in the Quarterly Journal of Economics reveals that regions exposed to such bank failures see immediate export drops, with affected entities struggling to maintain production due to credit crunches that limit inventory replenishment. Bloomberg analyses further indicate that these disruptions can boost inflation by forcing suppliers to seek costlier alternative financing, if available, thereby raising prices passed along the chain. The IMF’s Global Financial Stability Report underscores this by noting that cyber-related or market-driven bank failures amplify these issues, creating a domino effect where suppliers’ inability to meet commitments erodes trust in international partnerships.

How to Sell to Africa’s ‘Unbanked’—When They’re Not Poor

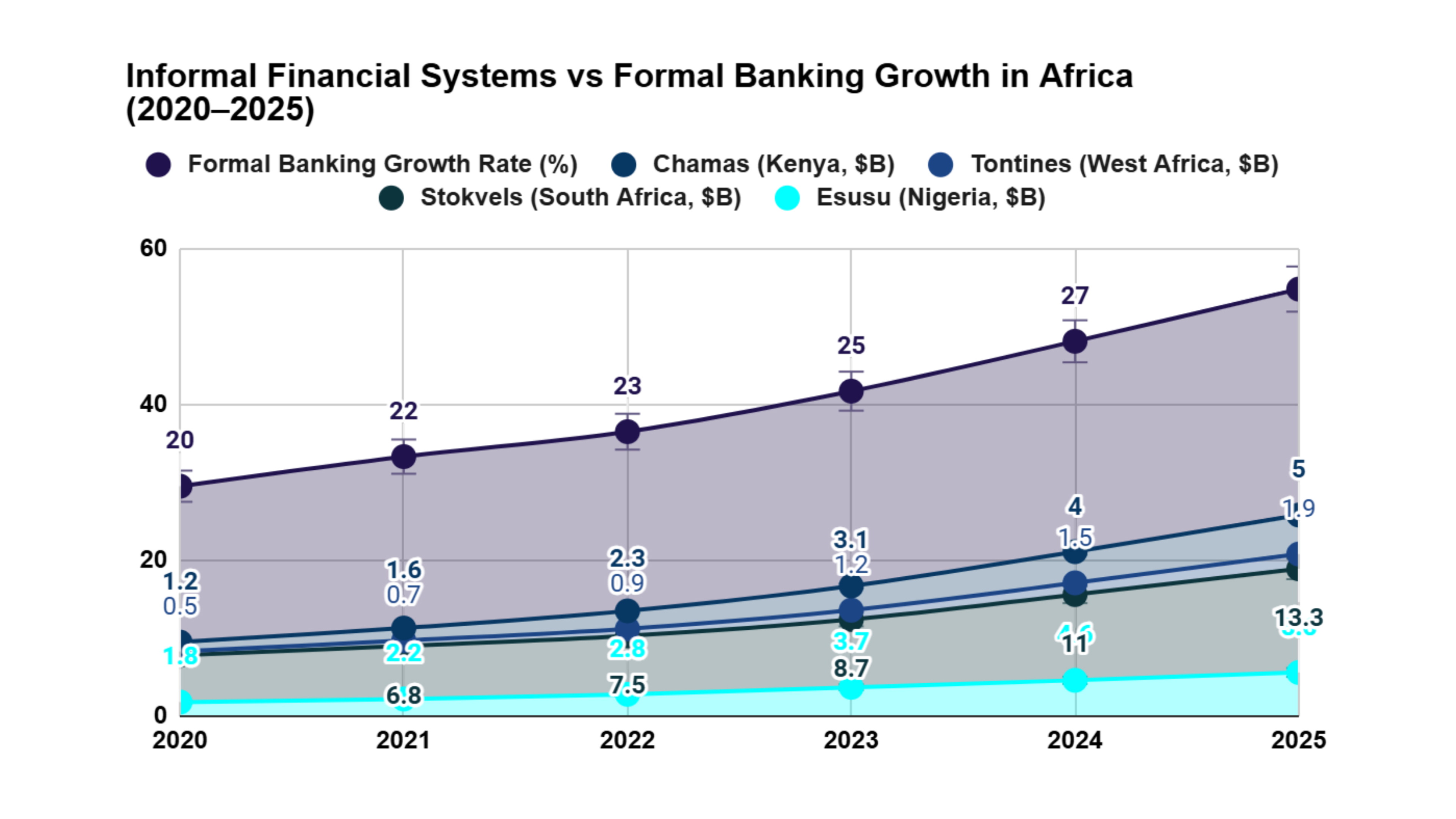

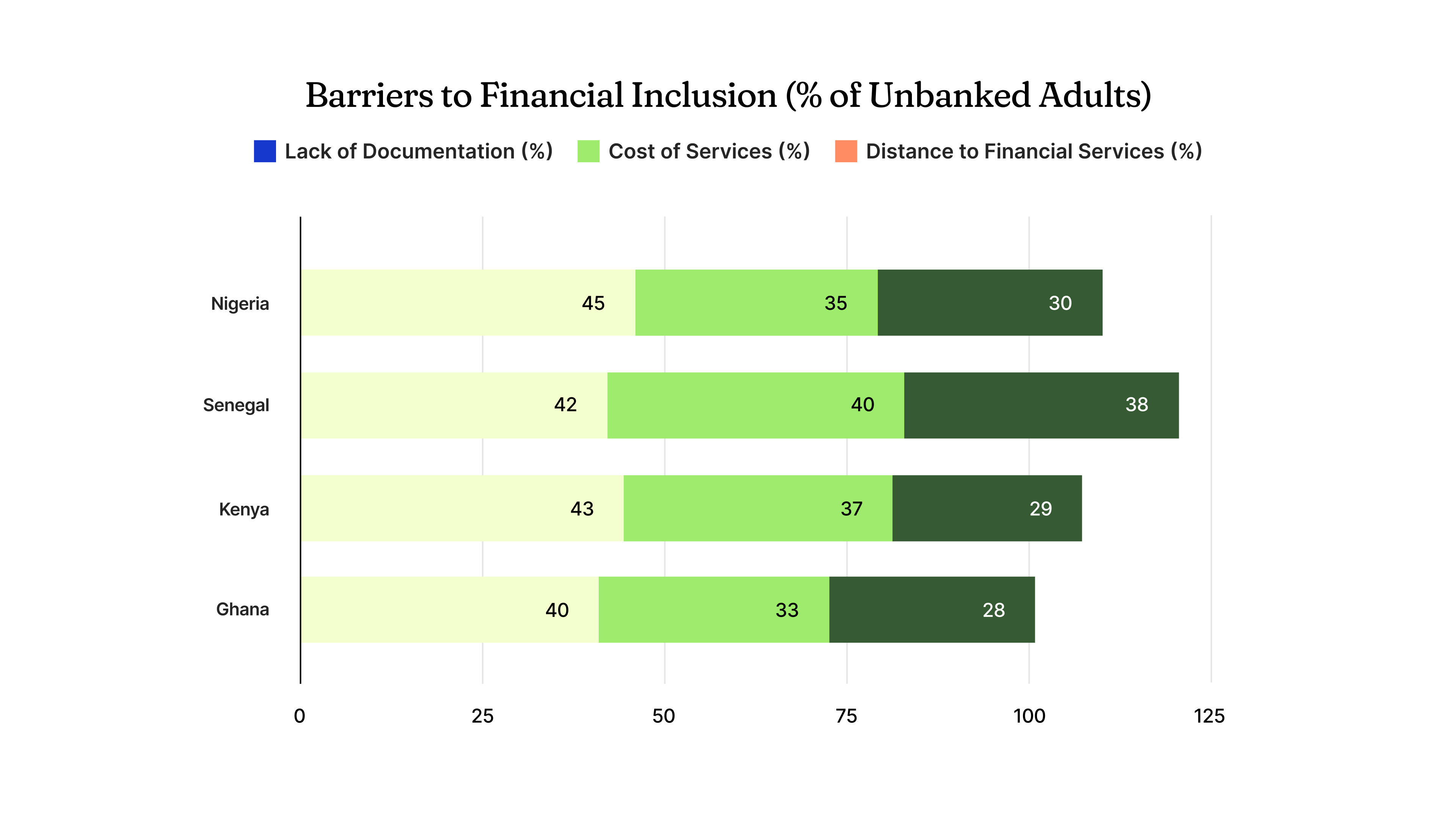

August 6, 2025 by johneb492254456 Africa’s unbanked population, often misjudged as financially excluded, drives a $20 billion informal credit economy through vibrant systems like Nigeria’s esusu, South Africa’s stokvels, and Senegal’s tontines. These community-based mechanisms reveal a market of creditworthy individuals, powered by trust and resilience rather than poverty. With Sub-Saharan Africa’s GDP growth projected at 3.5% in 2025 by the World Bank, this presentation explores how businesses can harness this ecosystem’s potential. Drawing from financial news, think tanks, and reports like the IMF’s 2025 Regional Outlook, we analyze opportunities amidst geopolitical shifts, including Middle East tensions impacting oil markets, and propose strategies for engaging this dynamic market. The notion that unbanked Africans lack financial capacity is misguided. The World Bank’s Global Findex 2021 survey shows over 80 million unbanked adults in Sub-Saharan Africa earn cash from agriculture, trade, or remittances, fueling systems like Nigeria’s esusu, Kenya’s chamas, and Ghana’s susu. These rotating savings and credit associations enable participants to pool funds for business ventures, education, or emergencies, significantly contributing to local economies. South Africa’s stokvels, for instance, manage over $7 billion annually, according to a 2023 Nedbank report. The IMF notes that informal sectors account for 40% of GDP in countries like Nigeria and Kenya, underscoring the unbanked’s economic influence. Businesses must recognize this spending power to design products that align with these trust-based systems. To reach Africa’s unbanked, businesses