Stablecoins as a Hedge Against Currency Volatility in Emerging Markets

May 11, 2026 by johneb492254456 Stablecoins – digital tokens pegged to stable assets, such as the U.S. dollar – are increasingly used in countries facing chronic inflation and currency volatility. In nations such as Nigeria, Argentina, and Turkey, citizens turn to cryptocurrency as a practical store of value and payment method when local currencies rapidly lose value. Recent reports show Nigeria alone handled ~$22 billion in stablecoin transfers over a year. In Argentina, hyperinflation (over 100% annually in 2023) has driven widespread stablecoin use for savings and even day-to-day payments. And in Turkey, stablecoin transactions surged, totalling roughly 3.7% of GDP in 2024, after currency controls were eased. These digital dollars function as a dollarized parallel economy: the “stablecoin boom” in these markets is not speculation but a survival tool. People use fiat-backed tokens like USDT and USDC to hedge inflation, move remittances cheaply, and access financial services when banks fail them. But stablecoins carry their own risks: reserve transparency, issuer solvency, regulatory uncertainty, and on-chain security are real concerns. Policymakers have noted that heavy stablecoin inflows can even feed back into FX markets, exerting downward pressure on volatile currencies. This article explores how stablecoins work as an inflation hedge and payment rail in emerging economies, and what trade-offs they entail. We survey stablecoin designs (fiat-backed, crypto-collateralized, algorithmic), peg mechanisms, and risks like redemption and custody. We examine macro drivers (inflation, capital controls), use cases (remittances, cross-border trade), and on-chain data. Detailed case studies of Nigeria, Argentina, and Turkey illustrate adoption patterns, user behavior, and regulatory responses. Throughout, we draw on recent data and analysis from the IMF, BIS, financial news, and industry reports. Stablecoins are blockchain-based tokens designed to maintain a fixed 1:1 value with a reserve asset (typically the US dollar). The most common design is fiat-collateralized: e.g. USDC or USDT, where an issuer claims each token is backed by one USD (or liquid treasury) in reserve. These rely on trusted custodians and regular audits. For example, Circle’s USDC is “100% backed by highly liquid cash and cash-equivalent assets and is always redeemable 1:1 for US dollars”. Major stablecoin issuers publish reserve attestations: Circle uses third-party audits and public fund disclosures, while Tether (USDT) has recently shifted its reserves toward U.S. Treasuries. Another design is crypto-collateralized stablecoins (like MakerDAO’s DAI), which lock up other cryptocurrencies as collateral. These require over-collateralization to survive price swings of the collateral. The system’s smart contracts automatically mint new tokens when collateral is deposited and burn tokens when they are redeemed. Real-time price oracles are critical to trigger liquidations if collateral falls in value. Algorithmic (non-collateralized) stablecoins attempt to maintain the peg via code-controlled supply, but these have proven very risky: the 2022 collapse of TerraUSD (UST) showed that purely algorithmic coins can lose their peg catastrophically when confidence falters. In economies with high inflation and tight currency controls, stablecoins naturally appeal. When the local currency is losing value or cannot be freely exchanged, holding a digital dollar in your smartphone wallet can be a lifeline. This dynamic is evident in Nigeria, Argentina, Turkey and beyond. Inflation and currency collapse. Argentina has long battled inflation; it reached hyperinflation levels (>100% annual) in 2023. Turkey’s annual inflation spiked above 85% in late 2022, though it has since moderated with aggressive rate hikes. Nigeria’s inflation has been lower (around 20% in 2025) but its currency (naira) has repeatedly crashed against the dollar – losing roughly 60% of its value from 2023 to 2025. In short, inflation, weak exchange rates, and costly cross-border payments are the engines behind stablecoin uptake. The evidence from user data confirms this: for example, Nigeria’s stablecoin transaction volume jumped 40–50% in the wake of tighter FX restrictions. Nigeria illustrates the stablecoin story vividly. Its naira has weakened sharply (about 60% since 2023), and inflation hovered 20% in 2025. Under such stress, Nigerians have turned in large numbers to USDT and USDC. Industry reports show that Nigeria processed nearly $22 billion in stablecoin transactions over July 2023–June 2024 – more than any other Sub-Saharan country. That accounted for 43% of all crypto volume in the region. USDT is dominant (about 88% of volume) due to its ubiquity and low fees, with USDC the second. Much of this on-chain activity corresponds to ordinary retail behavior. As one report notes, roughly 70% of Nigerian stablecoin users rely on them for personal needs like savings and remittances. When the naira was under pressure, many converted small amounts of naira to stablecoins. For example, on-chain data saw spikes in transfers under $1 million during devaluations, reflecting thousands of retail users moving modest sums to safety. Peer-to-peer networks (on Telegram, local exchanges, or apps like Yellow Card) became lifelines after the Central Bank banned crypto-related banking services in 2021. Nigerians adeptly shifted to P2P crypto trades and blockchain bridges, effectively running an underground stablecoin economy. The policy environment is shifting too. After years of hostility, Nigeria’s Central Bank in late 2023 announced it would lift the ban on crypto while regulating exchanges. Argentina’s financial chaos has made it a case study in digital dollarization. After 2020, inflation exploded to triple digits. By 2023, cumulative inflation reached 161% for the year, crushing the peso’s value. In this environment, stablecoins quickly moved from niche to necessity. Argentinian platforms like Ripio and LemonCash report that stablecoin-to-peso transaction volumes surged 40–50% after the government tightened currency controls in 2023. Citizens use USDT and USDC to immediately switch pesos into digital dollars at the black-market rate (“blue dollar”), often using a known strategy called the “rulo” (arbitraging official vs parallel rates). The economics are stark: with capital controls, acquiring a real dollar is bureaucratic and often impossible, but stablecoins provide a 24/7 access. Argentinian users even pay salaries, rent, and everyday bills with crypto dollars, effectively bypassing volatile peso pricing. This grassroots behavior contrasts with the formal stance: Argentinian law (e.g. Law 27,739) now applies AML rules to crypto firms, and regulators monitor stablecoin transactions. Nonetheless, given that over 250% inflation (normalized internationally) persisted into 2024, demand for any stable store of value was enormous. In response, President Javier Milei’s pro-crypto policies have further encouraged usage, even as authorities warn of risks. One crypto analyst observed, “Stablecoins have become a critical financial tool, offering Argentinians a hedge against relentless peso devaluation”. Turkey’s crypto scene is also booming. The Turkish lira has been volatile – a 2021 central bank fiat ban and years of policy-driven declines drove locals toward crypto. Despite an April 2021 ban on crypto payments, public interest kept growing. One survey notes half the population has owned some crypto. Importantly, stablecoins feature prominently: a recent on-chain analysis found Turkey’s USD stablecoin purchases amounted to 3.7% of GDP in 2024. That is remarkably high by global standards. By some estimates, Turks moved over $63 billion in cross-border payments using stablecoins in 2024. This demand persists even after inflationary pressures eased somewhat. The Turkish government has since implemented steep interest rates (37% by early 2026) and FX interventions, bringing headline inflation down to 30%. Yet crypto use remains ingrained. Trading volumes for lira-to-crypto pairs have skyrocketed (an 800% jump since 2021) as people treat crypto as a digital dollar proxy. Traders explicitly use USDT/USDC to preserve purchasing power. Regulators in Turkey have responded with mixed measures. The central bank still forbids crypto for retail payments, reflecting concerns about monetary control. But lawmakers have also established frameworks: for example the Capital Markets Board now licenses crypto exchanges and stablecoin issuers, subject to AML/KYC rules. As one report notes, Turkey’s stance is “refined” – authorities neither embrace crypto fully nor ban it outright, but aim for oversight. The result is stablecoin usage growing under a de facto regulated environment. Stablecoins offer several clear advantages in volatile economies. They are a relatively liquid U.S. dollar substitute: holders need only a phone and internet to store value internationally. This provides automatic diversification away from hyperinflationary money. Remittance and cross-border business become cheaper and faster: blockchain transfers settle in minutes, often costing a few cents, compared to multi-hour SWIFT transfers with multi-percent fees. Stablecoins also allow access to global financial services (e.g. decentralized finance or crypto exchanges) without needing a local bank, thus promoting inclusion. In emerging markets plagued by inflation and FX shortages, stablecoins have emerged as digital lifelines. They let people circumvent failing monetary systems and access dollars instantly. As evidence, millions in Nigeria, Argentina, Turkey and elsewhere now hold crypto dollars to preserve wealth and facilitate trade. However, these benefits come with caveats. Stablecoins do not eliminate risk; they simply shift it from onshore currency management to new forms of trust and compliance. International studies (e.g. by the IMF and BIS) warn that rapid stablecoin adoption can create new channels of financial volatility, suggesting policymakers cannot ignore them. For the general public in these countries, the key takeaway is this: stablecoins can hedge against local currency erosion, but users should stay informed. Only use well-known, audited stablecoins (like USDC/USDT) and trusted platforms. Understand that even digital dollars rely on the integrity of issuers and on-chain security. With the right cautions, however, holding a stablecoin can be a powerful tool to protect savings.

johneb492254456

What Are Stablecoins and How Do They Work?

What Are Stablecoins and How Do They Work?Macro Drivers in Emerging Markets

Stablecoin Adoption: Nigeria, Argentina, and Turkey

Nigeria: Crypto Dollarization on the Rise

Argentina: Hyperinflation and Digital Dollars

Turkey: Crypto Adoption Amid Lira Turmoil

Benefits, Risks, and Limitations

Benefits:

Risks and challenges: Stablecoins are not magical cures. Major risks include:

Conclusion

How CBN’s FX Policy Architecture Is Reshaping Naira Strength Between September 2025 and April 2026

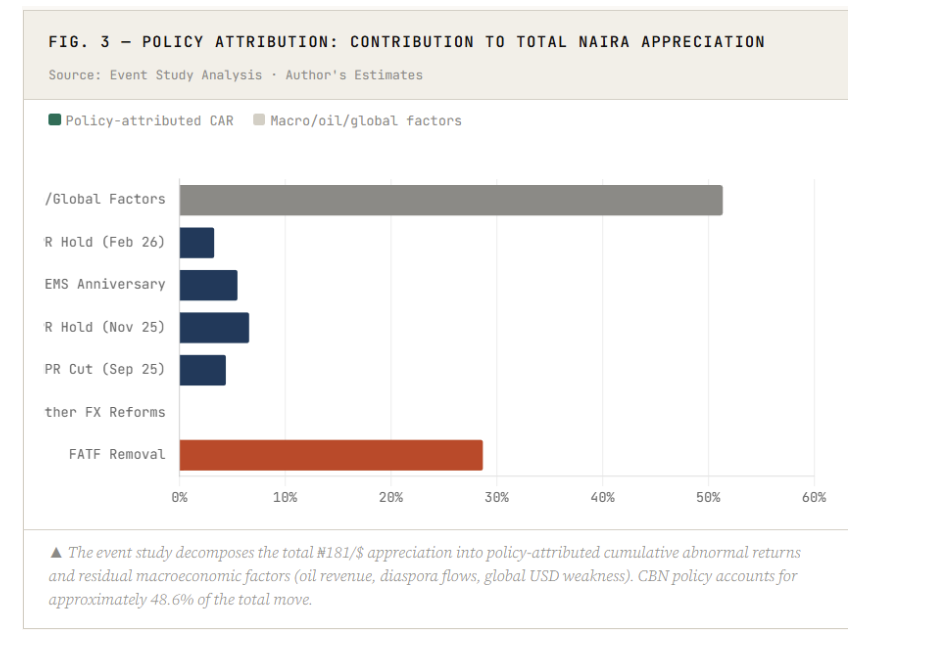

April 15, 2026 by johneb492254456 In the months following Nigeria’s most aggressive monetary tightening cycle in recent history, a quiet but remarkable transformation was unfolding in the foreign exchange market. The Nigerian naira, a currency that had shed more than half its value in two years and had become shorthand for economic distress, was beginning, for the first time in over a decade, to hold ground. Then gain it. Between September 2025 and April 2026, the naira appreciated from approximately ₦1,540 to ₦1,359 per dollar, a nominal gain of roughly 11.8%. For context, this marks Nigeria’s first sustained multi-month currency appreciation since 2012. It did not happen by accident. It was the product of a deliberate, sequenced, and in many ways courageous policy architecture by the Central Bank of Nigeria (CBN) under Governor Olayemi Cardoso. This article dissects architecture, the policy decisions, their timing, their mechanisms, and, critically, their measurable impact, using four econometric frameworks to assess how much of the naira’s recovery can be attributed to CBN actions versus broader macroeconomic forces. The naira’s trajectory over this period was not a straight line upward, it was a story of volatility compressing, confidence building, and structural reforms embedding themselves into market behaviour. The chart below maps monthly closing rates against key policy events. −88.4%Reduction in annualised FX volatility: from 4.58% in 2024 to just 0.53% in 2025. This structural decline in currency risk is arguably more significant than the level appreciation itself — it lowers the risk premium demanded by foreign portfolio investors. The CBN’s approach during this period was notable for its multi-dimensional character. Rather than relying on a single instrument, Governor Cardoso’s team deployed a layered framework spanning monetary policy, FX market structure, regulatory reform, and institutional credibility. What distinguishes this period’s policy mix is not any single measure but the deliberate sequencing. The MPR cut signalled intent; EFEMS provided the structural plumbing; the FATF delisting triggered the capital flow surge; the corridor adjustment managed liquidity without reversing gains; and the diaspora accounts deepened the supply side of the FX market. Each layer reinforced the others. If one had to identify a single inflection point in this story, it is October 24, 2025, the day the Financial Action Task Force (FATF) formally removed Nigeria from its list of jurisdictions under increased monitoring. The announcement, made at a Paris plenary session, followed a two-year remediation process that had required Nigeria to overhaul its anti-money laundering and counter-terrorist financing frameworks. The market’s response was striking in its speed and magnitude. Within five trading days, the naira had rallied to ₦1,444/$, a 10-month high representing a ₦86/$ move in less than a week. Foreign reserves crossed $43.1 billion. Dollar holders rushed to offload positions. The Association of BDC Operators noted that many dealers sold dollars below their purchase price as the gap narrowed sharply. “The FATF delisting is a strong affirmation of our reform trajectory and the growing integrity of our financial system.” — CBN Governor Olayemi Cardoso, October 2025 The economic mechanism was straightforward: FATF grey list membership raises the effective cost of doing business with a country, correspondent banking relationships become more expensive, cross-border transactions face higher compliance friction, and international capital views the jurisdiction as higher-risk. Removal reverses all of this simultaneously, acting as a structural re-rating of Nigeria’s financial system. Our event study analysis estimates the FATF event contributed approximately ₦52/$ of the total ₦181/$ naira appreciation recorded between September 2025 and April 2026, roughly 28.7% of the total move. No other single policy action came close. EFEMS: One Year of Market Transformation The Electronic Foreign Exchange Matching System deserves a standalone treatment because its impact, though less dramatic in any single moment than the FATF event, was arguably more transformative in structural terms. Launched in December 2024, EFEMS provides real-time, transparent matching of FX buy and sell orders across authorised dealer banks, eliminating the opacity that had long allowed arbitrage, speculative positioning, and rate manipulation to thrive. EFEMS also worked in tandem with the FX Code, published by the CBN in January 2025, which imposed conduct standards on authorised dealer banks. Together, these tools shifted Nigeria’s FX market from a discretionary, relationship-based system toward a rules-based, price-transparent one, the type of market structure that institutional foreign investors require before deploying capital. To move beyond narrative and toward quantifiable attribution, we apply four econometric frameworks to the period data. Each addresses a distinct question about the policy-FX relationship. The OLS regression estimates that each additional $1 billion in external reserves is associated with a ₦6.2/$ naira appreciation, holding other factors constant. Each major CBN policy action (captured via a binary dummy) contributes on average ₦18.3/$ of appreciation. The FATF removal carries a standalone coefficient of ₦52/$, confirming it as the dominant structural variable in the model. The adjusted R² of 0.87 means the model explains 87% of the variance in monthly USD/NGN rates using only four policy-related variables. This is a high explanatory power for a macroeconomic FX model with a small sample, and it strongly supports the hypothesis that CBN policy was the primary driver of naira strength in this period. There is a tendency in popular financial commentary to focus on the level of the exchange rate — ₦1,359 versus ₦1,540, as the headline metric. But the GARCH analysis reveals something arguably more important: the volatility of the naira has collapsed from 4.58% annualised (2024) to just 0.53% (2025). This is not a rounding error, it is an 88.4% structural reduction in FX risk. The GARCH Finding: Why Volatility Matters More Than Level There is a tendency in popular financial commentary to focus on the level of the exchange rate — ₦1,359 versus ₦1,540, as the headline metric. But the GARCH analysis reveals something arguably more important: the volatility of the naira has collapsed from 4.58% annualised (2024) to just 0.53% (2025). This is not a rounding error, it is an 88.4% structural reduction in FX risk. Why does this matter? Volatility is a central input in the cost of capital that foreign investors demand. A high-volatility currency requires larger hedging costs and risk premiums. As volatility compresses, the return on NGN-denominated assets effectively rises relative to peers, attracting more inflows, which further suppresses volatility. This is the virtuous cycle that CBN’s EFEMS platform and transparent market reforms have initiated. The naira’s appreciation was not solely a function of confidence and policy credibility; it was also underpinned by a real and substantial improvement in Nigeria’s FX supply position. External reserves grew from $40.5 billion in July 2025 to $45.2 billion by April 2026, an 11.6% increase driven by multiple converging inflows. Nigeria’s total capital inflows reached approximately $21 billion in 2025, with the Nigerian Exchange Limited recording transactions of ₦11.9 trillion, the highest since 2007. Foreign investors’ share of NGX transactions rose from 15.25% in 2024 to 22.21% in 2025. These are not marginal signals; they represent a structural re-engagement of global capital with the Nigerian market. The naira’s recovery story is real, documented, and econometrically supported. But intellectual honesty requires acknowledging the vulnerabilities that remain. The CBN’s own 2026 Outlook, and projections from Meristem Securities, Comercio Partners, and Citibank, all point to a constructive but conditional path ahead. The Constructive Case External reserves are projected to reach approximately $51 billion by year-end 2026, supported by Eurobond issuances, growing non-oil exports, and diaspora inflows. Headline inflation is projected by the CBN to moderate to 12.94% in 2026, down from an average of 21.26% in 2025. GDP growth is forecast at 4.49%, the highest in several years. Meristem projects USD/NGN in a ₦1,350–₦1,529 band for the full year, with the CBN maintaining positive real interest rates to preserve FPI attractiveness. The Risk Scenarios Three risk channels warrant monitoring. First, oil price weakness: crude averaged $63–72/barrel in the analysis period, but global demand slowdowns (partly reflecting US tariff uncertainty in early 2026) could compress Nigeria’s FX earnings. Second, inflation persistence: if Nigeria’s inflation differential with the US remains wide (12–16% vs 3%), PPP dynamics will exert steady depreciation pressure over the medium term. Third, capital flow reversal: foreign portfolio investments are by nature volatile, a global risk-off event could rapidly reverse inflows and pressure reserves. The PPP/REER analysis adds an important nuance: at ₦1,359/$, the naira is estimated to be approximately 5–10% below its PPP-implied value of ₦1,200–₦1,300. The REER stands near 98–100, approaching long-run equilibrium. This means CBN’s work has been corrective rather than distortive, the currency is closer to where inflation fundamentals say it should be. Further appreciation of the same magnitude as 2025 is unlikely without additional structural shocks or sustained commodity windfalls. Sources: Central Bank of Nigeria (CBN) — MPC Communiqués No. 159 & 160, Reforms & Initiatives page, Exchange Rate data (cbn.gov.ng) · TradingEconomics — Nigeria Interest Rate, USD/NGN historical data · Legit.ng — Year-in-review FX analysis, EFEMS anniversary reporting · TheCable — CBN 2025 policy impact review (Dec 31, 2025) · Vanguard Nigeria — FATF grey list analysis · BRB Capital — Post-MPC September 2025 report · Meristem Securities — 2026 FX outlook · Comercio Partners — Policy Shock to Structural Reset (2026) · Exchange-rates.org — USD/NGN historical 2025–2026 · Strategy& (PwC) — Nigeria 2026 Economic Outlook. Econometric Note: OLS, event study, GARCH(1,1) and PPP/REER estimates are based on publicly available monthly data (8-month observation window). Coefficient estimates should be interpreted with appropriate caution given small sample sizes. All model results are directionally consistent. Disclaimer: This article is for informational and analytical purposes only. It does not constitute investment advice.

johneb492254456

The Story Behind the Numbers

FX Rate Trend: September 2025 to April 2026

Three distinct phases are visible. The stabilisation phase (September–October 2025) saw the rate hold near ₦1,530–₦1,540, with the September MPR cut signalling policy pivot but not yet driving large moves. The acceleration phase (November–December 2025) delivered the bulk of the appreciation, ₦95/$ in two months, as the FATF delisting, foreign inflows, and narrowing BDC spreads converged. The consolidation phase (January–April 2026) saw the rate settle into a tighter ₦1,340–₦1,430 range, with volatility at historic lows.