must integrate with systems like esusu, stokvels, tontines, and chamas. The World Bank’s 2023 Digital Africa report highlights mobile money’s role, with 15% account ownership growth in countries like Ghana from 2017-2022. Fintechs can develop apps to digitize esusu contributions, offering transparency while preserving community trust. Retailers can introduce microcredit or pay-later models, addressing barriers like lack of documentation, which affects 45% of unbanked adults, per Global Findex 2021. Diaspora communities in the U.S. and Europe, adopting similar systems, present a global opportunity. For instance, Ghanaian susu groups in the UK manage millions annually, per a 2024 Bloomberg report. Tailored financial products can bridge local and diaspora markets, amplifying reach. Africa’s unbanked population powers a $20 billion informal credit economy through systems like esusu, stokvels, tontines, and chamas, proving their financial resilience. With Sub-Saharan Africa’s growth projected at 4.2% by 2026 (World Bank), businesses must move beyond stereotypes to tap this market’s potential. By digitizing trusted systems, addressing access barriers, and navigating geopolitical challenges like oil price volatility, companies can unlock significant opportunities. For the general public, this redefines financial inclusion as empowerment, not charity. Startups, retailers, and investors should act now: partner with communities, leverage mobile technology, and build products that amplify these systems’ strengths, positioning Africa’s unbanked as the next frontier for global fintech innovation.

johneb492254456

Africa’s $20 billion informal credit economy thrives on diverse systems tailored to local needs. Nigeria’s esusu involves regular contributions to a communal pot, accessible to members for loans or investments. South Africa’s stokvels support varied goals, from burials to property purchases, while Senegal’s tontines empower women-led enterprises, with 60% of participants being female, per a 2024 African Development Bank study. Kenya’s chamas, often digitized via mobile apps, facilitate group investments in real estate. Despite global challenges like reduced aid flows noted in the African Development Bank’s 2025 Economic Outlook, these systems remain robust, insulated from shocks like oil price fluctuations tied to 2024-2025 Middle East conflicts. Businesses can engage by offering tools that enhance these systems’ functionality without replacing them.