Three distinct phases are visible. The stabilisation phase (September–October 2025) saw the rate hold near ₦1,530–₦1,540, with the September MPR cut signalling policy pivot but not yet driving large moves. The acceleration phase (November–December 2025) delivered the bulk of the appreciation, ₦95/$ in two months, as the FATF delisting, foreign inflows, and narrowing BDC spreads converged. The consolidation phase (January–April 2026) saw the rate settle into a tighter ₦1,340–₦1,430 range, with volatility at historic lows.CBN’s Policy Architecture: Seven Decisions That Mattered

Date

Policy Category

Measure / Description

Rate at Time (₦/$)

Immediate Impact

Sep 23, 2025

Monetary

MPC cuts MPR 50bps to 27.00% (first cut since 2020). CRR for DMBs adjusted to 45%. New 75% CRR on non-TSA public sector deposits. Corridor set to +250/−250bps.

1540

−₦8/$ (appreciation)

Oct 24, 2025

Institutional

Nigeria removed from FATF grey list — formal end of 2-year remediation. Naira hit 10-month high within 5 days. Foreign reserves crossed $43.1B. FPIs accelerated inflows.

1530

−₦86/$ (5-day move)

Nov 25, 2025

Monetary

MPC holds MPR at 27%. Adjusts corridor to +50/−450bps (asymmetric) — signals intent to ease money market rates without triggering FX outflows. Inflation at 16.05%.

1460

−₦12/$ (stability)

Dec 2, 2025

Regulatory

New cash policy: removes all deposit limits and fees. Tightens withdrawals to ₦500K/wk (individuals) and ₦5M/wk (corporates). Promotes e-channel migration to reduce cash-driven FX demand.

1440

−₦4/$ (mild)

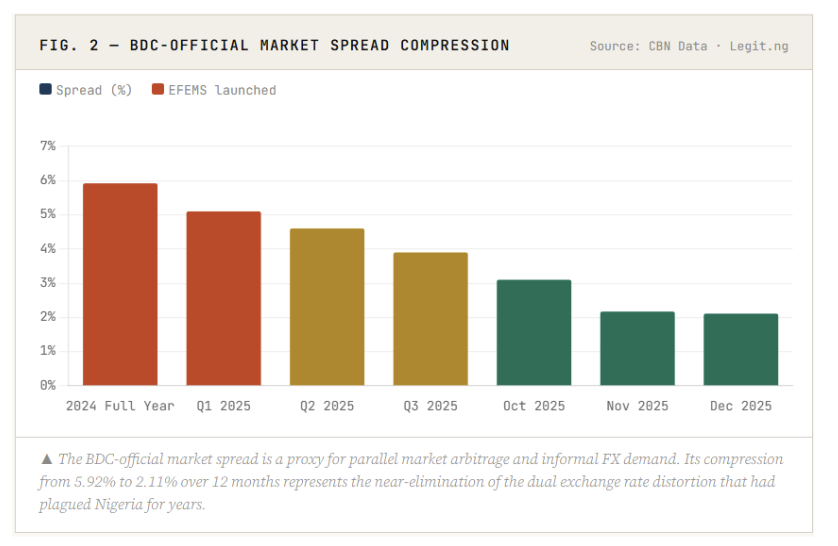

Jan 6, 2026

FX Market

EFEMS 1st anniversary. Naira hits all-time official high of ₦1,419/$. BDC-official spread at 2.11% vs 5.92% in 2024. EFEMS effectively eliminated parallel market arbitrage over 12 months.

1419

−₦11/$ (5-day avg)

Jan 10, 2026

FX Market

NRNOA and NRNIA accounts fully operational. Non-resident Nigerians can remit, hold, and invest foreign earnings locally. Targets ~$20B+ annual diaspora flows.

1430

−₦2/$ (initial)

Jan 24, 2026

FX Market

CBN announces comprehensive FX manual overhaul (to be released Q1 2026). Deputy Governor states it will ‘change and improve the value of the naira and reduce volatility’.

1435

−₦3/$ (guidance)

Feb 24, 2026

Monetary

MPC holds MPR at 27%. Inflation 15.1% (10th monthly decline). CRR 45% maintained. Statement reinforces data-dependent easing trajectory for 2026.

1370

−₦5/$

The Logic of Layering

The FATF Catalyst: October 24, 2025

By EFEMS’s first anniversary on January 6, 2026, the statistics told a compelling story: the BDC-official spread had compressed from 5.92% in 2024 to 2.11%, and the naira hit an all-time official high of ₦1,419/$. The parallel market premium, once a source of enormous rent extraction and dollar hoarding, had been structurally narrowed.

By EFEMS’s first anniversary on January 6, 2026, the statistics told a compelling story: the BDC-official spread had compressed from 5.92% in 2024 to 2.11%, and the naira hit an all-time official high of ₦1,419/$. The parallel market premium, once a source of enormous rent extraction and dollar hoarding, had been structurally narrowed.Econometric Evidence: Quantifying the Policy Impact

What the OLS Model Tells Us

What the OLS Model Tells UsThe GARCH Finding: Why Volatility Matters More Than Level

Why does this matter? Volatility is a central input in the cost of capital that foreign investors demand. A high-volatility currency requires larger hedging costs and risk premiums. As volatility compresses, the return on NGN-denominated assets effectively rises relative to peers — attracting more inflows, which further suppresses volatility. This is the virtuous cycle that CBN’s EFEMS platform and transparent market reforms have initiated.

Why does this matter? Volatility is a central input in the cost of capital that foreign investors demand. A high-volatility currency requires larger hedging costs and risk premiums. As volatility compresses, the return on NGN-denominated assets effectively rises relative to peers — attracting more inflows, which further suppresses volatility. This is the virtuous cycle that CBN’s EFEMS platform and transparent market reforms have initiated.External Reserves and Capital Flows: The Supply Side Story

The composition of reserve growth matters. Three channels dominated: foreign portfolio investment, which returned to Nigeria’s reformed FX market after years of abstention; diaspora remittances, channelled increasingly through the official NRNOA/NRNIA accounts; and oil revenues, supported by the Dangote Refinery’s ramp-up to 700,000 barrels per day, which reduced crude import dependence. The CBN spent approximately $7.53 billion on FX market interventions in 2025, a significant commitment to defend the new rate equilibrium, while still achieving net reserve accumulation.

The composition of reserve growth matters. Three channels dominated: foreign portfolio investment, which returned to Nigeria’s reformed FX market after years of abstention; diaspora remittances, channelled increasingly through the official NRNOA/NRNIA accounts; and oil revenues, supported by the Dangote Refinery’s ramp-up to 700,000 barrels per day, which reduced crude import dependence. The CBN spent approximately $7.53 billion on FX market interventions in 2025, a significant commitment to defend the new rate equilibrium, while still achieving net reserve accumulation.2026 Outlook: Progress, but Fragile

An Analysis of Commodity Cycles as the Hidden Driver of Emerging-Market Currency Stability

March 2, 2026 by johneb492254456 In 2024–2026, volatile commodity prices, especially cocoa, oil, and gold, have been hidden stabilizers for many emerging-market currencies. For example, soaring cocoa prices (up 172% in 2024) dramatically boosted export revenues in Ghana and the Ivory Coast, helping Ghana’s central bank build reserves and the cedi to appreciate (the cedi was about +42% stronger by mid-2025). Similarly, higher oil prices have bolstered Nigeria’s foreign exchange reserves and helped stabilize the naira (which traded below ₦1,400/$ in early 2026 as Brent rose above $69). Gold’s surge (40% higher in 2025 vs 2024) drove record trade surpluses in Peru and lifted South Africa’s terms of trade, underpinning relative stability or gains in the sol and rand. In short, commodity price cycles and emerging-market currency stability are closely linked: when export commodity prices rise, these economies often see healthier external accounts, easing exchange-rate pressure and inflation, a dynamic that influences investor confidence and central bank policy decisions. Global cocoa prices exploded in 2024 due to weather shocks in West Africa (Ghana, Ivory Coast). Cocoa jumped 172% in 2024, briefly hitting a record $13,000/ton. Analysts warned prices would stay “historically elevated” into 2025. Indeed, by October 2025, cocoa costs were still more than double early-2024 levels. (By early 2026, with better harvests on the horizon, cocoa futures began to correct – ICE cocoa prices hit multi-year lows asthe Ivory Coast/Ghana trimmed official prices.) Ghana’s cedi: Ghana, a top cocoa exporter, saw a direct benefit. The huge jump in cocoa earnings helped Ghana rebuild its foreign reserves and support the cedi. By late 2025, Ghanaian authorities credited “higher export earnings” from cocoa (and gold) for stronger external liquidity. In fact, Ghana’s cedi appreciated sharply in 2025: it was about 42% stronger against the dollar by mid-2025. This helped Ghana climb back to a B- rating (S&P noted cocoa/gold prices have “unusually favorable” in 2025, supporting the cedi and lifting reserves from $6.8B to $11B). With more FX inflows, the Bank of Ghana could ease some exchange-rate pressure – though inflation remained high (25% in early 2024), a legacy of past devaluations. Ivory Coast (CFA franc): Ivory Coast (world’s No.1 cocoa producer) saw its export revenues surge. Improved terms-of-trade from soaring cocoa exports helped narrow a large current-account deficit (projected to fall to 1–5% of GDP in 2024/25). The CFA franc (pegged to the euro) remained stable on the peg – inflation stayed around 3% – but higher cocoa FX earnings strengthened the regional reserves pool. (By late 2024, regional WAEMU reserves fell to low levels, but were buoyed by new Eurobond inflows and rules tightening repatriation of cocoa revenues.) In summary, rising cocoa prices in 2024–25 lifted Ghana’s and the Ivory Coast’s export receipts, which in turn underpinned their currencies. Ghana’s experience shows how a “commodity boom” can rapidly improve reserves and stabilize a currency. Oil price trends 2024–2026: After peaking around $80–$90 in mid-2022, crude prices cooled by late 2024. Brent ended 2024 at $74.6/barrel, down 3% on the year. In 2025, oil mostly traded in the $60–75 range (fluctuating with OPEC+ cuts and demand concerns). By early 2026, prices were rallying again: Brent was around $69 in Feb 2026, notably above Nigeria’s budget benchmark ($64.8). (Global factors like U.S.-China relations, Iran tensions, and shifts in supply/demand drove these swings.) Nigeria’s naira: Oil revenues are Nigeria’s FX lifeblood (80% of FX). As oil prices strengthened in late 2025/early 2026 (and after Nigeria eased FX market reforms), the naira steadied and even rallied slightly. In Feb 2026, analysts noted that the oil price rally “would largely bolster” Nigeria’s fiscal revenues, FX reserves, and promote exchange-rate stability. Indeed, the naira traded below ₦1,400/USD on the official market (a notable improvement). In 2025, the naira had its best year in over a decade: it gained roughly 7–7.5% in 2025 after having lost 41% in 2024. Commodity impact: Higher petrodollar inflows mean more USD supply, easing black-market pressure on the naira. (Of course, inflation and policy matters too – Nigeria’s inflation was 15% by end-2025 – but the oil tailwinds gave breathing room.) Analysts caution that lower oil (with current low production) could quickly pressure the naira again, highlighting the tight FX link. Venezuela’s bolívar: Venezuela’s case is more complex. The economy still suffers hyperinflation and extensive dollarization, but oil wealth remains central. In late 2025, the interim government agreed to ship 50 million barrels of oil to the U.S., bringing in $500m; $300m of these proceeds were injected to “stabilize” the FX market and protect the bolívar. Business leaders publicly welcomed this oil-funded USD injection as a way to “regularize and stabilize the exchange system”. In practice, these moves aimed to close the gap between Venezuela’s official and black-market rates. Still, inflation was extreme: private estimates for 2025 inflation were >400%. So while higher oil export revenues provide critical hard-currency support, the bolívar’s stability remains fragile. The currency did see a dramatic change from mid-2025: the old bolívar was replaced by a new currency (pegged loosely to the “petro” crypto), with USD/VES trading around 400 by early 2026. That’s far from stable by developed-world standards, but better than its prior hyper-inflationary collapse (USD/VES peaked at 11.8 million in July 2025). In summary, oil cycles in 2024–2026 have significantly influenced Nigeria’s and Venezuela’s currencies: higher oil prices and flows generally eased FX shortages (strengthening the naira) or allowed government FX support operations (in Venezuela), whereas low oil periods would reverse those effects. Gold price trends 2024–2026: Gold has been a standout commodity in 2024–25. After a mid-2022 correction, gold prices surged in 2024–2025 amid inflation and geopolitical uncertainty. Scotiabank notes gold averaged 40% higher in 2025 than in 2024 (though some cooling is expected in 2026). Precious metals benefited from safe-haven demand: the USD’s unusual weakness in late 2024/25 also helped gold (and other metals) prices. Thus, 2024–25 saw multi-year highs in many currencies: for example, in Nigeria, the naira price of gold tripled (up 121%) due to devaluations and inflation, and Venezuela saw an 84% rise in gold in bolívars. These are extreme cases of how inflation erodes currencies – investors flocked to gold. South Africa (rand): South Africa is one of the world’s largest gold producers. Rising global gold prices help its export revenues and terms of trade. Indeed, in late 2025, the rand was noted to be strengthening alongside gold: Reuters reported on Dec 15, 2025, that the rand “strengthened” against the dollar as “higher gold prices” supported it. Local traders explicitly link Rand gains to the gold rally, and forecasts noted South African gold prices rose 30–45% in local-currency terms. While the rand also depends on many factors (like trade flows and Fed policy), the gold boom provided a tailwind. The South African Reserve Bank also cited resilient FDI inflows and stable inflation. Still, the direct link to gold is clear: when bullion is firm, miners export more revenue, giving the rand support. Peru (sol): Peru is a major producer of gold (and copper). Soaring metals prices vastly improved Peru’s terms of trade in 2024–25. Scotiabank reports Peru ended 2025 with a record trade surplus, driven by metal exports – gold alone was on average 40% pricier than in 2024. These export gains translated into a strong sol (PEN). Remarkably, the sol “showed a surprising combination of strength and stability in 2025”: it appreciated about 5–7% on the year (around S/3.56 per USD by year-end 2025). While the primary reason cited is a very weak US dollar globally, Peru’s robust external accounts were a close second driver. In short, high gold and copper earnings gave policymakers room to cut rates and keep inflation low (consumer inflation held near 2% by the end of 2025), which in turn supported the currency. (Note: Peru’s central bank often tightens in election years, but solid trade gave it flexibility.) These commodity-currency links interact with broader macroeconomics. Key points: Commodity price booms have quietly underpinned currency stability in key emerging markets from 2024 through early 2026. Soaring cocoa prices in West Africa bolstered the cedi and eased balance-of-payments strains in Ghana and Ivory Coast. Rising oil prices and improved fiscal oil receipts buoyed Nigeria’s naira and gave breathing space to its economy. And gold’s bull run helped South Africa and Peru accumulate reserves and keep inflation in check, supporting their currencies. These hidden commodity cycles — intertwined with macro factors like inflation and policy — have shaped investor sentiment and central bank choices in the region. Future fluctuations in cocoa, oil, and gold will likely continue to ripple through emerging-market FX markets, making them essential bellwethers for analysts and policymakers alike.

johneb492254456

Cocoa Cycles & West African Currencies (Ghana, Ivory Coast)

Oil Cycles & Petrocurrencies (Nigeria, Venezuela)

Gold Cycles & Mining Economies (South Africa, Peru)

Macro Factors, Inflation, and Policy Implications

Conclusion

Nigeria’s Rate Pivot: Assessing the Impact of the CBN’s 26.5% Policy Rate on the Naira Outlook

February 27, 2026 by johneb492254456 Nigeria’s Central Bank, CBN, executed a pivotal monetary policy shift on February 23-24, 2026, trimming the Monetary Policy Rate (MPR) by 50 basis points to 26.5% from 27%, marking the first cut of the year and the second under Governor Olayemi Cardoso’s tenure. This decision, made at the 304th Monetary Policy Committee (MPC) meeting, reflects growing confidence in Nigeria’s disinflation trajectory, with headline inflation easing to 15.1% in January 2026 from peaks above 34% in prior years. While retaining the Cash Reserve Ratio (CRR) at 45% and the Liquidity Ratio at 30%, the CBN signaled a cautious pivot toward supporting growth amid stabilizing external buffers like foreign reserves hitting a 13-year high near $50 billion. This rate adjustment arrives against a backdrop of robust naira performance in February 2026, as highlighted in Wiretimes’ Weekly FX and Market Intelligence report by Wewire. The report notes that the currency outperformed the African FX basket, appreciating steadily across three reporting weeks: it kicked off with a 1.44% week-to-date (WTD) gain to USD/NGN 1,363.34 (month-to-date or MTD: 1.44%; year-to-date or YTD: 5.59%), built on that momentum with a further 0.90% WTD advance to 1,351.05 (MTD: 2.32%; YTD: 6.44%), and moderated to a 0.67% WTD rise ending at 1,342.06 by February 19 (MTD: 2.97%; YTD: 7.06%). This sustained strength was fueled by bolstered FX liquidity, sharper price discovery through ongoing market reforms, and dampened dollar demand, all reinforcing near-term stability for the naira. The Naira’s February rally played out distinctly across markets, underscoring maturing FX reforms initiated in mid-2023. In the Nigerian Autonomous Foreign Exchange Market (NAFEM) the official window, the naira appreciated progressively. It opened February around ₦1,386.55/$1, dipped briefly to ₦1,390/$1 early on, then strengthened to ₦1,345.45/$1 by February 18 and ₦1,342.06/$1 by February 19. CBN data confirms a simple average (mean) rate of ₦1,356.98/$1 on February 25, with intraday highs at ₦1,361.50 and lows at ₦1,353.00, closing at ₦1,359.50. Investing.com tracked USD/NGN at approximately ₦1,351.82 on February 25, up 0.06% daily but reflecting 4.51% monthly gains. Parallel rates, often called the “black market,” traded at a premium but converged notably. Early February saw USD/NGN between ₦1,440-₦1,465/$1, narrowing the arbitrage gap. By mid-month (February 9-18), it stabilized at ₦1,440-₦1,455 buy and up to ₦1,480-₦1,510 sell amid school fees and import demand. This premium around 8-12% over NAFEM has shrunk from 2025 highs, signaling reduced speculation. Lower policy rates typically exert downward pressure on currencies by reducing foreign capital inflows seeking high yields. In Nigeria, however, the 50bps trim to 26.5%, still elevated globally, may reinforce naira strength through transmission channels. Lower domestic credit costs (e.g., lower lending rates) curb import demand, easing dollar pressure and supporting FX reserves. Enhanced liquidity from retained CRR aids banks in funding real sector loans, stabilizing inflows without overheating inflation. Analysts like FXTM’s Lukman Otunuga note the cut “stabilizes and potentially bolsters” the naira, given its 6% YTD gains pre-cut. Bullish Outlook for Naira Stability CBN eyes 4.49% GDP growth and 12.94% inflation for 2026, implying steady naira around current levels. Key Risks and Downside Scenarios Carry Trade Reversal: If global rates (e.g., Fed at 4-5%) stay attractive, outflows could test ₦1,400/$1 in NAFEM. For portfolios, the pivot favors naira assets: overweight local equities (banks up 5-10% post-announcement), sovereign bonds (yields dipping 50-100bps), and hedged dollar exposure. Exporters benefit from stability, while importers lock rates amid convergence. Monitor MPC March signals further cuts hinge on February CPI (due early March). In sum, the 26.5% MPR anchors a “soft landing,” extending February’s naira momentum into 2026 stability, provided reforms endure. Investors should eye reserves and oil for directional cues.

johneb492254456

Naira’s February Surge: Official and Parallel Market Dynamics

NAFEM (Official) Rates

Parallel (Black) Market Rates

Market

Early Feb Rate (USD/NGN)

Mid-Feb Rate (USD/NGN)

Feb 25 Rate (USD/NGN)

Appreciation (MTD Feb)

NAFEM (Official)

1,386-1,390

1,342-1,345

1,356.98 (avg)