Africa’s $20 billion informal credit economy thrives on diverse systems tailored to local needs. Nigeria’s esusu involves regular contributions to a communal pot, accessible to members for loans or investments. South Africa’s stokvels support varied goals, from burials to property purchases, while Senegal’s tontines empower women-led enterprises, with 60% of participants being female, per a 2024 African Development Bank study. Kenya’s chamas, often digitized via mobile apps, facilitate group investments in real estate. Despite global challenges like reduced aid flows noted in the African Development Bank’s 2025 Economic Outlook, these systems remain robust, insulated from shocks like oil price fluctuations tied to 2024-2025 Middle East conflicts. Businesses can engage by offering tools that enhance these systems’ functionality without replacing them.

Engaging Africa’s unbanked involves navigating risks like Nigeria’s 23.7% inflation rate in April 2025 (IMF) and food insecurity affecting 8% of its population, which strain informal systems. Geopolitical risks, such as potential U.S. aid reductions flagged by the Atlantic Council in 2025, may limit external support, increasing reliance on local networks. However, opportunities abound: Nigeria’s 2024 reforms, including subsidy cuts and currency liberalization, have spurred investor interest, per the IMF, creating a favorable climate for private sector growth. Fintechs and retailers offering affordable, tech-enabled solutions like mobile apps for esusu or tontines can capture a market where 464 million people remain in poverty yet actively drive informal economies.

Engaging Africa’s unbanked involves navigating risks like Nigeria’s 23.7% inflation rate in April 2025 (IMF) and food insecurity affecting 8% of its population, which strain informal systems. Geopolitical risks, such as potential U.S. aid reductions flagged by the Atlantic Council in 2025, may limit external support, increasing reliance on local networks. However, opportunities abound: Nigeria’s 2024 reforms, including subsidy cuts and currency liberalization, have spurred investor interest, per the IMF, creating a favorable climate for private sector growth. Fintechs and retailers offering affordable, tech-enabled solutions like mobile apps for esusu or tontines can capture a market where 464 million people remain in poverty yet actively drive informal economies.

Africa’s $6B P2P USDT Economy Is Growing. Will the GENIUS Act Break or Boost It?