2.97%[user-provided data]

Parallel/Black

1,440-1,465

1,440-1,510

N/A (est. 1,480-1,500)

2-3% (aligned)

Mechanics of Rate Cuts and Currency Valuation

Potential Impacts: Bullish Case vs. Risks

Scenario

Naira Projection (USD/NGN, End-2026)

Key Driver

Probability

Base (Continued Reforms)

1,320-1,380

Reserves >$51B, cuts to 24%

60%

Bull (Aggressive Easing)

<1,300

FX inflows double

20%

Bear (Global Shock)

>1,450

Oil <$70, outflows

20%

Strategic Implications of Nigeria’s Rate Pivot for Investors

How Greenland Is Becoming a New Flashpoint for Global Resource Competition

February 19, 2026 by johneb492254456 Greenland’s vast Arctic frontier is rapidly moving from a remote backwater to the center of global geopolitical and resource competition. Warming is opening shipping lanes and revealing under-ice deposits, making Greenland “a strategic Arctic linchpin”. Its position atop the North Atlantic anchors the Greenland–Iceland–U.K. (GIUK) gap, a Cold War chokepoint that remains vital for tracking Russian naval movements. The U.S. maintains a large military presence there – notably the Pituffik (Thule) Space Base for missile-warning and space surveillance – under a 1951 defense agreement with Denmark. At the same time Greenland sits astride emerging Arctic routes (the Northwest Passage and a Transpolar corridor) that, as sea ice thins, could one day slash Asia-Europe voyage times]. In short, climate change and geography are giving Greenland outsized military and logistic importance in the US/EU–Russia–China balance of power. Greenland is estimated to hold enormous quantities of critical minerals. Its rare earth element (REE) reserves – used in magnets, batteries and advanced electronics – may exceed 30 million tonnes in total (with about 1.5 million tonnes currently “proven” as economically viable). This ranks Greenland among the world’s top REE holders (roughly 8th globally) and possibly second only to China once more exploration is done. Major known deposits include the Kvanefjeld and Tanbreez projects in southern Greenland. (Kvanefjeld’s ore contains both rare earths and uranium; Tanbreez is rich in heavy rare earths plus zirconium/niobium.) In addition, Greenland has significant known occurrences of graphite (for batteries), copper, gold and other “modern” minerals. Overall, one recent survey found 25 of the EU’s 34 critical raw materials inside Greenland]. Greenland’s offshore oil and gas potential is also large on paper. A USGS assessment in 2007 estimated “significant oil and gas reserves” on the Greenland shelf. Subsequent seismic surveys hinted at hydrocarbon prospects under the seabed. However, Greenland’s government (citing environmental and economic concerns) halted new petroleum licensing in 2021. Thus despite reports of “vast reserves of oil… offshore”, drilling is currently off-limits. Exploiting any oil would require building pipelines and ports in extreme conditions – a multi-billion dollar gamble many consider unprofitable at today’s prices]. United States: Washington views Greenland through both strategic and economic lenses. Militarily, U.S. strategy is focused on denying adversaries sanctuary: Trump’s push for “ownership” was justified as essential to defend the GIUK gap. Analysts say Greenland gives the U.S. “disproportionate leverage” by hosting early-warning radar and anchoring an anti-sub chokepoint. On resources, the U.S. has quietly ramped up engagement: for example, in 2023 the Danish and Greenland foreign ministers met U.S. officials amid talk of sharing critical minerals. The Biden administration has extended financing and trade agreements to help Greenland develop mining in ways that secure supplies of rare earths outside China. In 2024 U.S. diplomats even reportedly lobbied Denmark to steer Greenland’s richest rare-earth concession (Tanbreez) toward Western companies. All these moves reflect a U.S. desire to pre-empt China and Russia: “Gaining access to Greenland’s mineral resources would be in line with the Trump administration’s drive to secure critical minerals as a national security imperative”. China: Beijing calls itself a “near-Arctic state” and has long eyed Greenland’s minerals and routes, though its foothold is now limited. Chinese state firms won a 6.5% stake in the Kvanefjeld rare-earth project, and Chinese investment once accounted for over 10% of Greenland’s GDP. China’s stated Arctic policy (the “Polar Silk Road”) highlights shipping and scientific interests. In practice, however, most Chinese Arctic engagement is with Russia’s Northern Sea Route; cooperation with Moscow on icebreakers and LNG shipping has taken priority. In Greenland itself, security concerns have limited China’s gains: past bids by Chinese firms to buy airfields or naval bases were blocked by Denmark under U.S. pressure. Today Chinese miners are essentially on the sidelines. A recent analysis notes that “since Donald Trump’s first presidential term… Chinese companies in Greenland have faced pushback,” and Beijing has discouraged new ventures there. Chinese officials officially oppose U.S. “threats” in Greenland, but Chinese firms do hold interests (for example, Shenghe Resources in Tanbreez) which Western partners have worked to contain. Russia: For Moscow, Greenland is a strategic concern more than an immediate resource target. Russia’s Arctic strategy emphasizes its own hydrocarbon-rich shelf and the Northern Sea Route (NSR). Russia has invested heavily to keep the NSR open year-round – cargo through the route jumped from 33 million tons in 2021 to nearly 39 million in 2024 – and fields like Yamal and Gydan will anchor a vast “new oil and gas province” to serve Asian markets. In that context, Greenland faces Russia across the Arctic; control of Greenland would constrain the Russian Northern Fleet’s access to the Atlantic. Hence U.S. officials frame Greenland as a counter to Russian power projection. Russia, meanwhile, portrays the U.S. debate as Washington in disarray – Beijing observers quip that a U.S. annexation of Greenland would mean “NATO’s demise” and benefit China. (Notably, Russia is now deepening ties with allies like India under a new logistics pact for Arctic ports, underlining how the Arctic is a broader contest.) European Union (and Allies): European countries see Greenland’s minerals as a way to diversify away from China. The EU’s 2023 Critical Raw Materials Act specifically identifies Greenland in its global supply chain plans. The UK has launched trade talks in 2025 to secure rare-earths, as have France and other NATO partners. At a 2025 summit, Greenland’s prime minister described the EU as a “stable, reliable and important partner” and urged it to invest in Greenland’s mines. Brussels has already signed an EU–Greenland raw-materials partnership (2023) and is working with Denmark on Arctic development. EU strategists caution that any European efforts must include strict environmental and social safeguards – Greenpeace notes that “opportunities for mining and trans-Arctic shipping will not be commercially viable in the near term” – and stress close coordination so as not to undercut each other (e.g. UK vs EU competitive deals). In short, EU capitals see Greenland as a Western-friendly resource base to counter Chinese dominance, but also recognize Greenland’s autonomy and want to respect its climate policies. Greenland’s leaders face a classic dilemma. On one hand, mining and (potentially) oil development promise revenue, jobs and steps toward economic independence from Danish subsidies. Greenland Minerals Ltd. estimates that the Kvanefjeld rare-earth mine would eventually produce over $600 million in annual revenue (nearly four times Greenland’s current GDP). With imports and aid from Denmark equaling half the economy, Greenlanders eyeing full sovereignty see resource exports as an alternative. On the other hand, development threatens Greenland’s fragile environment and traditional livelihoods. Mining requires massive infrastructure – roads, ports, power – in a land with almost no existing transport networks. Extracting one metal often involves byproducts of another (e.g. uranium in the Kvanefjeld ore). Local people recall that past Arctic mining in places like Narsaq left heavy-metal pollution decades later. Greenland’s Inuit population insists on control over any project. The 2009 Self-Government Act enshrines the right of Greenlanders to self-determination – meaning no foreign “sale” of Greenland can occur without local consent. In practice, this has given Greenland’s parliament veto power over projects. In 2021 the new Inuit Ataqatigiit (IA) government, elected on an anti-uranium platform, passed a law banning uranium mining. The effect was immediate: it blocked the giant Kvanefjeld project and sent Greenland Minerals Ltd. (the developer) into legal battle. Local opinion is split: while some Inuit leaders see a mine as a route to jobs and independence, others worry that trucks, spills, and waste would disrupt fishing, hunting and tourism. Most Greenlanders (and all major parties) agree that Greenlanders themselves must decide if and how to develop resources. Environmentalists also sound the alarm on climate and biodiversity. Greenland contains unique ecosystems like the North Water Polynya and harbors a huge fraction of the world’s freshwater in its ice. Any new mining poses risks of pollution to rivers, fjords and the Arctic Ocean. Moreover, paradoxically, exploiting Greenland’s fossil fuels would exacerbate the climate crisis that is melting the island itself. Climate analysts note that policies should balance resource security and climate policy, since unchecked mining in Greenland’s melting environment could cause “further harm” with global impact. Greenland today sits at a crossroads of climate change, great-power rivalry, and the energy transition. Its enormous mineral endowment gives it real economic leverage and strategic relevance – but bringing those resources out is fraught. Recent analyses conclude that “economic ambitions need to be matched by coordinated approaches to climate security, emerging risks and long-term stability in a rapidly changing Arctic.” In practice, this means any race to exploit Greenland must be managed collaboratively, respecting Greenlanders’ rights and fragile environment as much as it chases ores and oil. The stakes are high: a successful Greenland strategy could help the West break China’s metals monopoly and boost Arctic security; a reckless one could damage an ecosystem vital to global climate and blow a hole in Western alliances.

johneb492254456

Greenland’s ice sheet is rapidly melting (as shown above), exposing mineral-rich rock once locked in by ice. Climate change is transforming Greenland’s ice cover: in 2025 it marked its 29th consecutive year of net ice loss, with melt rates far above the 1990s average. Scientists warn the ice sheet is nearing a critical tipping point, whose collapse could raise global sea levels by over 7 meters. The retreating ice and warming temperatures now expose vast resource deposits (from copper to nickel) and open the Northwest Passage for more months each year. As one analysis notes, “melting land and sea ice is making Greenland’s rich mineral and hydrocarbon deposits more accessible”. This long-hidden wealth has drawn a global “treasure hunt” for metals like nickel, cobalt, and rare earths needed for EV batteries and green tech. However, analysts caution that extraction will be extremely challenging: Greenland’s ice-free area is tiny, its terrain rugged, and there are virtually no roads or deep ports. Every ton of ore would have to be barged or flown out, substantially raising costs.Resource Endowment: Rare Earths and Oil

Great Power Interests

Economic Opportunities vs. Environmental and Social Risks

Balancing the Stakes: Opportunities and Risks

Conclusion

Why FX Policy Innovation Is Becoming a Competitive Necessity for African Central Banks

February 16, 2026 by johneb492254456 Across Africa, central banks are adopting new foreign‐exchange (FX) policy tools to manage volatile currency markets. In early February 2026, Ghana’s central bank unveiled a structured “discretion-under-constraint” FX framework for dollar interventions, and Nigeria’s central bank approved weekly $150,000 dollar sales to licensed Bureau de Change (BDC) operators. These parallel moves – a rule-based auction system in Ghana and expanded retail FX access in Nigeria – respond to a common challenge: global monetary divergence, capital flow volatility, and inflation pressures. African FX policy is becoming more innovative as countries compete to maintain stable exchange rates and attract investment. Currency stability in Africa matters because sharp swings in exchange rates can fuel inflation and economic instability. Ghanaian cedi and US dollar notes. Ghana’s central bank (BoG) has detailed new guidelines for FX spot interventions, announced February 10, 2026. Under this structured discretion-under-constraint approach, the BoG will hold periodic dollar auctions whenever the cedi’s movements fall outside pre-set triggers. Crucially, the framework does not peg the cedi at a fixed rate but aims to smooth out “excess short-term volatility”. In practice, only licensed banks may bid in these auctions (in $500,000 increments), with each bank limited to 20% of any auction’s volume. The auctions use a multiple-price format: banks quote USD bids in cedi terms, and the BoG fills buy or sell orders from the most competitive prices until the announced volume is reached. By imposing clear rules and limits, the new BoG FX framework preserves market-driven price discovery while curbing wild swings. The BoG emphasizes that spot interventions now form part of a broader FX operations framework (alongside reserve accumulation and FX intermediation) to deepen transparency and confidence. At the same time, the central bank explicitly ties this policy to inflation: it notes that stability in the cedi “remains central to inflation control and broader macroeconomic recovery. In effect, Ghana’s structured approach means the central bank retains some discretion to act when needed, but only within a transparent, rule-based system. This balances flexibility and predictability. As one Ghanaian news source explained, the rule-based auctions will “allow the exchange rate to be market-driven while limiting excess short-term volatility – but not eliminating it”. In other words, Ghana is innovating its FX policy by formalizing when and how it intervenes, so that markets can anticipate BoG actions. The hope is that greater clarity and constraints will reduce speculative attacks on the cedi while still accommodating necessary corrections. In contrast to Ghana’s auction model, Nigeria’s central bank (CBN) has tweaked the participants in its FX market. A circular dated February 10, 2026, allows all duly licensed Bureau de Change (BDC) operators to buy U.S. dollars from authorized dealer banks, up to $150,000 per week per BDC. Previously, BDCs had been largely shut out of official channels; this change restores their access (via banks) at prevailing market rates. The stated goal is to improve FX liquidity in the retail segment – helping individuals and small businesses obtain dollars for legitimate needs like travel, school fees, or imported inputs. By widening the base of official dollar buyers, the CBN hopes to narrow the gap between Nigeria’s official and parallel exchange rates, which had widened sharply. The new Nigeria BDC policy comes with strict safeguards. Authorized dealers must conduct full KYC checks on BDC customers, and existing BDC guidelines still apply. Any unsold dollars bought by BDCs must be returned to the market within 24 hours (they are not allowed to hoard foreign currency). Settlement rules ensure all transactions go through bank accounts (not third-party cash) to enhance transparency. In sum, this Nigerian Bureau de Change dollar sales policy is an attempt to combine wider market access with tighter controls: licensed BDCs can once again participate, but under a disciplined quota system. The CBN frames it as part of a broader strategy to “deepen market efficiency, enhance transparency and strengthen the overall functioning of the FX system”. Both the Ghana and Nigeria reforms reflect challenging global conditions. As major central banks (notably the U.S. Federal Reserve) raised interest rates in 2022–2025, emerging markets faced capital outflows. Economists note that higher U.S. rates make dollar assets more attractive, pulling capital away from markets like Africa. This leads to rapid outflows from African markets, causing local currencies to weaken and markets to become volatile. The Habtoor Research analysis explains that when U.S. interest rates rise, “investment returns in the U.S. become more attractive… [which] draws capital away from emerging markets, including those in Africa”. The result has been sharper currency swings and inflation pressures. Indeed, to counter these forces, many African central banks have tightened policy themselves. The same analysis notes that African central banks often raise their own rates “to preserve foreign investments and curb capital flight, thus preventing further currency depreciation and keeping inflation in check”. In this era of monetary divergence, stable and flexible FX policies are seen as crucial. Central banks can no longer rely on benign external conditions. Instead, they need tools to buffer their economies from global shocks. Ghana’s auction framework and Nigeria’s BDC scheme are examples of such FX market innovation in Africa. By intervening in a more rule-based way or by expanding official dollar supply, these countries seek to manage the volatile capital flows and import costs that come with global rate cycles. For emerging economies, FX stability is not just a technical concern – it’s fundamental to macroeconomic health. A volatile or collapsing currency can rapidly import inflation, since most food, fuel, and capital goods are priced in dollars. Ghana’s authorities have been explicit: stable exchange rates are “central to inflation control”. In late 2025, Ghana’s inflation rate fell sharply (to around 5%), driven largely by a stronger cedi and growing foreign reserves. Citing BoG sources, one report notes that a 40%-plus appreciation in the cedi over 2025 (backed by $13.8B in reserves) helped tame imported price pressures. Nigeria faces similar dynamics. After years of dual exchange rates, analysts warned that the FX market distortions had “become intolerable,” deterring foreign investment[4]. In a unified system, all players rely on one market, which reduces arbitrage and builds confidence. Indeed, Nigeria’s overhaul of FX pricing in 2024–2025 was explicitly aimed at ending an arbitrage-rich system that “hampered foreign direct investment”. In short, currency stability underpins growth. It anchors inflation expectations, lowers borrowing costs, and makes trade and investment planning more reliable. When central banks innovate – for example, with transparent auction systems or by ensuring dollars reach ordinary businesses through BDCs – they are trying to prevent the wild swings that can trigger economic crises. As one commentator warned in 2025, slipping back into ad hoc interventions or policy inconsistency could “undo” the gains of reform[22]. This underscores the point: investors and businesses demand credible, stable FX regimes in emerging markets. FX policy innovation in Africa is fast becoming a competitive necessity for central banks. In a global environment where money can flow quickly into or out of countries, a central bank’s credibility depends on effectively managing its currency market. Ghana and Nigeria’s recent measures reflect this urgency. By adopting more structured, transparent interventions, these countries aim to make their FX markets more attractive and stable than those of other countries. The new Bank of Ghana FX framework and Nigeria’s BDC dollar sales rule show how policymakers are tailoring tools to local needs – rule-based auctions for Ghana and expanded retail access for Nigeria. Looking ahead, other African central banks are likely to watch and adapt. If these innovations succeed in smoothing volatility and anchoring inflation, they could set examples continent-wide. Ultimately, maintaining currency stability in Africa’s emerging markets is key to sustaining growth and investment. As external pressures (like divergent global rates and volatile capital flows) continue, central banks will need to keep innovating their FX policies. The goal is clear: stable, predictable exchange rates that support price stability and economic recovery. In the words of Ghana’s central bank, deepening confidence in the FX market is “central to inflation control” – a lesson that resonates across Africa today.