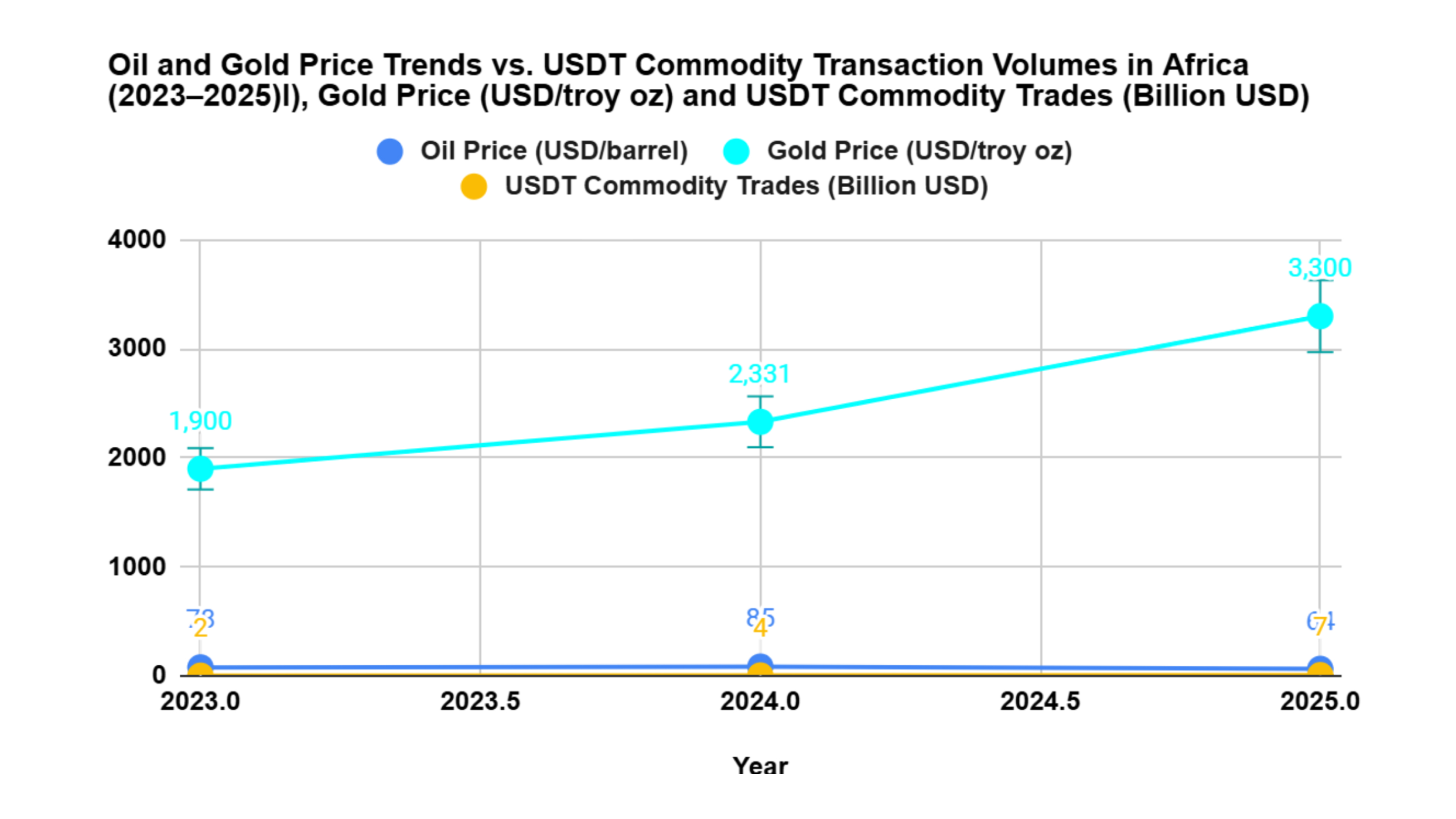

July 30, 2025 by johneb492254456 Africa’s peer-to-peer (P2P) economy, powered by stablecoins like USDT, has surged to a $6 billion market, reshaping trade and finance across the continent. This presentation explores the growth of this digital economy, the potential impact of the U.S.-proposed GENIUS Act, and the influence of recent geopolitical events, including Middle East conflicts and commodity market shifts. Drawing on insights from financial news, think tanks, and official reports from the IMF and World Bank, we analyze the drivers, opportunities, and risks for African markets. Tailored for the general public, this week’s StayWired topic offers a clear and engaging look at how digital currencies and global policies are transforming Africa’s economic landscape. Blockchain analytics from Chainalysis report that sub-Saharan Africa accounted for 9.1% of global cryptocurrency transactions in 2024, with USDT dominating 60% of P2P trading volume, equating to roughly $3.6 billion in monthly transactions across Nigeria, Kenya, and South Africa alone. Stablecoins like USDT, pegged to the U.S. dollar, enable African traders and individuals to bypass traditional banking barriers, where cross-border transaction fees can reach 7-10% and take days to settle. The continent’s young population, with 70% under 30 years old, and mobile penetration rates exceeding 85% in key markets, have fueled this growth, with platforms like Binance reporting a 120% year-over-year increase in P2P USDT trades in Nigeria. The World Bank notes that sub-Saharan Africa’s digital economy grew by 15% annually from 2020 to 2024, supported by blockchain’s secure and transparent transactions. Geopolitical uncertainties, including a tripling of global trade restrictions since 2019, have pushed African users toward USDT to circumvent volatile local currencies, like the Nigerian naira, which depreciated 40% against the USD in 2024, and restricted USD access. This digital shift empowers small-scale traders and businesses, with 80% of African P2P users being micro-entrepreneurs, to engage in global markets with unprecedented ease. Recent geopolitical events have significantly influenced the growth of Africa’s P2P USDT economy. The Russia-Ukraine conflict and escalating Middle East tensions, particularly in 2024, have disrupted global commodity markets, including oil, which accounts for one-third of the world’s seaborne trade. These disruptions, as highlighted by the World Bank, have caused oil price volatility, impacting African economies reliant on imports. The IMF reports that trade restrictions have tripled since 2019, creating a fragmented global economy where African traders face challenges accessing USD through traditional banking systems. Fears of sanctions and tariffs, such as those threatened by U.S. policymakers in 2024, have driven adoption of USDT as a decentralized alternative. This allows African users to maintain trade continuity with partners in Asia and the Middle East, where USDT is increasingly accepted for commodity transactions. The Middle East’s role in oil markets and the rising prominence of gold as a safe-haven asset have bolstered Africa’s shift to USDT. World Bank data indicates that oil price volatility, driven by Middle East conflicts, could increase prices by 6% in 2024, straining African economies with limited USD reserves. USDT provides a stable, dollar-pegged alternative for oil and commodity payments, reducing exposure to currency fluctuations. Meanwhile, gold prices hit a record $2,331 per troy ounce in April 2024, driven by central bank purchases in emerging markets, as noted by the World Bank. This shift toward “politically neutral” assets reflects a broader move away from USD dominance, with African traders using USDT to settle transactions in gold and other commodities. Financial news sources like Bloomberg highlight growing non-dollar commodity contracts, further enabling USDT’s role in African P2P markets. The Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, signed into law on July 18, 2025, establishes a federal regulatory framework for stablecoins like USDT, with significant implications for Africa’s $6 billion P2P economy. By requiring issuers to maintain 100% reserve backing and comply with stringent anti-money laundering and sanctions protocols, the Act enhances trust in stablecoins, potentially boosting their adoption among African traders seeking reliable digital payment solutions. Financial news sources report that the Act’s clarity could attract institutional players, increasing USDT’s legitimacy for cross-border transactions in sub-Saharan Africa, where 60% of the population remains unbanked. However, the Act’s strict compliance requirements, including monthly reserve attestations and federal oversight, may raise costs for platforms like Binance, which could pass onto users, potentially limiting P2P trading in cost-sensitive markets like Nigeria and Kenya. The World Bank highlights that regulatory clarity can drive financial inclusion, but African nations must develop complementary frameworks to balance innovation with consumer protection, ensuring the P2P economy continues to thrive amidst global regulatory shifts. Africa’s $6B P2P USDT economy stands at a crossroads as geopolitical and regulatory dynamics evolve. The GENIUS Act could boost growth by providing regulatory clarity, attracting institutional players, and enhancing financial inclusion, as suggested by World Bank reports on digital economies. However, overly restrictive policies could stifle the informal, low-cost P2P ecosystem that thrives on accessibility. Geopolitical risks, including Middle East conflicts and trade barriers, will likely continue driving USDT adoption as African traders seek resilient payment solutions. The IMF’s exploration of central bank digital currencies (CBDCs) suggests future competition, but USDT’s global reach and ease of use give it a strong foothold. For African economies, balancing innovation with regulatory compliance will be key to sustaining this digital transformation. The general public should watch how these trends unfold, as they could redefine global trade and finance.

johneb492254456

An Analysis of the Cocoa Price Boom: Why Ghana Is Winning in Revenue but Losing in Output