johneb492254456

Bank of Ghana FX Framework: Structured Auctions for Stability

Nigeria Bureau de Change Dollar Sales: $150k Weekly Cap

Global Monetary Pressures and Capital Flows

Why Currency Stability Matters in Emerging Markets

Conclusion: A Competitive Necessity

Love Across Borders: How Stablecoins Are Quietly Powering Modern Remittances

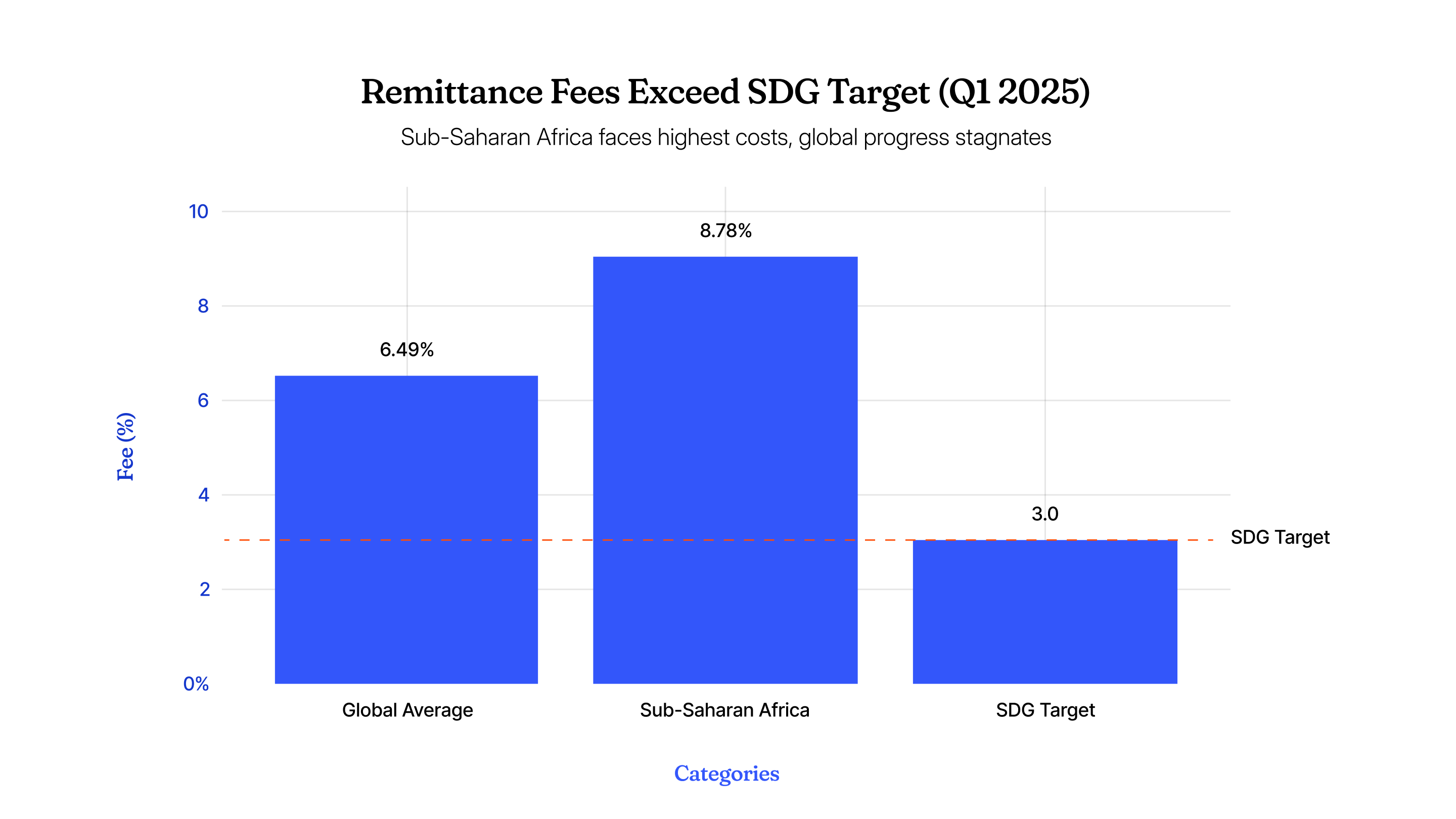

February 11, 2026 by johneb492254456 Remittances represent more than money; they carry love, support, and hope from one country to another. For millions of families separated by borders, sending funds home has long meant high costs, long waits, and lost value. Stablecoins, digital currencies designed to maintain a stable value, are quietly but powerfully changing this by making transfers faster, cheaper, and more reliable. This presentation explores the human side of this shift and why it matters today. Cross-border remittances total hundreds of billions of dollars each year, supporting families in low- and middle-income countries far more than foreign investment or aid in many cases. Yet the process remains burdensome. The World Bank reports that the global average cost to send remittances stayed around 6.49% in 2025, well above the global target of 3%. In regions like Sub-Saharan Africa, fees often rise, sometimes to 8-9%. Delays of several days are common due to multiple banks and intermediaries involved in correspondent networks, plus unpredictable foreign exchange spreads that reduce what recipients actually get. These frictions hit hardest in corridors where people rely on every dollar or peso for essentials like food, education, and healthcare. Stablecoins cut remittance times from days to minutes and slash fees dramatically, often below 1% for the blockchain portion, compared to traditional averages over 6%. In high-adoption areas, this saves households significant amounts annually. Recipients can hold funds digitally or convert to local currency when ready, bypassing opaque intermediaries. Chainalysis highlights how stablecoins serve as a hedge in volatile economies and enable reliable cross-border payments. Adoption thrives in regions facing economic pressures. In Sub-Saharan Africa, stablecoins make up a large portion of crypto activity, with Chainalysis noting 43% of transaction volume in some areas tied to remittances and payments. Latin America sees strong use in corridors like the U.S.-Mexico, where platforms process billions. Asia, including India and the Philippines, integrates stablecoins for diaspora transfers amid large remittance inflows. These areas show grassroots demand—people choose stablecoins for speed and reliability in high-inflation or currency-constrained settings. Reports from Chainalysis and others confirm this practical, need-driven growth, not hype. Stablecoins often work quietly within familiar apps and wallets, not as a full replacement for banks but as efficient rails underneath. Users send via platforms that handle conversions seamlessly, so the experience feels simple. Regulatory steps, like the U.S. GENIUS Act in 2025 and frameworks in other regions, add transparency and trust through reserve requirements and audits. This evolution turns remittances from a slow banking service into a modern payments utility faster, clearer, and more aligned with real human needs. As more fintechs and institutions adapt, expectations for cross-border money movement rise toward what families deserve. Stablecoins are reshaping remittances by prioritizing practicality, delivering more value where it matters most. This quiet transformation empowers families across borders, reduces exclusion, and fosters financial resilience in challenging economies. While challenges like regulation and access remain, the momentum points to broader change. Remittances evolve into something more inclusive and efficient, staying true to their core purpose: connecting people with care and support. The future looks clearer, faster, and more human-centered.

johneb492254456

Stablecoins maintain consistent value by pegging to assets like the U.S. dollar, making them unlike volatile cryptocurrencies. Popular ones include USDT and USDC, which together process massive volumes monthly. Chainalysis data from 2025 shows stablecoins surging in use for practical needs rather than speculation. They operate on blockchain networks that enable near-instant, 24/7 transfers without relying on traditional banking layers. This creates predictability; senders know exactly how much arrives, and recipients avoid surprise deductions. Adoption grows strongest where local currencies face inflation or access to hard currency is limited, turning stablecoins into a bridge for everyday financial needs.

Stablecoins maintain consistent value by pegging to assets like the U.S. dollar, making them unlike volatile cryptocurrencies. Popular ones include USDT and USDC, which together process massive volumes monthly. Chainalysis data from 2025 shows stablecoins surging in use for practical needs rather than speculation. They operate on blockchain networks that enable near-instant, 24/7 transfers without relying on traditional banking layers. This creates predictability; senders know exactly how much arrives, and recipients avoid surprise deductions. Adoption grows strongest where local currencies face inflation or access to hard currency is limited, turning stablecoins into a bridge for everyday financial needs.

How Rules of Origin Are Distorting Global Commerce

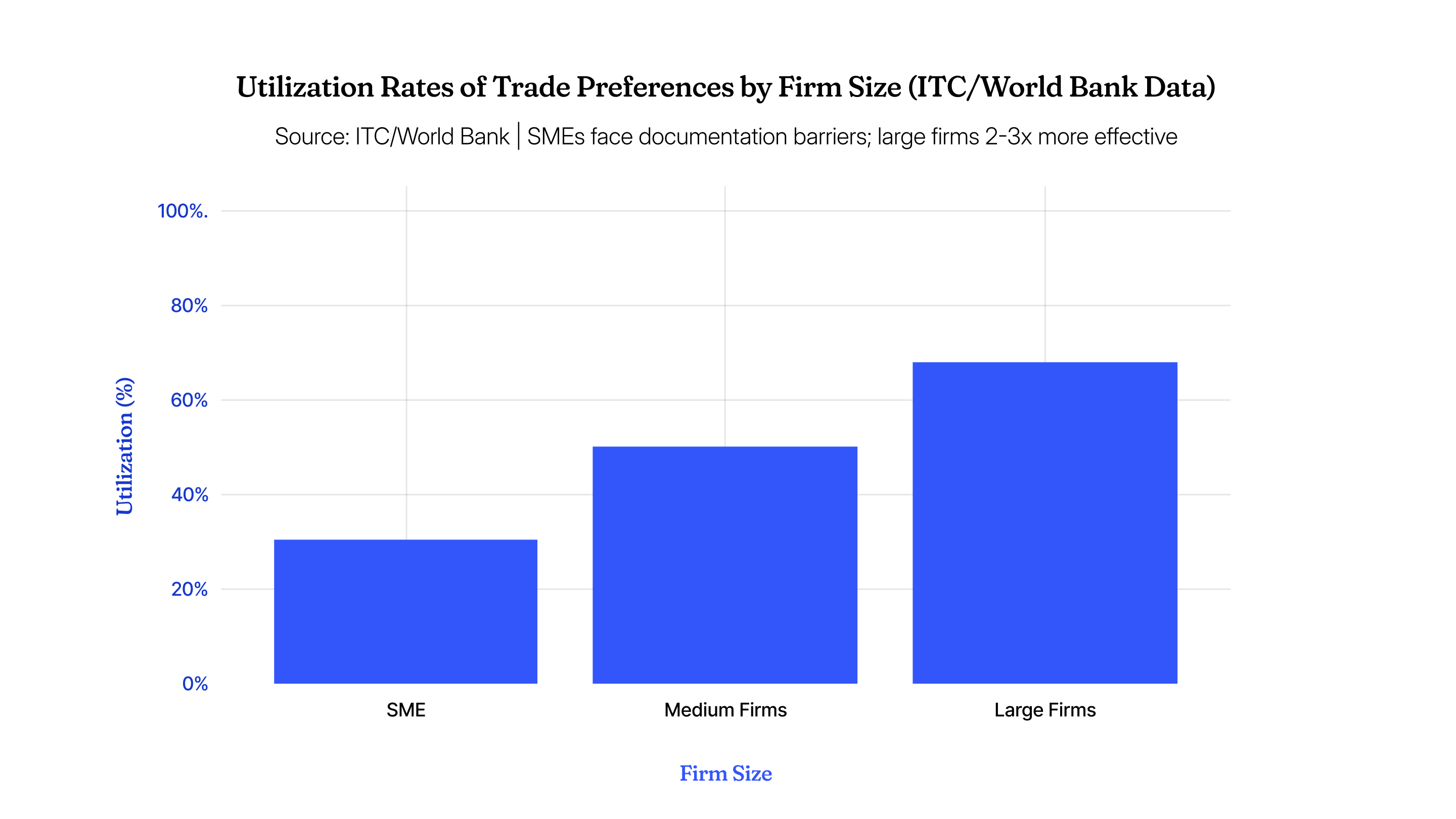

February 4, 2026 by johneb492254456 Global trade is often discussed in terms of tariffs, trade wars, and geopolitical alliances, yet some of the most powerful forces shaping commerce operate quietly in the background. Rules of Origin sit at the center of this unseen architecture. They determine which goods qualify for trade benefits and which do not, influencing prices, supply chains, and access to markets without ever making headlines. As global production becomes more fragmented, these rules increasingly shape trade outcomes in ways most consumers and businesses never fully see. Rules of Origin exist to define the national identity of goods in a world where production spans borders. They establish criteria to determine whether a product is considered domestic or foreign for tariff, quota, and trade preference purposes. These criteria can be based on where a product was last substantially transformed, the amount of local value added, or whether specific manufacturing processes occurred within a member country of a trade agreement. Institutions such as the World Trade Organization and regional trade blocs emphasize that these rules are essential for preventing trade deflection. In today’s trade environment, Rules of Origin increasingly distort decision-making. Companies often reorganize production not to improve efficiency or reduce costs, but to satisfy technical origin thresholds. Manufacturing steps may be relocated solely to qualify for preferential treatment, even if this increases operational complexity. Bloomberg trade analysis has highlighted how firms absorb higher logistics and compliance costs simply to avoid losing tariff advantages. This shift creates a paradox where compliance strategy overrides economic logic. Trade outcomes become less about productivity and more about legal interpretation. Large multinationals often have the legal teams and trade specialists needed to navigate complex origin requirements. Smaller exporters and importers do not. Reports from the International Trade Centre show that small and medium-sized enterprises are significantly less likely to utilize trade preferences because of documentation burdens and uncertainty around compliance. As a result, the benefits of free trade agreements accrue unevenly. This imbalance quietly reinforces market concentration. Firms with scale and regulatory expertise gain an advantage, while smaller players face higher effective trade barriers. In this way, Rules of Origin shape not only cross-border trade flows but also competition within markets. The growing influence of Rules of Origin reflects a broader shift in global trade. Market access is no longer determined solely by price or quality but by regulatory alignment and administrative precision. IMF and World Bank assessments increasingly note that non-tariff measures now pose greater barriers to trade than tariffs themselves. Rules of Origin sit squarely within this category. For consumers, this contributes to higher prices and fewer choices. For businesses, it introduces uncertainty and raises the cost of cross-border expansion. Trade becomes slower, more fragmented, and more dependent on legal interpretation than economic fundamentals. As global trade agreements expand and supply chains continue to reconfigure, Rules of Origin will play an even larger role in determining who benefits from globalization and who does not. Understanding these rules is no longer limited to trade lawyers or customs officials. It has become essential knowledge for manufacturers, importers, policymakers, and even consumers trying to understand why goods cost more or arrive later. The future of trade will not be shaped only by grand geopolitical statements or headline-grabbing tariffs. It will be shaped in the fine print, where Rules of Origin quietly decide access, advantage, and exclusion in the global economy.