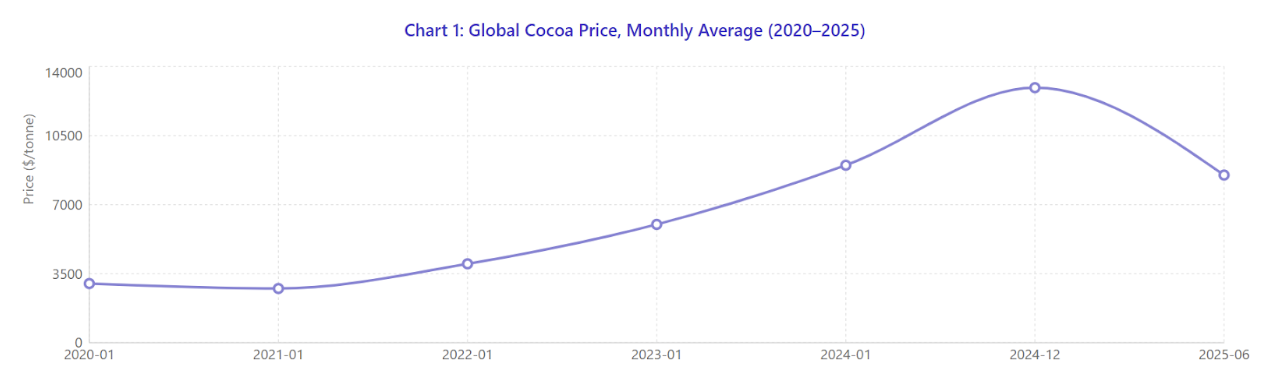

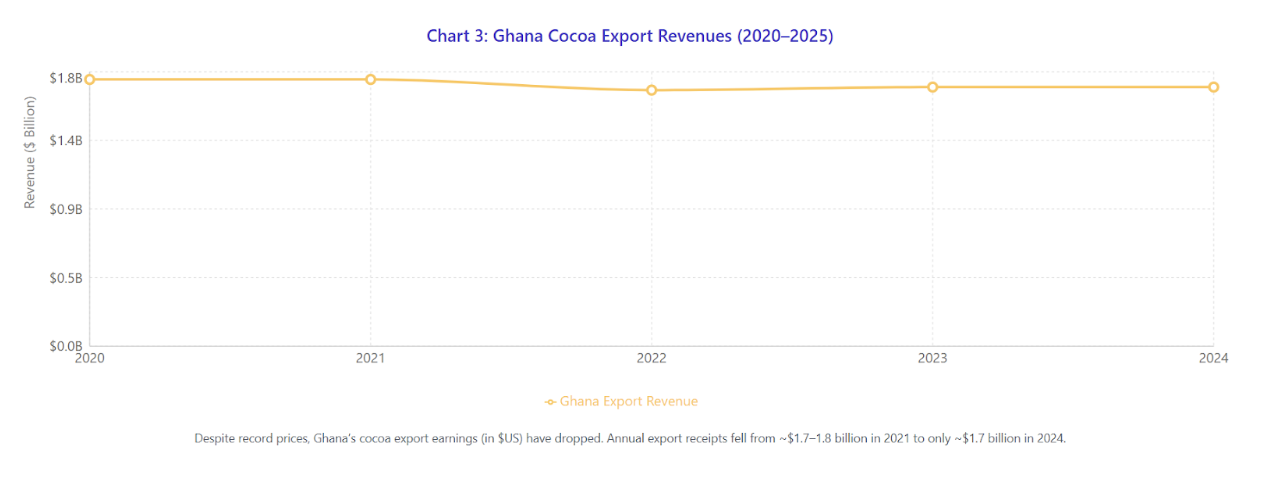

July 14, 2025 by johneb492254456 Global cocoa prices surged sharply from 2020 through 2024. After relatively moderate prices ($2,500–3,000/tonne) in early 2021, supply shocks and weather problems in West Africa drove futures much higher. By late 2024, cocoa had “nearly tripled in price” from its year-ago level, reaching a record NY–ICE high of about $12,930/tonne in late 2024. (For context, cocoa was trading near $3,000 in early 2020.) This boom was driven by consecutive years of production shortfalls in Ghana and Côte d’Ivoire – for example, Ghana fell to ~530,000 tonnes in 2023/24 vs. 1.05 million in 2020/21 – which tightened world supply. The price boom greatly affects Ghana’s economy because cocoa is a major export. Cocoa contributes roughly $2 billion in foreign exchange per year (making it Ghana’s third-largest export). In normal seasons, cocoa revenues help finance the government and foreign currency earnings. When world prices soared, Ghanaian exporters in principle earned more per ton. Indeed, Ghana’s Cocoa Board (COCOBOD) saw its revenues jump – in 2022/23 it reported 17.7 billion cedi (≈$1.15 billion) in cocoa sales, up 42% year-on-year – the first profit in six years for the agency. However, much of this higher price did not translate into Ghana’s export earnings in 2024 (see below). Cocoa remains a staple of Ghana’s export economy. Pre-crisis, Ghana earned roughly $1.7–2.0 billion per year from cocoa exports. For example, cocoa exports earned about $1.26 billion (beans) plus $0.41 billion (paste) in 2022 (≈$1.68 b total). By 2024, however, Ghana’s cocoa export revenues fell rather than rose, despite record prices. Bank of Ghana data show cocoa export receipts dipped below $2 billion, hitting about $1.7 billion in 2024, the lowest level in 15 years. This paradox (record world prices but lower revenues) occurred because Ghana could not immediately sell its crop at the new highs. Due to prior forward-sale contracts (at lower prices) and delayed shipments, Ghana locked in a lot of its exports at much lower rates. In other words, high prices mostly went to fulfilling past commitments. Confectionery News reports that 57% of Ghana’s 2024/25 crop had been sold forward months in advance at pre-boom prices, limiting the benefit to the country. Thus even though global cocoa prices spiked by ~+157% in 2024, Ghana’s export earnings did not rise. At the same time, Ghana’s government coffers from cocoa have been hit by currency and financing issues. COCOBOD’s operations carry heavy debt, and higher international prices did not immediately relieve its obligations. Ghana’s President warned in 2025 that COCOBOD stood to lose ~$1.3 billion on forward contracts written at low prices. (COCOBOD also struggled to roll over $2 billion of accumulated debt.) The shortfall in expected cocoa revenue contributed to Ghana’s fiscal strains in 2024/25. On the positive side, COCOBOD ended 2023 with a profit (2.3 billion cedi, ~$150 million) for the first time in years, as higher sales and its debt restructuring took effect. Overall, though, Ghana’s cocoa-dependent government revenues have not benefited from the price boom to the extent one might expect, because of currency fluctuations and contract timing. Ghana’s cocoa production fell steeply from 2021 onward. After reaching a record ~1.04 million t in 2020/21, output declined to roughly 683,000 t in 2021/22 and 656,000 t in 2022/23. By the 2023/24 harvest (the season ending mid-2024), output plunged further to around 430,000–530,000 t. Early estimates for 2024/25 suggested a modest rebound (600k–700k t) as COCOBOD forecasts improved, but still well below pre-crisis levels. (Ghana’s government is targeting a symbolic 1 million t, which it has only met in 2010/11 and 2020/21.) Multiple factors drove this slump. Climate and weather played a central role: West Africa suffered repeated droughts, unusually dry spells, and higher temperatures that stressed cocoa trees. Analysts note “adverse weather” for four consecutive seasons (2021–24) in Ghana and Côte d’Ivoire, with Ghana’s government explicitly citing an “unusual dry spell” in 2024 that cut its 2024/25 crop estimate from 810,000 to 650,000 t. Hot, dry conditions reduce flower pollination and pod development, sharply cutting yields. Disease and aging trees also hurt yields. Cocoa Swollen Shoot Virus Disease (CSSVD) has spread in western Ghana, killing old cacao trees. Confectionery News reports that aging and disease have undermined Ghana’s mature plantations. Government sources note over 500,000 hectares of older cocoa farms in Ghana are “unproductive” due to CSSVD, old age and miners. Illegal gold mining (“galamsey”) destroyed or displaced many cocoa farms, particularly in the Western Region. Smuggling is another factor: low local prices in past seasons induced farmers to divert cocoa across borders (into Côte d’Ivoire or Togo). Reuters estimates over 150,000 t of cocoa were smuggled out of Ghana annually in 2021–2023. (This smuggled cocoa isn’t counted in Ghana’s official output.) Labor constraints and under-investment are related issues: chronic low farm incomes in recent years meant farmers often skimped on inputs and replanting. Many smallholders age, and cocoa farming has become less attractive to young Ghanaians. Combined, these problems have hit Ghana’s production hard, even as world prices soared. (By contrast, Côte d’Ivoire maintained fairly stable production in 2019–23, highlighting Ghana’s outsized weather and governance issues.) For Ghana’s farmers, the price boom has been a double-edged sword. In principle, higher farmgate prices should raise incomes, and COCOBOD did sharply raise Ghana’s official “producer price”. For the 2023/24 season, COCOBOD raised the farmgate price by 63% to 20,943 cedi/tonne (≈$1,837/t at the time), and for 2024/25 it jumped to 48,000 cedi/tonne ($3,070/t)– roughly three times the 2022/23 level. But these Ghana prices still lag far behind global prices. A Reuters analysis notes Ghana’s 2023/24 producer price of $1,837/t was much lower than world futures ($3,800/t), and by 2024/25 world cocoa peaked near $13,000/t while Ghana’s price was only ~$3,070/t. As a result, the high world market price has not fully reached farmers: many continued to lose out (some resorting to smuggling) rather than benefit from the “cocoa windfall”. Meanwhile, the costs of farming have skyrocketed. Global inflation and currency moves have made fertilizers, pesticides, and labor much more expensive. Fairtrade reports that Ghana’s fertilizer prices (in cedi) nearly tripled since 2019, a 52% rise even measured in USD terms. Overall living costs for rural Ghanaian households jumped sharply in 2022–23. Thus, many farmers face a squeeze: even with higher nominal prices, input and living costs are eating up gains. Fairtrade notes that rising input costs mean farmers have “low profit margins” and may be unable to reinvest in their farms. A Fairtrade/Ghana report warns that the 2022 inflation increases of 59% in Ghana make it hard for farmers to earn a decent living. The combination of low relative prices and high costs has kept many cocoa farmers in poverty. Confectionery News quotes Fairtrade Africa: “Global inflation on the cost of production and living has forced many farmers to live in poverty or extreme poverty.” Ghana’s rural poverty rates in cocoa areas have been high for years. Despite COCOBOD’s price hikes (farmgate roughly tripled in two years), farmers’ real income gains are limited if the Ghana cedi remains weak and inflation persists. Many farmers thus remain cash-poor: land tenure is weak, banks will not lend easily, and farmers often lack funds to replant old trees or buy fertilizers. On the other hand, farmers do receive higher nominal payments per bag now than before the boom. The 2024/25 farmgate price (~3,100 cedi/bag or ~$307/t) is well above the ~$1,100/t in 2022. This may relieve some hardship, but it’s still below the global reference price that Ghanaian coffee/chocolate buyers pay. Ghanaian cooperatives and authorities are under pressure to raise future farmgate prices further: economists estimate a “living income price” of ~$2,100/t would be needed for Ghanaian farmers to earn sustainable incomes. Farm unions have demanded much larger increases in 2025/26.

johneb492254456

Introduction

Prices began to ease somewhat in 2025, as improved weather and carryover stocks alleviated shortages. By mid-2025, ICE cocoa futures fell back to the $8,000–9,000/tonne range. Nonetheless, prices over 2023–24 remained at multidecade highs, roughly 3–4 times the levels of early 2020.

Prices began to ease somewhat in 2025, as improved weather and carryover stocks alleviated shortages. By mid-2025, ICE cocoa futures fell back to the $8,000–9,000/tonne range. Nonetheless, prices over 2023–24 remained at multidecade highs, roughly 3–4 times the levels of early 2020.Ghana Cocoa Exports and Government Revenue

Declining Cocoa Production in Ghana

Declining Cocoa Production in Ghana Impacts on Cocoa Farmers

Impacts on Cocoa Farmers

When Geopolitical Tensions Move Markets: How Rumors of Global Conflict Rocked the FX & Commodity Space

johneb492254456

July 14, 2025 by johneb492254456

Geopolitical tensions, particularly in the Middle East, have long influenced global financial markets, driving volatility in foreign exchange (FX) and commodity prices. Recent events in 2024-2025, centered around escalating conflicts between Israel and Iran, have amplified these effects, impacting everything from oil prices at the pump to gold trading on international markets. This week’s Staywired presentation explores how rumors and realities of global conflict shape the FX and commodity spaces, with a focus on FX, oil and gold.