johneb492254456

Beyond commerce, Rules of Origin have taken on strategic importance. Governments increasingly use them to influence supply chain geography without issuing explicit bans. By tightening origin requirements or redefining what constitutes sufficient transformation, countries can reduce dependence on certain regions while remaining aligned with international trade rules. Policy analysis from think tanks such as the Peterson Institute and Bruegel has shown how these mechanisms subtly redirect sourcing away from politically sensitive suppliers. This approach allows states to pursue economic security objectives quietly.

Beyond commerce, Rules of Origin have taken on strategic importance. Governments increasingly use them to influence supply chain geography without issuing explicit bans. By tightening origin requirements or redefining what constitutes sufficient transformation, countries can reduce dependence on certain regions while remaining aligned with international trade rules. Policy analysis from think tanks such as the Peterson Institute and Bruegel has shown how these mechanisms subtly redirect sourcing away from politically sensitive suppliers. This approach allows states to pursue economic security objectives quietly.

A Strong Dollar Is Hurting Importers — Even When Prices Look Cheaper

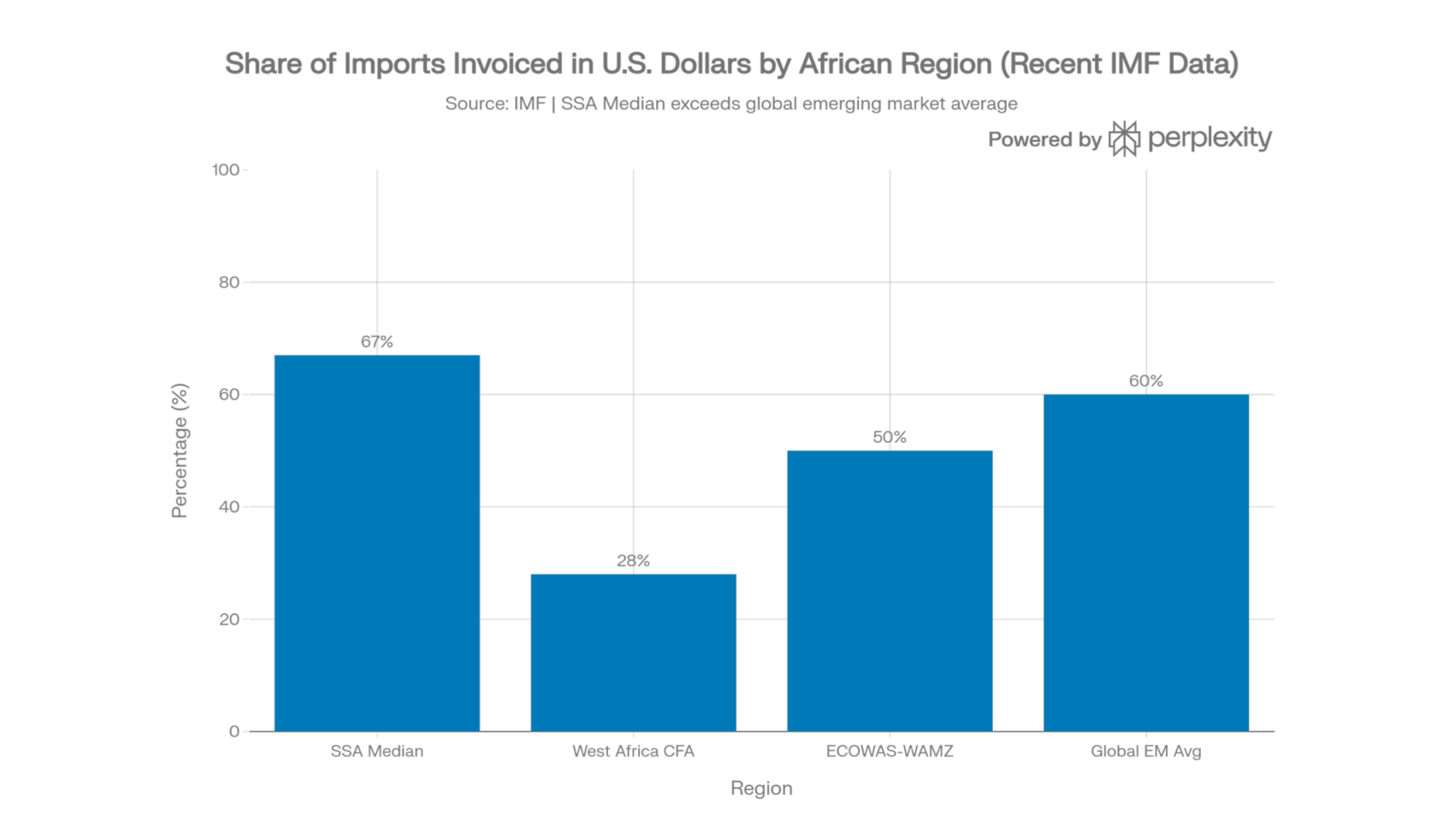

January 28, 2026 by johneb492254456 The fundamental concept that a stronger U.S. dollar benefits importers by increasing their purchasing power often fails to materialize for African businesses. For companies operating in regions like Sub-Saharan Africa, the U.S. dollar is not just a currency but a primary invoicing vehicle for over 80% of imports. Between 2022 and 2025, even as global commodity prices saw periods of cooling, the simultaneous depreciation of local currencies like the Nigerian Naira, Kenyan Shilling, and Ghanaian Cedi meant that the “local currency price” of goods rose sharply. This phenomenon, often referred to as imported inflation, ensures that the theoretical discount of a strong dollar is immediately consumed by the shrinking value of the domestic currency used to acquire those dollars. The promise of cheaper imports assumes that suppliers maintain stable prices and that exchange rate benefits reach the end-user. However, International Monetary Fund reports indicate that global suppliers frequently adjust their dollar-denominated price lists upward to hedge against the volatility of emerging market currencies. For an African business importer, the nominal price on a Proforma Invoice might look stable, but the cost of clearing that invoice in local terms becomes a moving target. Furthermore, the prevalence of dollar-based invoicing means that African importers bear 100% of the currency risk, as most international exporters refuse to settle in local African denominations, effectively shifting the burden of dollar strength entirely onto the buyer. The era of a strong dollar between 2022 and 2025 coincided with aggressive monetary tightening by the U.S. Federal Reserve, which forced African central banks to raise their own interest rates to defend their currencies. For a business importer in Africa, this created a double-edged sword: not only did the dollar become more expensive to buy, but the cost of borrowing local currency to purchase those dollars also skyrocketed. Data from the World Bank suggests that the average cost of business loans in many African nations exceeded 20-25% during this period. These high interest rates effectively cancel out any savings from lower global prices, as the cost of financing the “time-to-market” for imported goods becomes a dominant expense. To protect themselves from further currency slides, sophisticated importers turn to financial hedging tools such as forward contracts and options. However, in a high-volatility environment, the “premium” or cost of these hedges increases dramatically. For many African importers, the cost of securing a forward contract in 2024 became so high that it nearly equaled the expected loss from further currency depreciation. This leaves businesses with a difficult choice: pay a guaranteed high fee for protection or remain exposed to the market. In many cases, the lack of deep, liquid FX markets in Africa means these tools are either unavailable or prohibitively expensive, leaving importers as “price takers” in a hostile currency environment. The strong dollar’s impact extends to the very infrastructure of trade, as shipping lines and insurance providers almost exclusively price their services in U.S. dollars. Even if a business finds a cheaper supplier in Asia, the freight costs and marine insurance premiums must be paid in dollars, which have become more expensive in local terms. Additionally, many African governments calculate import duties based on the “Current Market Rate” of the dollar. As the dollar climbs, the tax burden on the importer rises automatically, even if the quantity of goods remains the same. This “tax on a tax” further inflates the final price of goods, ensuring that the consumer never sees the benefit of “cheaper” global prices. As we move into 2026, African business importers are shifting their strategies to survive the “Strong Dollar Era” by seeking alternatives to traditional trade routes. Many are exploring the Pan-African Payment and Settlement System (PAPSS) to trade in local currencies within the continent, reducing the need for dollar intermediation. Others are engaging in “near-shoring,” sourcing raw materials from neighboring countries rather than distant dollar-based markets. While the strong dollar continues to present a formidable challenge, these shifts in supply chain logic and the adoption of regional digital payment systems represent a critical evolution for African commerce, moving away from a total dependency on a single global reserve currency.

johneb492254456

Beyond the unit price of goods, a strong dollar creates a severe cash-flow mismatch that threatens the survival of small and medium-sized enterprises. As the dollar strengthened through 2024, the amount of local currency required to fund the same volume of inventory nearly doubled in some markets. This forces business importers to divert funds from operations, marketing, and payroll just to maintain their stock levels. Many African businesses operate on credit lines denominated in local currency, which often hit their limits faster as exchange rates deteriorate. The result is a “liquidity trap” where businesses are technically profitable on a per-unit basis but are running out of cash because their working capital cannot keep pace with the dollar’s appreciation.