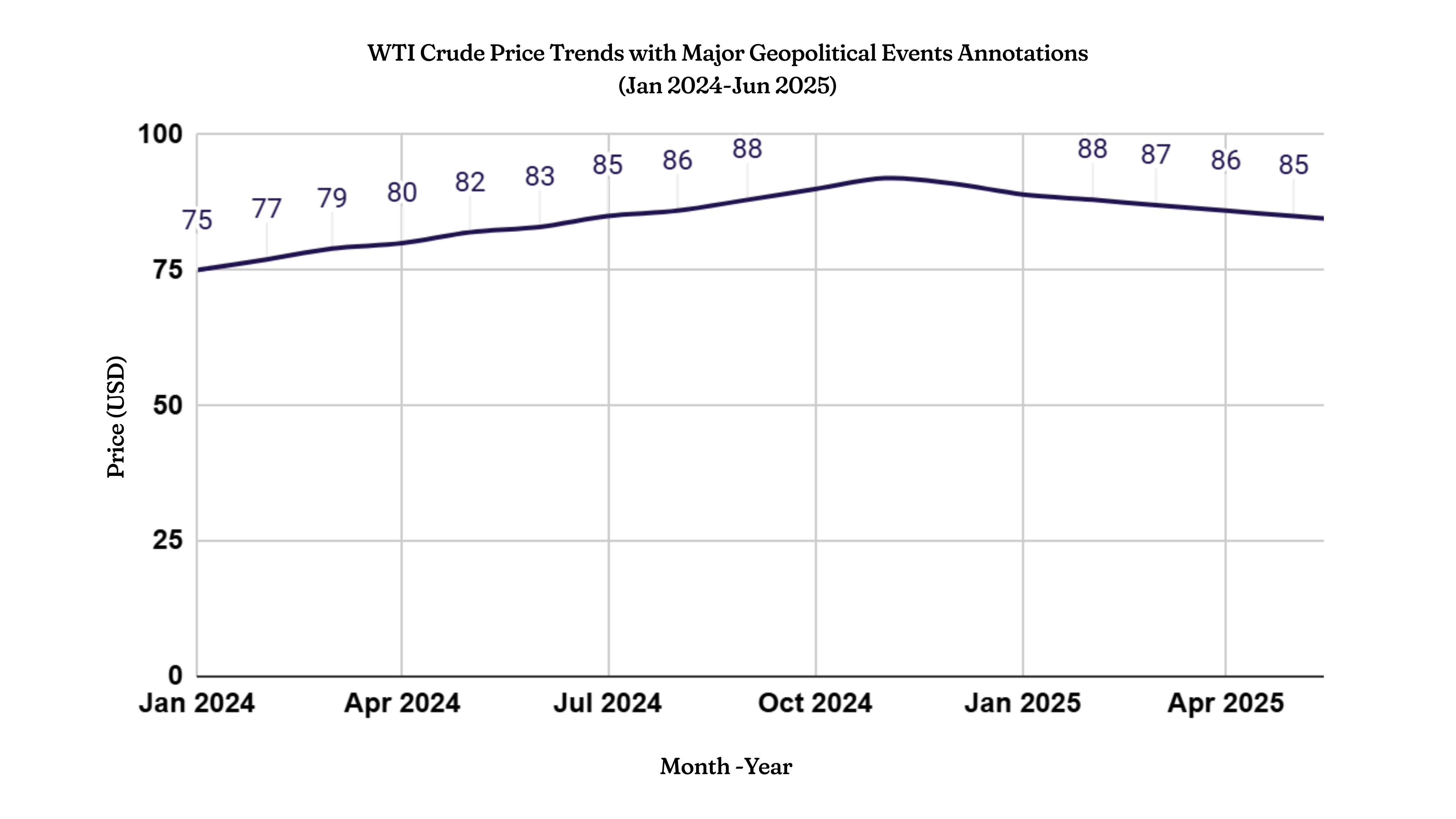

The Middle East has been a hotspot for geopolitical tensions in 2024-2025, with escalating conflicts raising fears of broader regional instability. Key developments, including disruptions in diplomatic negotiations, have unsettled global markets, as reported by Reuters. The Strait of Hormuz, a critical chokepoint for 20% of global oil trade, has become a major concern, with analysts warning that any disruption could spike oil prices by 20-30%. Meanwhile, ongoing rivalry between major global powers vying for regional influence has added further complexity, amplifying market uncertainty. These events have driven investors to seek safe-haven assets like gold and the U.S. dollar, reflecting heightened global risk sentimentOil markets have reacted sharply to Middle East tensions. West Texas Intermediate (WTI) crude prices surged, with forecasts from Kalshi markets predicting a rise to $94.10 by year-end 2024, a $21 increase in a single week. This spike was driven by fears of supply disruptions, particularly through the Strait of Hormuz, which handles a significant portion of global oil exports. Bloomberg reported that oil prices jumped past $80 a barrel following initial Israel-Iran clashes, reflecting trader panic. For consumers, this translates to higher fuel costs, impacting transportation and goods prices globally. The IMF has noted that sustained oil price increases could exacerbate inflation, forcing central banks to reconsider interest rate cuts, which further pressures economies.

As tensions escalated, gold prices soared to near-record highs, as reported by posts on X and Reuters. Investors, spooked by the prospect of a wider conflict, flocked to gold as a safe-haven asset, pushing prices to all-time highs. This surge reflects gold’s role as a hedge against uncertainty, with demand spiking during periods of geopolitical instability. The World Bank has highlighted gold’s sensitivity to global risk sentiment, noting that its price movements often mirror investor fears of economic or political upheaval. For the average consumer, rising gold prices signal broader economic caution, potentially affecting jewelry costs and investment portfolios.

As tensions escalated, gold prices soared to near-record highs, as reported by posts on X and Reuters. Investors, spooked by the prospect of a wider conflict, flocked to gold as a safe-haven asset, pushing prices to all-time highs. This surge reflects gold’s role as a hedge against uncertainty, with demand spiking during periods of geopolitical instability. The World Bank has highlighted gold’s sensitivity to global risk sentiment, noting that its price movements often mirror investor fears of economic or political upheaval. For the average consumer, rising gold prices signal broader economic caution, potentially affecting jewelry costs and investment portfolios.

The U.S. dollar strengthened significantly as markets reacted to Middle East unrest. Posts on X noted a 1.5% drop in U.S. stock futures alongside a rush to the dollar, which traders viewed as a “life raft” amid volatility. This flight to safety stems from the dollar’s status as the world’s reserve currency, often bolstered during crises. The IMF’s 2024 reports underscore that geopolitical shocks tend to increase dollar demand, impacting currency pairs like EUR/USD and USD/JPY. For consumers, a stronger dollar can lower import costs but raise export prices, affecting global trade dynamics. Emerging market currencies, particularly those tied to oil-producing nations, faced depreciation pressures, adding to economic strain.

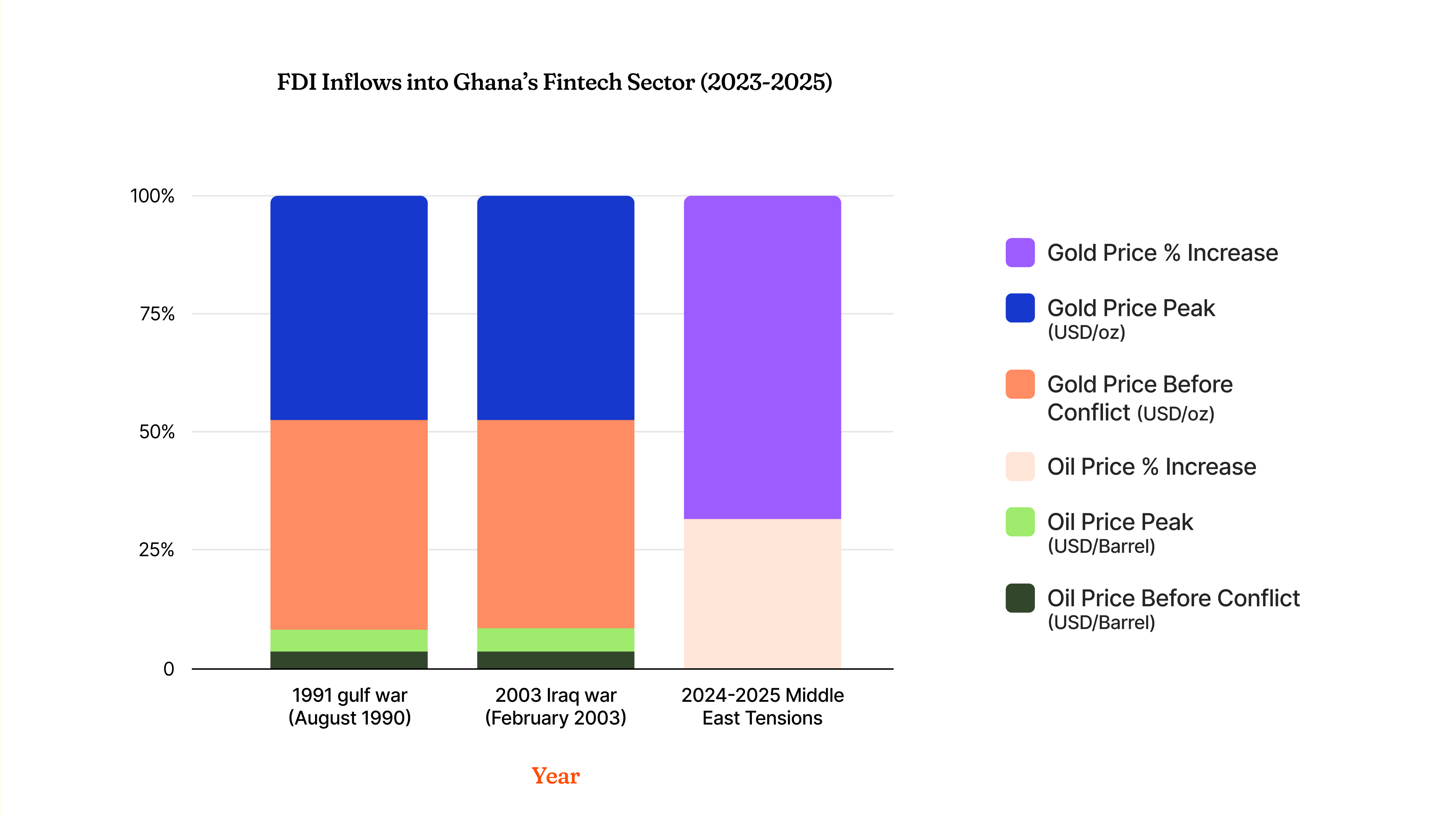

While 2024-2025 events are acute, historical patterns provide context. The 1991 Gulf War saw oil prices spike 30% in weeks, while the 2003 Iraq War drove gold to multi-year highs. These precedents, documented by Bloomberg, show that geopolitical tensions consistently disrupt commodity and FX markets. The Council on Foreign Relations notes that Middle East conflicts have a unique ability to ripple globally due to the region’s oil dominance and strategic importance. Comparing past and present, today’s markets face additional complexities from U.S.-China rivalry and digital asset volatility, amplifying the impact of rumors and confirmed conflicts.

Geopolitical tensions in the Middle East, particularly the 2024-2025 Israel-Iran conflict, have reshaped global markets, driving up oil and gold prices while strengthening the U.S. dollar. These shifts affect everyday life higher fuel costs increase prices at the pump, rising gold prices influence jewelry and investments, and a stronger dollar impacts trade and travel. For the general public, understanding these dynamics is crucial as they navigate rising costs and economic uncertainty. Financial news, IMF reports, and think tanks like the Council on Foreign Relations provide critical insights into these trends. As markets remain volatile, staying informed empowers consumers to anticipate and adapt to these global shifts.